|

The Great Recession has profoundly altered the U.S. labor market, says a growing number of economists. The problem is that unemployed workers are not finding their way to available jobs as smoothly as in past recoveries due mainly to a mismatch between the skills companies need and those workers have to offer. If these analysts are right—and there is mounting evidence in their favor—the goal of returning to the heady days of 5 percent unemployment, generally perceived as “full employment,” may no longer be possible, and policymakers may not be able to do anything about it.

Recent Labor Department data, especially the trend in job openings relative to the pace of hiring and the level of unemployment, strongly suggest that the job markets are not functioning as efficiently as they did before the recession. At least some of the high level of unemployment since the recession ended reflects more than just a weak recovery or the uncertain outlook. Job market trends imply that something fundamental has changed in the labor market’s ability to match workers with jobs—a problem that could take a long time to correct.

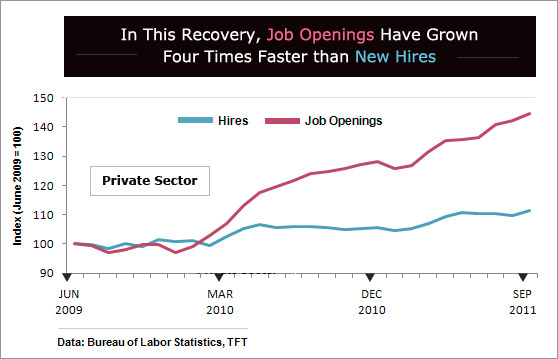

On the surface, the news that September job openings rose to the highest level in three years was positive. What is unusual is that job openings during this recovery have grown four times faster than new hires. A divergence that wide suggests that more is at work here than just corporate caution over Europe, U.S. fiscal policy, and the economic outlook. Even during the “jobless recovery” in the early 2000s, openings and hires tracked each other much more closely. “That job openings are outpacing hires tells us that labor market frictions are keeping the rate of job finding subdued,” says economist Michael Gapen at Barclays Capital.

Those frictions, say Gapen and others, are new structural impediments to job growth. They largely reflect the recession’s deep scars, especially in housing and construction, as well as policymakers’ response to the downturn. It will be years before the construction industry can support its pre-recession level of workers, who now face the difficulty of transitioning to other employment requiring different skills. The same is true for other workers in the many housing-related industries who benefited from the housing bubble. And with one-in-four mortgages underwater, many workers in industries unrelated to housing cannot easily move to other locations where they might find jobs.

In addition, the unprecedented length of jobless benefits, which Congress might extend beyond the current 99 weeks in most states, has the well-documented tendency to limit job search. The weak recovery itself can also create lasting barriers to finding a job if workers stay unemployed for so long that they lose their skills, their workplace contacts, and their attachment to the job market. These are all new obstacles to job gains that economic growth alone—at whatever pace—may not be able to remove.

That’s because these structural changes appear to have lifted the unemployment rate associated with full employment. Prior to the recession, that level was about 5 percent, or a little less. Now, some economists think full employment could be a jobless rate as high as 7-7.5 percent. Over the decades, the level has shifted as the factors affecting job markets have changed. The level is crucial, economists say, because policy efforts that would push the unemployment rate below full employment would create labor shortages leading to hikes in wages and prices that would only stoke inflation.

In the 1970s, for example, the Federal Reserve under Chairman Arthur Burns failed to observe that the jobless rate associated with full employment had risen to around 7 percent. That Fed’s failure to lift interest rates amid rising inflation contributed to the Great Inflation of the 1970s. In contrast, Fed Chairman Alan Greenspan in the late-1990s eschewed loud calls to lift interest rates when joblessness dipped below 5 percent, believing that the full employment jobless rate had shifted down from the 6-7 percent level of the 1980s. He turned out to be right, and inflation remained under control.

One of the strongest arguments that the full employment jobless rate has risen once again is based on the relationship between job openings and the unemployment rate. Economists call it the Beveridge Curve. It represents how efficient job markets are in matching unemployed workers with available jobs, and it strongly suggests that markets face much more difficultly in matching workers with openings. The relationship appears to have shifted in such a way that job openings in recent months are now running 30-40 percent higher than what you would have previously expected at 9 percent unemployment.

Even the views of current Fed policymakers are starting to change. Back in January 2009 when the Fed first published its long-run projection for the unemployment rate, which is essentially the Fed’s estimate of full employment, the policy committee’s forecast was 4.8-5 percent. The November 2011 forecast shows 5.2-6 percent.

Of course, with the unemployment rate currently at 9 percent, the inflation consequences of underestimating full employment are small. “However, as the unemployment rate falls, the inflationary consequences become larger,” says Barclays chief economist Dean Maki.

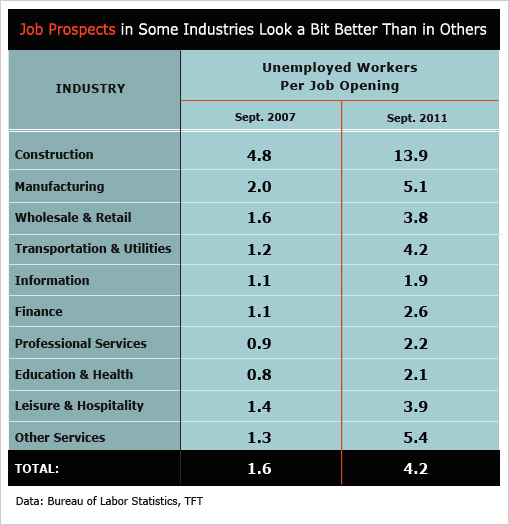

Ultimately, wage growth will be the proof of the pudding for any great shift in the workings of the labor markets. More job openings in industries where workers are hard to find would tend to push up wage growth in those industries. Overall hourly wages and salaries in the private sector are growing only modestly, given that in September there were 4.2 unemployed workers for every job opening. However, construction, where the ratio is 13.9 workers per opening, greatly skews that reading. High-skilled industries where the ratio is much lower, such as information, professional and business services, and healthcare, are areas where wage growth has picked up during the recovery.

Over the next year or two, policymakers will have to come to grips with the fact that stimulative policies can push the economy only to full employment without lifting inflation. Beyond that, programs aimed at retraining and education are one key to putting more people to work. The problem is, in coming years Washington may not have the fiscal resources to commit to those types of efforts.