By this stage of the recovery, the longing is almost palpable. We want to get back to normal. It’s time to shake off this nasty recession and get back to the serious business of getting richer. We always have in the past. As the investment thinker William Bernstein put it in an interview with The Fiscal Times, “Since the birth of the republic, we have been through mishaps much worse than 2008: a revolution that nearly wiped out our credit, a civil war, the libertarian valhalla of the 19th century that saw several depressions as bad as the thirties, the Great Depression itself, and two world wars.”

Over those tumultuous 200 years, the trend in per capita economic growth has been remarkably steady, and so has the return on capital. Stocks have averaged 6 percent a year over inflation since 1802, according to Wharton professor Jeremy Siegel, or 9 percent a year since 1927 according to the oft-quoted Ibbotson survey. American history, in other words, favors optimists.

But what if history is bunk? The America of 2010 — aging, indebted, overextended and under-educated — is not the fresh-faced republic of 1802, with a continent to exploit and a population surging from immigration. Nor is it the victor of WWII, the only developed nation that escaped the war’s destruction. Economic win streaks do come to an end. Just ask Britain. Or Japan.

Washington and Wall Street are coming around to the idea that the economic future we’re stumbling towards will be far less generous from the normality we long for. The “New Normal” — a disarmingly benign term coined by Mohamed El-Erian, co-chief investment officer of the big California investment firm Pimco — envisions a future of sluggish growth, international discord, increased uncertainty and minuscule returns on capital. Government revenues shrink while spending remains high.

The 8 percent historic returns projected into the future by many corporate and state pension funds (and those retirement calculators offered by your 401(k) administrator) never materialize. The fiscal implication: Pension funds that are a trillion dollars underfunded at 8 percent returns actually face shortfalls two or three times as large. And the mind-boggling $6.6 trillion Retirement Income Gap — the difference between what the nation has saved and what it should have saved, as calculated by a coalition known as Retirement USA — may actually be understated.

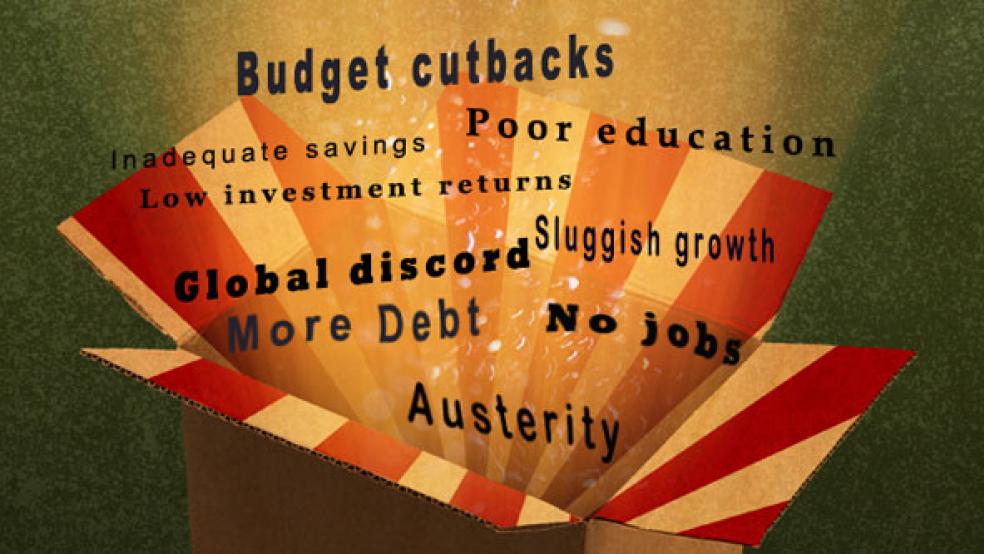

Delving into the logic behind the New Normal thesis is like peering into a Pandora’s Box of economic ills. It’s not for the faint-hearted.

Americans have to deleverage: Households went into the crisis with more debt than at any time in U.S. history. They have to pay that load down, either by saving more or by defaulting. Neither is conducive to economic growth. Government debt is also at levels not seen since the end of World War II. Our leaders can either commit to years of austerity to pay it down or ignore the problem and let inflation and devaluation solve the problem. Again, neither will help economic growth.

Demographics could undo us: In simple terms, economic growth equals labor force growth times growth in productivity. Our labor force will stagnate as the baby boomers retire and the U.S. population’s growth rate slows to a crawl. While dramatic increases in productivity could theoretically take up the slack, that may be too much to ask of a generation whose education, for the first time in American history, ranked in the bottom third of developed nations. And who, for the first time, went to college in lower proportions than their parents.

Globalization will reverse: In an Institutional Investor essay called Paradise Lost, economist Nouriel Roubini and political risk consultant Ian Bremmer argue that 2008 cost the U.S. and other advanced economies the ability to set the global agenda. “The trend is most visible,” they write, “in the transition from a G-7 to a Group of 20 model of international decision making which includes influential and deep-pocketed developing countries like Brazil, China, India, Saudi Arabia and the United Arab Emirates. Without these countries, multilateral efforts to solve pressing transnational problems wouldn’t have much credibility. But getting this varied group to agree on anything will be profoundly difficult.” In the resulting power vacuum, protectionism will rise and the global free trade that fueled a half century of international growth will recede.

Summing up the implications of the New Normal, El-Erian’s boss, Pimco Managing Director Bill Gross, writes in his October newsletter, “The unmistakable fact is that future investment returns will be far lower than historical averages … There is no 8 percent there for pension funds. There are no ‘stocks for the long run’ at 12 percent returns.”

Of course, at the bottom of Pandora’s Box, there was hope. Here too, but in this case it’s a faint hope and it comes not so much from history as from psychology. We can never know the future, the reasoning goes, and we should be humble enough to admit that our vision will always be slanted by the events of the recent past, whether encouraging or frightening. James Paulsen, chief market strategist of Wells Capital and one of the dismal science’s few optimists, suggests that New Normal majority may have overdosed on gloom: “Fears fueled by the “new-normal” story have produced and maintained a bear mania in stock market valuations,” he writes. “If a new-normal lost decade doesn’t appear, won’t [today’s inordinately cautious investors] look silly?”

History would suggest that could happen. But somehow, history isn’t much comfort any more.

Reporter: Temma Ehrenfeld

Eric Schurenberg is Editor-in-Chief of BNET, the CBS Business Network.