- Core inflation fell to 0.9 percent in May.

- A 7 percent unemployment rate could be the turning point.

- The manufacturing operating rate was 71.5 percent in May.

Despite the mild 2 percent overall inflation rate in May, as measured by the rise in the consumer price index over the past year, consumers always think prices are too high. They may complain about this year’s 6.8 percent rise in the price of pork chops from a year ago, for example, or the 10.7 percent jump in the cost of public transportation. But so far, households have been able to enjoy some offsets, perhaps in the 2.4 percent decline in the price of chicken or the 9.1 percent drop in the price tag on women’s dresses.

| Where prices have risen and fallen over the past year | |

| Consumer Price Index Category | Percent Change from a Year ago, May 2010 |

| Food and Beverages | 0.7 |

| Housing | 0.5 |

| Apparel | -0.6 |

| Transportation | 10.7 |

| Medical Care | 3.4 |

| Recreation | -0.5 |

| Education | 4.8 |

| Communication | -0.3 |

| Personal Care | 0.8 |

| Energy | 14.7 |

| Total CPI | 2.0 |

| Core CPI (Excludes Energy & Food) | 0.9 |

| Data: Bureau of Labor Statistics | |

Consumers can take heart that the overall inflation outlook remains benign — at least for now. Policymakers at the Federal Reserve certainly think so. Their statement after meeting on June 23 noted the recent weakness in prices of energy and other commodities and the lack of cost pressures amid high unemployment. The Fed’s bottom line: “Inflation is likely to be subdued for some time.” The big question: How long is “some time”?

The question is beginning to divide economists, some of whom fear the Fed could stoke future inflation by sticking with its ultra-low interest rate policy for too long. The answer depends to a great extent on how much slack exists in the economy. The tighter an economy is wound up, the greater the upward pressure on prices. After a recession as severe as the one we just experienced, with so much unemployment and idle production facilities, any sudden upward pressure on wages and prices would seem like a long shot. However, some economists wonder if the economy is stronger than some traditional markers might suggest.

Take May’s 9.7 percent unemployment rate. Until now, economists say, labor costs haven’t begun to push on inflation and won’t until the jobless rate approaches about 5 percent, the rate broadly believed to be full employment. But the severity of the recent recession may have changed that. After the 1973-75 recession wiped out a large amount of U.S. production capacity and the need for many factory skills, the Fed kept interest rates very low, believing full employment was a jobless rate of about 4 percent. The inflation flash point turned out to be a much higher rate, which helped to fuel the decade’s double-digit inflation.

Something similar may be happening this time. Many unemployed workers may never re-enter the workforce, as their skills in real estate, finance, the auto industry and other hard-hit areas go begging. A mismatch between available jobs and the skills of those seeking work is already evident in the record number of long-term unemployed people. Workers also may be less mobile, because falling home values limit their ability to move for new jobs. Plus, studies suggest that the unprecedented length of jobless benefits is discouraging job search.

A growing number of economists now believe the full employment level, as measured by the jobless rate, has risen somewhat. In fact, two Fed officials think it has risen to between 6 percent and 6.3 percent, based on the policy committee’s April forecasts for the long-term unemployment rate. Others, including 2006 Nobel Prize winner Edmund Phelps, think it could be 7 percent, or more, which would mean we’re closer to full employment than we think.

Other traditional measures of economic slack also raise questions. The operating rate in manufacturing, or the percentage of facilities and equipment currently in use, stood at a relatively low 71.5 percent in May. However, it has risen 6.2 percentage points in the past year, the fastest annual increase in more than 25 years, say economists at J.P. Morgan Chase.

The export-led rebound in factory production isn’t the only reason for the increase. Steep cutbacks in capital spending during the recession reduced production capacity. The amount of available facilities and equipment in place has shrunk by a record 1.9 percent from the peak in January 2009, according to Federal Reserve data. Combined with continued strong output, that growth could create production bottlenecks sooner than earlier anticipated, putting upward pressure on prices. If current trends continue, operating rates could reach normal levels of about 79 percent within a year or so.

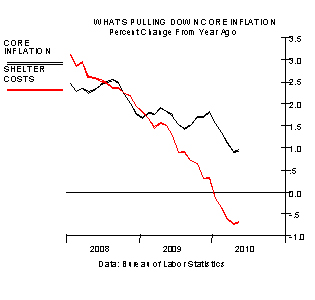

One factor supporting the Fed’s benign inflation outlook is the decline in core inflation, which can be a better indication of the underlying trend because it excludes the short-term ups and downs in energy and food costs. Core inflation has been falling rapidly, to 0.9 percent in May from a peak of 2.5 percent in August 2008. Some analysts even suggest the drop could be a precursor to deflation.

However, the decline has been remarkably narrow, says Barclays Capital economist Dean Maki, concentrated almost exclusively in the “shelter” component of the CPI.

Maki estimates that excluding shelter, which accounts for an outsized 42 percent of core CPI, core inflation hasn’t budged from its 2.1 percent reading this time last year. With signs that home prices and rents are stabilizing, Maki and others say core inflation should bottom out in the second half of the year and set the stage for higher prices in 2011.

If the economists are right, a pickup in inflation next year may well be a greater risk than consumers — and even policymakers — now expect. For household budgets, that could mean fewer less expensive items to provide an offset to those costlier pork chops and bus fares.