| | |

Biden Eyes Trillion-Dollar Stimulus as Negotiations Stall

September is just around the corner, but the impending arrival of fall has done little to inspire lawmakers and the Trump administration to come to an agreement on the next coronavirus stimulus bill.

White House Chief of Staff Mark Meadows said late last week that the Trump administration would support a $1.3 trillion bill, moving up from the $1 trillion he has cited in the past – and higher than some Senate Republicans have said they would support.

Saying she was willing to meet Republicans halfway, House Speaker Nancy Pelosi indicated that she would reduce the size of her proposed stimulus bill from $3.4 trillion to $2.2 trillion. But that still leaves an enormous gap between the two parties.

On “Meet the Press” Sunday, Meadows sounded like he had reached his limit, accusing Pelosi of being “willing to turn down $1.3 trillion of help that goes to the American people because she would rather them have nothing than to give way” on her offer.

‘Bad blood’ not making things easier. Part of the problem, The Hill’s Mike Lillis and Scott Wong say, is the fundamental lack of respect between Meadows, a tea part insurgent who has embraced President Trump, and Pelosi, the ultimate Washington insider. “As the parties scramble for an elusive deal on another round of coronavirus relief, mistrust and bad blood between two of the principal negotiators ... have snarled the talks and complicated the path to a timely agreement,” they wrote Monday.

While some of the sniping between the two leaders could be dismissed as political maneuvering that aims to motivate voters ahead of the election, there are fundamental political and philosophical issues at stake. The dispute highlights “the stark ideological differences between the sides when it comes to the government’s role in responding to the public health and economic crises sparked by the coronavirus pandemic — differences all but epitomized in the figures of Pelosi and Meadows,” Lillis and Wong say.

Biden mulls his own coronavirus relief package. If negotiators are unable to move beyond the current stalemate, Democratic presidential nominee Joe Biden may need to move quickly on a coronavirus relief package in January, should he win the election, Axios reported Monday.

Biden’s economic advisers are “are growing increasingly worried that the economy is deteriorating by the day,” Axios’ Hans Nichols and Felix Salmon said, and are warning that “problems can compound and cascade — including business bankruptcies, supply chain disruptions, mass evictions, and huge shortfalls in state and local budgets.”

Jake Sullivan, a senior policy adviser to Biden, told Axios that, “We have always contemplated the need for additional stimulus. We will confront the situation we find in January.”

While Biden’s team hasn’t discussed the plan publicly, advisers say the stimulus package would be in the $1 trillion to $2 trillion range, depending on what Congress is able to do before January. And that’s completely separate from Biden’s previously announced plan to spend roughly $3.5 trillion on clean energy, infrastructure, education and a host of other initiatives designed to revitalize the economy and combat inequality.

One thing motivating Biden’s advisers, many of whom served in the Obama administration, is the perceived failure of the fiscal response to the Great Recession. “They feel that the 2009 stimulus package — the $787 billion American Recovery and Reinvestment Act — was woefully inadequate,” Nichols and Salmon said. “And they're determined not to make the same mistake twice.”

Republicans have also said that they would push more relief spending in January, should Trump win the election. “Trump's call for a $2 trillion infrastructure bill back in March would be a starting point for a 2021 stimulus,” Nichols and Salmon said.

|

|

|

Quote of the Day

“If people want chaos, and I think there’s some people who do — I’m not ascribing that point of view to anyone. I just think there are some people who are motivated by chaos. They think it helps them politically. Then there’s nothing we can put together to make them happy.”

-- Sen. John Kennedy (R-LA), commenting on the possibility that Congress will seek to combine a coronavirus relief bill with a funding package for the 2021 fiscal year, which begins October 1. Lawmakers are expected to pass a continuing resolution to keep the government funded in the new fiscal year, and stimulus money may become an issue as the legislation is negotiated.

|

|

|

Trump’s Payroll Tax Deferral Gets Rolling

The IRS issued guidance late Friday that provides details on President Trump’s executive action to allow employers to stop collecting Social Security taxes for employees starting September 1 through the end of the year.

According to the guidance, employers who choose to participate in the program will stop collecting the 6.2% payroll tax that is the employee’s share of Social Security taxes for the next four months for workers who earn up to $104,000 per year. The employers will then be required to collect twice as much from January to April next year.

According to Richard Rubin of The Wall Street Journal, a worker making $75,000 a year would save about $1,550 by December 31 – but then would owe the same amount in 2021.

“The government’s action doesn’t actually change the underlying taxes, because only Congress can do that,” Rubin said. “Employees would still owe the taxes eventually.

Many businesses have expressed their doubts about the plan,

Federal workers drafted into the program. One employer that will participate is the government. “The federal government will implement an across-the-board payroll tax deferral by all federal payroll providers, so all federal employees who meet the income threshold will see savings,” a senior administration official told Federal News Network Monday. The deferral is expected to begin with the second paycheck of September, and will apply to those with gross Social Security wages of less than $4,000 per pay period.

Unions representing federal workers spoke out against the plan. “Either way, the employee loses,” said Randy Erwin, president of the National Federation of Federal Employees. “If the tax deferment becomes permanent, and provided it is legal, the employee could get a lower payout in retirement. If the deferment is temporary, the employee risks getting a huge tax bill plus interest and penalties early next year.”

Rep. Don Beyer (D-VA), whose district includes thousands of federal workers, also criticized the move. “The Trump administration’s plan to initiate payroll tax deferrals for civil servants treats the federal workforce as a guinea pig for a bad policy that businesses already rejected as ‘unworkable,’” he said, referring to a statement by the U.S. Chamber of Commerce. “This payroll tax deferral does not really put money in workers’ pockets, it simply sets up the members of the federal workforce who can least afford it for a big tax bill that many will not expect.”

|

|

|

Op-Ed of the Day: Once Again, Infrastructure

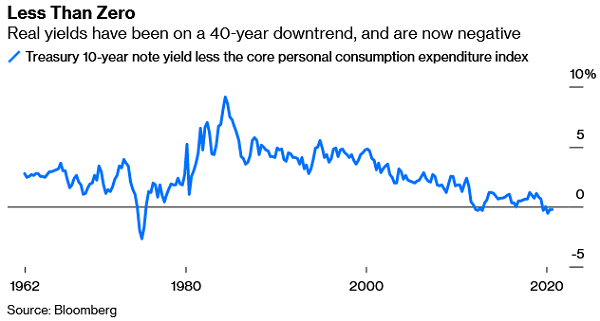

Real interest rates are negative, which means the federal government is essentially getting paid to borrow money right now, once inflation is taken into account. Writing at Bloomberg Monday, Wall Street analyst Paul Podolsky argues that short of widespread social chaos or a balance of payments crisis, the only thing that could push real interest rates back above zero is massive public investment in infrastructure. Doing so would kill two birds with one stone by making much-needed investments in public goods while restoring interest rates to a more normal range.

|

|

| |

While both Republicans and Democrats have talked enthusiastically about infrastructure investment, the problem – aside from their notable inability to get anything done – is that their proposals in the range of $1 trillion to $2 trillion are too small. “To boost growth above its economic potential of about 1.5% a year and match estimates of what is needed to be spent on infrastructure, an investment of around $4 trillion, or close to 20% of gross domestic product, is warranted,” Podolsky says.

Read Podolsky’s argument here.

|

|

| | | | | | | - Sweden Shouldn’t Be America’s Pandemic Model – Scott Gottlieb, Wall Street Journal

- Miracles Are Not a Plan – Jared Bernstein, Washington Post

- Negative Real Rates Aren't Reversing Anytime Soon – Paul Podolsky, Bloomberg

- Why Does It Matter If Interest Rates Are Below the GDP Growth Rate? – Michael Pettis, Carnegie Endowment for International Peace

- Don’t Forget About Inflation – Robert J. Samuelson, Washington Post

- The Fed Is Fighting the Last War on Inflation – Daniel Moss, Bloomberg

- Larry Kudlow’s Economic Hallucinations – Timothy Noah, New Republic

- The Census Is in Trouble. So Is Democracy – Los Angeles Times Editorial Board

- Trump’s Republican Party Is Erasing Reagan’s Memory – Bruce Bartlett, New Republic

- Child Care Has Always Been Essential to Our Economy — Let's Start Treating It That Way –

- Rep. Katherine Clark (D-MA), Sen. Lisa Murkowski KR-AL) and Suzanne Clark, The Hill

- U.S. Expats Can’t Renounce Their Citizenship Fast Enough – Andreas Kluth, Bloomberg

|

|

|

|

|