| | |

Big Banks Say Stimulus Payments Will Start Arriving Wednesday

The latest round of Covid relief payments will start reaching many checking and savings accounts at big banks by 9 a.m. on Wednesday, according to the trade group that governs the ACH Network payment system.

After the American Rescue Plan Act was signed into law last week, there was some confusion — and plenty of grumbling — over when the “economic impact payments” would be available.

“After Wells Fargo & Co., JPMorgan Chase & Co. and Bank of America Corp. told their customers they wouldn’t receive their stimulus money until this week, consumers flooded social media with complaints,” Bloomberg’s Jennifer Surane reports. “But banks were quick to note they haven’t been given the money yet.”

Nine banking and credit union industry groups issued a statement Tuesday saying that the availability of the funds was determined by the Internal Revenue Service, not by them: “While the IRS could have chosen to send the funds via Same Day ACH or provided for an earlier effective date, it chose not to do so. It is up to the sender, in this case the IRS, to decide when it wants the money to be made available and the IRS chose March 17.”

Banks will receive the money from the government at 8:30 a.m. ET on Wednesday. “This is literally the moment in time when the money will be transferred from the government to banks’ and credit unions’ settlement accounts at the Federal Reserve,” Nacha, the group governing the ACH Network, said in a statement. “There is no mystery where the money is from the time the first payment file was transmitted on Friday, March 12 to when all recipients will have access to the money on Wednesday—it is still with the government.”

Some banks and financial technology companies did begin depositing billions of dollars’ worth of payments into customer accounts ahead of the official payment date after they were notified by the IRS that their customers would be eligible for the payments.

Once they receive the money Wednesday morning, banks must make it available to account holders by 9 a.m. ET.

More than 100 million payments are reportedly expected to go out Wednesday via direct deposit, but not all direct deposits will go out at the same time — and some payments will go out in the form of checks or debit cards that will be sent by mail.

|

|

|

Biden Plan: Higher Taxes on the Wealthy, Relief for the Middle Class

President Joe Biden thinks middle-class families need tax relief while the wealthy and corporations need to start paying a bit more, a White House economic adviser said Tuesday.

Bharat Ramamurti, who served as a top economic policy adviser to Sen. Elizabeth Warren in her 2020 presidential campaign and now serves as deputy director of the National Economic Council in the Biden administration, told Bloomberg TV that Biden’s tax proposals will focus on increasing taxes on corporations and the wealthy.

“The president’s tax plan is intended to make sure that middle-class families are not paying more than their fair share and that the wealthiest folks, who by and large have done quite well over the last several years, including during the last year, are paying a little bit more,” Ramamurti said. “We hope to work with Congress to accomplish those goals.”

Ramamurti said that many middle-class families are hurting in the current environment and need the kind of assistance provided in Biden’s $1.9 trillion Covid relief bill. “A teacher and a nurse who collectively make, you know, $110,000, deserve relief,” he said. “And what we’ve seen in the data is that families with that kind of profile have suffered.”

One major question is whether the White House will push to make permanent benefits in the relief legislation that help middle-class families, such as the expanded child tax credit. Ramamurti said that Biden is “interested at looking at that,” but no decisions have been made.

Familiar battle lines form: Meanwhile, Republicans are making it clear that although Biden and some centrist Democrats would like to make the next economic package a bipartisan affair, they have no interest in tax hikes to help pay for new spending on things like infrastructure. “I don’t think there’s going to be any enthusiasm on our side for a tax increase,” Senate Minority Leader Mitch McConnell (R-KY) said Tuesday.

McConnell predicted that Democrats would use the budget reconciliation process to pass their “Trojan horse” of a bill with a simple majority and no Republican support, sneaking tax hikes into legislation authorizing new spending on public goods.

Republican Sen. Rick Scott of Florida also took aim at Biden’s still-developing plan Tuesday, in terms we will likely hear repeatedly in the coming months. “The Biden-Harris administration is fulfilling its campaign promise to ram through job-killing tax hikes,” he said in a statement. “As folks across the nation recover from this economic crisis, the last thing they need is to send their hard-earned money to fund the Democrats’ big government agenda.”

That’s not to say that Republicans don’t have their own tax proposals, though. In stark contrast to burgeoning Democratic plans, Republicans are offering tax cuts for the wealthy. Last week, GOP senators reintroduced the Death Tax Repeal Act of 2021, which would permanently repeal the estate tax, a 40% levy currently applied only to estates worth more than $11.7 million, or twice that amount for couples.

|

|

|

More Lawmakers Call for Tax Day Delay

More than 100 House members signed a letter to IRS Commissioner Charles Rettig Tuesday calling for a delay in this year’s tax filing deadline.

The letter from Democratic Reps. Jamie Raskin (MD) and Bill Pascrell (NJ) requested the delay on behalf of “millions of stressed-out taxpayers, businesses and preparers” who are “still grappling with the massive economic, logistical and health challenges wrought by this devastating pandemic.”

The letter says that the IRS will need to take action to address changes to the tax law in the Covid relief package and that taxpayers will need time, and agency guidance, to understand the changes.

|

|

|

As Biden Sells Relief Plan, Dems Move Beyond Obama Legacy

President Joe Biden visited a suburban Philadelphia flooring business on Tuesday, his first stop on a “Help Is Here” tour to promote the $1.9 trillion American Rescue Plan Act he signed into law last week.

Much like Biden’s push to “go big” with the relief legislation, the tour is part of a concerted administration effort to avoid repeating what many Democrats now see as mistakes made in 2009, when President Obama oversaw a $787 billion stimulus plan in response to the Great Recession.

“It has become an article of faith in the party that Mr. Obama’s presidency was diminished because his two signature accomplishments, the stimulus bill and the Affordable Care Act, were not expansive enough and their pitch to the public on the benefits of both measures was lacking,” Jonathan Martin of The New York Times says. “By this logic, Democrats began losing elections and the full control of the government, until now, because of their initial compromises with Republicans and insufficient salesmanship.”

Obama allies have noticed the shade, The New York Times’s Astead W. Herndon reports:

“The re-examination has irked some of the former president’s allies but thrilled the party’s progressive wing, which sees Mr. Biden’s more expansive plan as a down payment on his ambitious agenda. And it has sent an early signal that Mr. Biden’s administration does not intend to be a carbon copy of his Democratic predecessor’s. Times, all concede, have changed. …

“Both Mr. Obama and Mr. Biden came into office on promises of unity and bipartisanship in the face of an economic crisis, but Mr. Biden is the beneficiary of a changed landscape in the party. Democrats are now more cognizant of Republican obstruction, less deferential to the deficit hawks and energized by a growing progressive wing that has pulled the party’s ideological midpoint to the left.”

Casting a cloud over Obama’s legacy: Asked earlier this month about the prospect of getting GOP cooperation on legislation, Senate Majority Leader Chuck Schumer said that after Democrats succeeded in passing the massive package on their own, he hoped that Republicans might try to work together. “But,” he told CNN, “we're not going to make the mistake of 2008 and 2009 and do such a small measly proposal that it won't get us out of the mess that we are in right now.”

Schumer added that Obama and Democrats had tried a bipartisan approach back in 2009 and 2010. “We cut back on the stimulus dramatically and we stayed in recession for five years,” he said.

Other Democrats — including Biden —have said Obama made a mistake in not selling his rescue plan or explaining it to the American public. “I kept saying, ‘Tell people what we did,’” Biden recalled at an event earlier this month. “He said, ‘We don’t have time. I’m not going to take a victory lap,’ and we paid a price for it, ironically, for that humility.”

Progressives are overjoyed: Those on the left who criticized Obama’s approach are delighted that their critiques have become orthodoxy, at least among Democrats and many mainstream economists — and that Biden has embraced the right lessons, as they see them.

“I am less surprised by the ways in which the [Covid relief] bill was trimmed back, than by the extent that it breaks with the Clinton-Obama model,” economist J. W. Mason wrote Monday. “The fact that people like Lawrence Summers have been ignored in favor of progressives like Heather Boushey and Jared Bernstein, and deficit hawks like the Committee for a Responsible Federal Budget have been left screeching irrelevantly from the sidelines, isn’t just satisfying to see. It suggests a big move in the center of gravity of economic policy debates.”

|

|

|

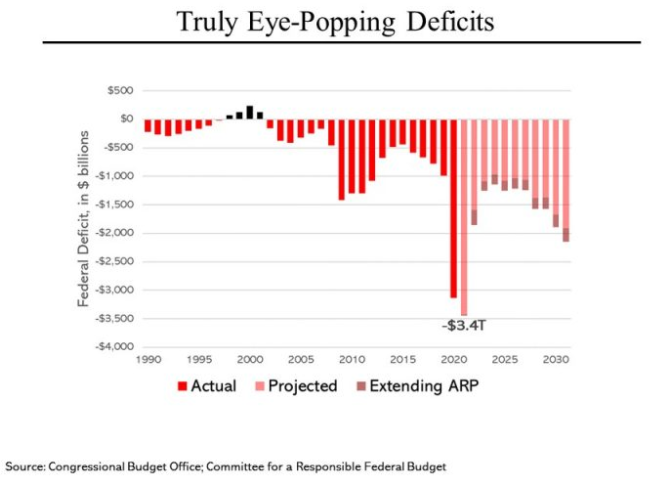

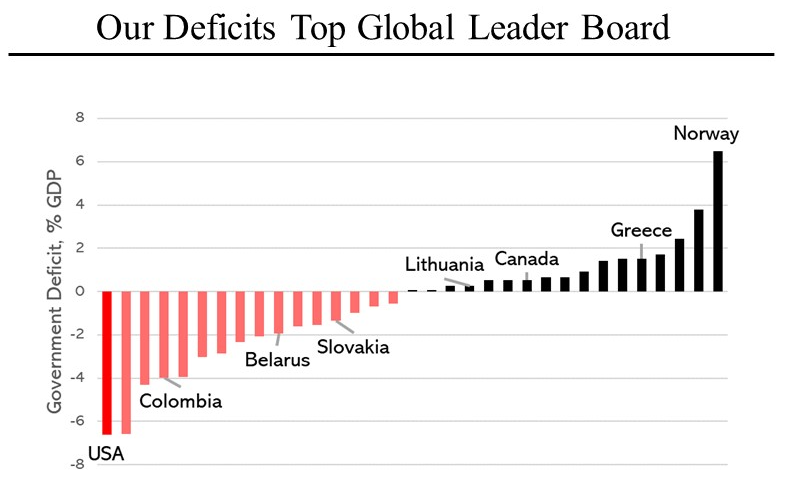

Charts of the Day

On Wednesday’s edition of MSNBC’s Morning Joe, Steven Rattner, an investment manager who was the Obama administration’s “car czar” in charge of the 2009 auto industry rescue, sought to put the U.S. budget deficit into some historical and global perspective.

“In just two years, we will have amassed deficits of $6.5 trillion, 50% more than the combined budgetary deficits from 1965 to 2005, after we first lost our fiscal discipline around the time of the Vietnam War,” Rattner writes. “How have we amassed such a large debt burden compared to other countries? In part because we can. As the world’s reserve currency, investors have been willing to buy our debt; a third of it is held by foreigners, led by Japan and China.”

|

|

| | | | | | |

|

|