|

Economic policymakers continue to fight an uphill battle against the forces that threaten to tip the economy back into recession. The new jobs initiative from President Obama faces stiff resistance in Congress, and Federal Reserve officials are beset by internal conflict and a dwindling basket of options. In the meantime, one powerful policy option remains dormant, despite several recent studies that show its potential to lift the economy.

The Federal Reserve is widely expected to embark on new efforts to lower long term-interest rates at this week’s policy meeting on Sept. 20-21. The problem is that the housing crisis is blocking a traditional avenue by which lower interest rates have lifted the economy in the past: Despite historically low mortgage rates, homeowners cannot refinance because their mortgage exceeds their home value and because the refinance process is cumbersome and costly. “We believe that efforts to unclog the mortgage refinancing pipeline would have the most bang for the buck,” says Morgan Stanley economist David Greenlaw.

“The bottom line is that market conditions have

created a potentially costless windfall that is not

being used”

As of June, more than 75 percent of Fannie Mae and Freddie Mac mortgages with 30-year fixed rates have a rate of 5 percent or more, while market rates have been at or below 5 percent for two years, says a new study by mortgage consultant Alan Boyce and Columbia University economists Glenn Hubbard and Chris Mayer. With current mortgage rates just above 4 percent, normal credit conditions would have created three times the current amount of refi activity, they say, which means tens of millions of homeowners are not taking advantage of a historic opportunity. The authors offer a plan they say could reduce mortgage payments by about $70 billion that would act like a long-lasting tax cut for some 25-30 million homeowners.

The basic idea is that the principal value of mortgages backed by Fannie and Freddie are already guaranteed by the government. However, the refi process is fraught with disincentives, including regulations that increase borrowing rates, bank premiums for riskier borrowers, complications from second-mortgage holders, and unnecessarily high closing costs. Several studies show that simply recognizing the implicit loan guarantee could eliminate these inefficiencies and facilitate a streamlined refi process that could have a major economic impact. “The bottom line is that market conditions have created a potentially costless windfall that is not being used,” Morgan Stanley’s Greenlaw wrote in a note to clients last year.

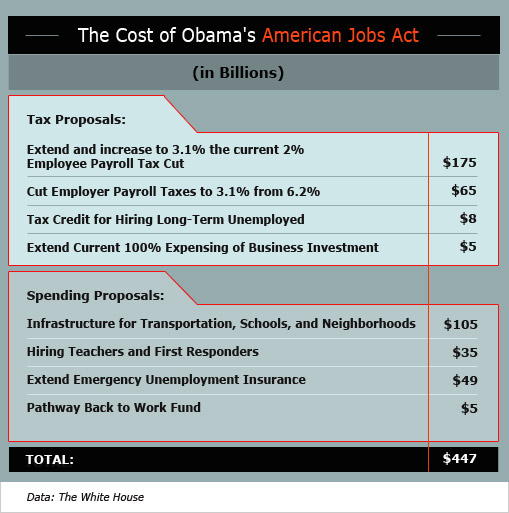

Policymakers share a new urgency that more efforts are needed, but they continue to take a broad focus, with no mention of refi reform in Obama’s plan. House Republicans are sure to pick apart Obama’s $447 billion American Jobs Act, but a return to their bull-headed approach during the debt-ceiling debate seems unlikely. In an NBC/Wall Street Journal poll on Aug. 27-31, 71 percent of Americans had an unfavorable opinion of the way those negotiations were handled. In a speech on Sept. 15, House Speaker John Boehner was critical of Obama’s plan but in a much less strident tone.

Even without any GOP opposition, would Obama’s jobs act lift job growth? Based on the plan’s likely impact on GDP, the answer is yes. Analysts at J.P. Morgan say that if the package were passed in its entirety it could add 1.9 percentage points to economic growth next year. That boost would more than offset the 1.7 percentage point drag that would result from programs set to expire at the end of 2011, the waning stimulus from the 2009 Recovery Act, and the spending cuts from the debt-ceiling deal.

Morgan’s current forecast of only 1.2 percent GDP growth in 2012 assumes no new fiscal stimulus next year and thus includes that entire 1.7 percentage point drag. Morgan’s Michael Feroli says the boost from the entire Obama package would lift Morgan’s forecast to 3.1 percent. If so, that pace would be consistent with stronger payroll gains in 2012 than in 2011.

That’s a lot of ifs, but the analysis makes a key point: Whatever fraction of Obama’s jobs bill that Congress does pass will offer an important offset to the fiscal drag that would otherwise weigh heavily on an already fragile economy next year. Half of that 1.7-point drag on growth next year would come from the expiration of the 2011 payroll tax cut and the end of emergency unemployment benefits, programs that are extended and expanded in Obama’s plan.

One problem is that Americans are sending Washington conflicting signals. The NBC/ Wall Street Journal poll shows that people believe initiatives like those in Obama’s jobs bill, such as extending the payroll tax cut and unemployment insurance and new outlays for construction and job training, are generally good ideas. However, in the same poll 56 percent say Washington should worry more about holding down the deficit, while only 38 percent say lawmakers should worry more about boosting the economy.

Economists know you can’t have it both ways at the same time. Congressional Budget Office Director Douglas Elmendorf echoed that point on Sept. 13 at the first public meeting of the Congressional “Super Committee” on deficit reduction, which is charged with finding at least $1.5 billion in budget cuts over 10 years. He warned that “immediate spending cuts or tax increases would represent an added drag on the weak economic expansion.” However, Elmendorf told the committee that, over a ten-year horizon, both stimulus now and deficit-reduction later could still achieve long-run fiscal stability.

Wall Street has a much more downbeat take on policy: Investors worry that traditionally effective policies are so shackled by politics and a dearth of options, that nothing can pull the economy out of the mud. That’s especially true for monetary policy. Fed chairman Bernanke and a majority of Fed policymakers appear to ready to employ new efforts to stimulate the economy, which Fed watchers expect to be unveiled at the policy committee’s Sept. 20-21 meeting, but the expected impact is small.

Some economists have even suggested the Fed should

charge banks a fee to hold their deposits.

Wall Street anticipates the Fed will begin to increase the average maturity of its $2.7 trillion in securities holdings by buying more long-term securities, while selling an equivalent amount of shorter-term holdings. The intent is to lower long-term rates, especially mortgage rates, further, but most economists expect such an effort to deliver even less rate reduction than was achieved by the last round of outright securities purchases, which added more than $600 billion to the Fed’s balance sheet. However, the biggest potential impact of lower long-term rates is in housing, where the effect is not being felt.

One other option already discussed by the Fed would be to encourage bank lending by cutting the current 0.25 percent interest rate the Fed pays banks to keep their $1.6 trillion in excess reserves on deposit at the Fed. Some economists have even suggested the Fed should charge banks a fee to hold their deposits. A lower or even negative rate would create a disincentive for banks to keep those funds parked at the Fed and an incentive to lend them out.

The bottom line is that the economy does not suffer so much from a lack of policy options, and economists agree that one of the most potent would be mortgage refi reform. One big problem is that policymakers appear just as conflicted as their constituents over what direction needs to be taken, while the economy continues to flounder along. After two years of lackluster recovery and new recession worries, it’s becoming clear that the economy cannot recover quickly on its own under traditional policy efforts.