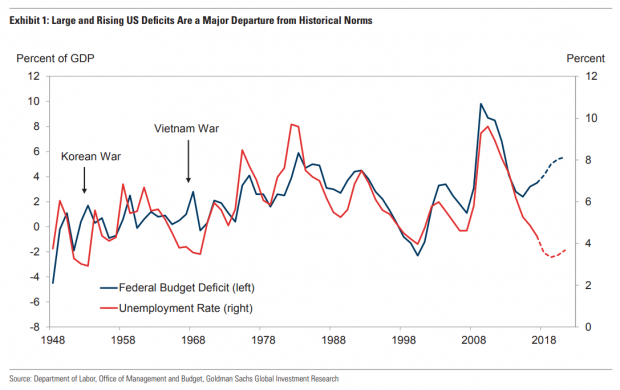

In a note to clients on Saturday, Goldman Sachs economists say that the larger deficits resulting from Congress’ recent tax cuts and spending increases could drive interest rates higher in at least a couple of ways: First, the federal reserve will likely raise rates. “The sizeable demand boost provided by the recent deficit-increasing tax cuts and spending cap increases at a time when the economy is already somewhat beyond full employment is a striking departure from historical norms that is likely to contribute to further overheating this year and next and tighter monetary policy in response,” Daan Struyven and David Mericle write.

Second, as the U.S. Treasury pumps up its bond issuance in response to the rising deficits — and with the Federal Reserve no longer on its bond-buying spree — investors may seek a higher premium for absorbing that larger supply of debt.

Just how high will interest rates climb? Goldman projects that the yield on the benchmark 10-year Treasury will rise from just under 3 percent now to 3.6 percent by the end of 2019.

The Goldman economists used a few approaches to try to tease out the deficit effects on interest rates. We’ll spare you all the details and just tell you that Goldman estimates that a 1 percentage point increase in the budget deficit results in a rise in 10-year interest rates of about 20 basis points (or 0.2 percentage points). Applying that estimate to the deficit increases resulting from tax cuts and spending hikes — roughly 1.5 percent of GDP combined — results in an overall projected rise in 10-year interest rates of 0.3 percentage points. In other words, rising deficits account for about half of Goldman’s projected increase in the 10-year yield.

Goldman’s economists note that the timing of this rise in rates is uncertain — but that Treasury markets haven’t yet fully appreciated how strong the effect of rising deficits will be.