About $364. That’s how much Americans’ income taxes will go up, on average, as a result of the fiscal cliff deal passed by Congress late last night, according to the non-partisan Tax Policy Center.

That average is fairly meaningless, though. While nearly everyone will end up paying more to the federal government, the real brunt of the income tax hit will be felt by less than 1 percent of American households.

Under the deal, tax rates will revert from 35 percent to the Clinton-era 39.6 percent on those with adjusted gross incomes of $400,000, or $450,000 for married couples. Among other changes, personal tax exemptions and itemized deductions will be phased out for individuals with incomes above $250,000 or couples making more than $300,000.

At the same time, the deal also means that a large majority of households will see their paychecks shrink because of the expiration of the payroll tax holiday. On average, households will pay about $720 more than they would have if the payroll tax had been extended. On the other hand, the average household will save $1,847 compared to the tax bill they would have paid if Congress had not reached a deal. Compared to what might have been without the agreement, the top 1 percent of earners just got an average tax cut of nearly $26,000 – and millionaires got a tax cut of almost $39,000.

In the end, about 0.7 percent of households will see their income taxes rise, according to a preliminary analysis by the non-partisan Tax Policy Center. Yet a much higher share of households – 77.1 percent – will be paying more money to the federal government because the payroll tax used to fund Social Security will go back from 4.2 percent to 6.2 percent in earned income up to $113,700. With that tax reverting to its prior rate, households earning $50,000 will pay $1,000 more, and those making $100,000 will see their paychecks reduced by $2,000 compared to 2012. In all, the expiration of the payroll tax holiday is expected to raise $126 billion.

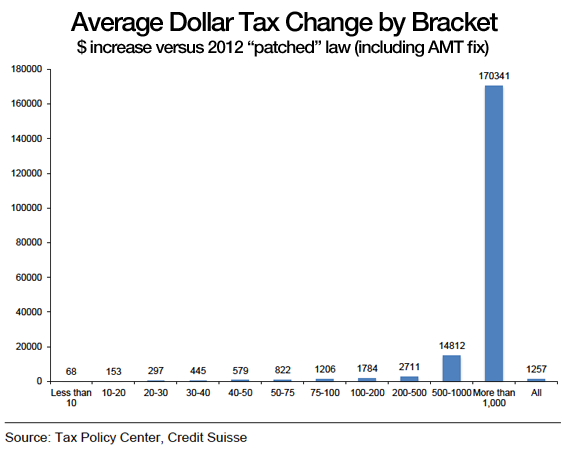

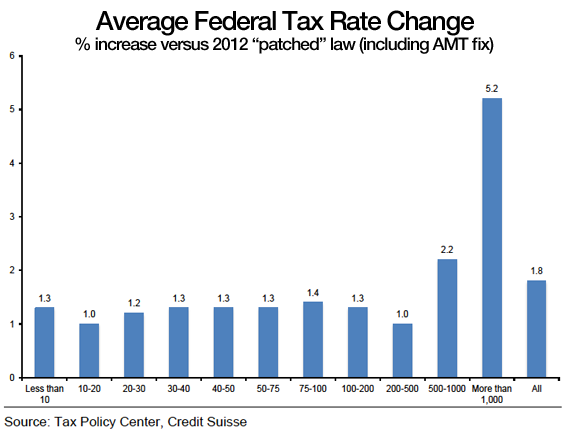

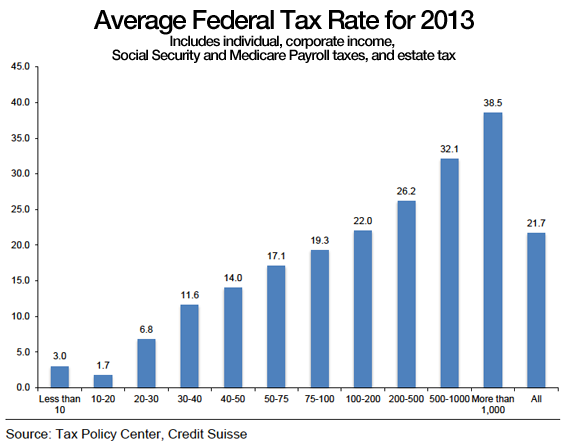

The four charts below may provide a better sense of how the tax deal will affect people across income levels. The charts, from Credit Suisse and based on data from the Tax Policy Center, present averages, but they clearly show that total after-tax income will drop across the board. The biggest hit, though, will be to households making more than $500,000.

To get more detail on how your own tax bill will change, try the Tax Foundation’s Tax Policy Calculator.