Just how tight is the job market? The fate of millions of unemployed workers hinges on the answer to that question, as does the timing and pace of the Federal Reserve’s interest rate hikes.

We’ll get our next reading on the labor market on Friday, and economists on average expect that the unemployment rate will stay at its current 5.5 percent, down from 10 percent at its recent peak in October 2009. But those economists by and large also expect unemployment to keep tumbling over the rest of the year, dropping below 5 percent well before the calendar turns to 2016.

Related: The Middle Class Is Struggling in All 50 States

That level is important because it represents the lower end of the Federal Reserve’s newly reduced estimate of something called the non-accelerating inflation rate of unemployment (NAIRU) — essentially, full employment consistent with a healthy economy. An unemployment rate that falls even further would signify a labor market that has potentially tightened to the point that employers must start offering higher wages to recruit and keep workers, eventually leading to higher prices.

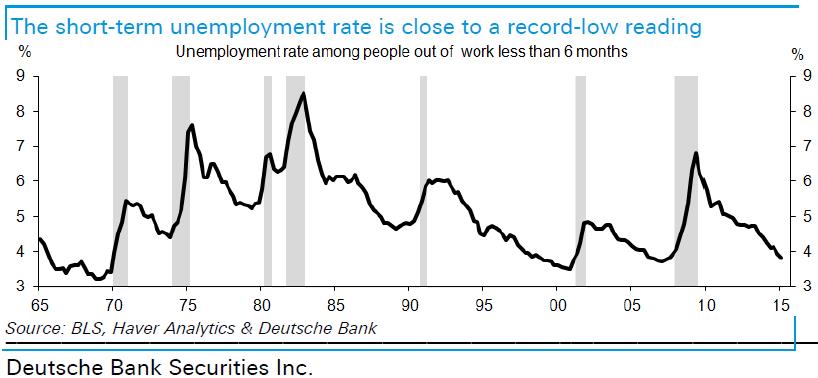

In a note to clients today, economists at Deutsche Bank pointed out that another, admittedly narrower measure suggests that the job market is even tighter than the headline unemployment rate indicates. The unemployment rate among workers who have been out of a job for six months or less is down to 3.8 percent, they note, which is where it was in 2006 and 2007. The only time since the late 1960s that the short-term unemployment rate has been lower was in 1999-2000, when it averaged 3.6 percent.

“The reason this matters is that underlying wage pressure may be largely a function of what happens to short-term unemployed,” Deutsche Bank’s Joseph LaVorgna and Brett Ryan wrote. “Once the unemployment rate among people out of work less than six months falls to an extremely low level, as it recently has, employers may be forced to bid up increasingly scarce skilled labor.”

Related: Macro Wars — The Attack of the Anti-Keynesians

By contrast, the unemployment rate for Americans out of work six months or longer, at 1.7 percent, remains well above its pre-recession norm. “However,” LaVorgna and Ryan write, “this latter group may be less important to the wage-setting process if labor costs are determined largely by the demand for skilled workers or those that can readily find employment.”

The point is that purely in terms of the job market, wage pressure and inflation, the job market may already be even tighter than it looks. “It is possible the economy is already at, or even through, the NAIRU. If this is the case then wage growth should noticeably accelerate over the coming quarters,” Deutsche bank’s economists wrote.

From the perspective of Fed Chair Janet Yellen, that may not be such a bad thing, though. In a speech last week, Yellen said that the economy still has a way to go before reaching maximum employment. But she also laid out an argument for why the Fed would take a “gradualist approach” to normalizing monetary policy — even with the potential risks of moving too slowly, including a possible surge in inflation and an excessive buildup in leverage as a result of persistently low interest rates. Among other things, Yellen said that a tight labor market could reverse some economic damage lingering from the financial crisis.

Related: Bernanke Says He Didn’t ‘Throw Seniors Under the Bus’

“The deep recession and slow recovery likely have held back investment in physical and human capital, restrained the rate of new business formation, prompted discouraged workers to leave the labor force, and eroded the skills of the long-term unemployed,” she said. “Some of these effects might be reversed in a tight labor market, yielding long-term benefits associated with a more productive economy.”

The good news for workers in all of this is that, sooner or later, wages are going to start to rise.

Top Reads from The Fiscal Times: