This may have been forgotten over time, but one of President Obama’s main selling points in promoting expanded Medicaid coverage for low-income Americans as part of Obamacare was that it would ease the financial worries of millions of people. As the president said in a 2015 weekly radio address promoting his controversial initiative, “That’s the whole point of health insurance: Peace of mind.”

The administration’s drive to persuade states to expand the rolls of poor people eligible for health care coverage narrowly survived a 2012 Supreme Court challenge and strong opposition from Republicans governors and state legislatures throughout the country. Today, 31 states and the District of Columbia take part in the federally-funded program that is targeted to assist all adults with incomes up to 133 percent of the poverty level.

Related: Even With Obamacare, 29 Million People Are Uninsured: Here’s Why

A new study by the Federal Reserve Bank of New York released this week confirms that the expanded Medicaid plan has indeed eased the financial anxiety of millions of poor people, primarily by reducing the size of debts sent to collection agencies.

The report, prepared by economic analysts Nicole Dussault, Maxim Pinkovskiy and Basit Zafar, says that the main role of programs like Medicaid is “not to protect our health per se, but to protect our finances.”

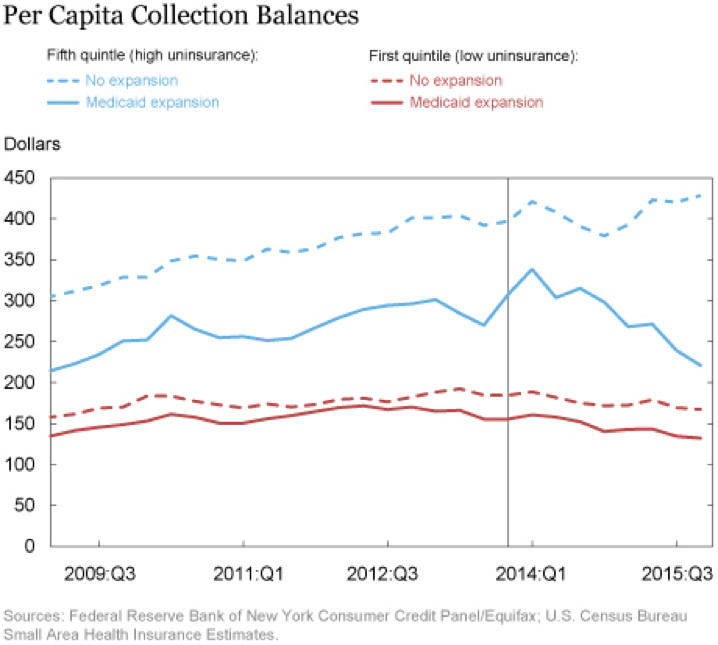

Drawing on data from the first quarter of 2009 to the fourth quarter of 2015, the Federal Reserve Bank analysts found “suggestive evidence” that “counties with a high un-insurance burden pre-reform in states that subsequently expanded Medicaid had a decrease in average debt sent to collections agencies compared with such counties in states that did not expand Medicaid.”

Indeed, by the fourth quarter of 2015, collections declined on average by more than $100 per capita in the counties that benefited the most from the Medicaid expansion in relationship to less affected counties. That may not seem like a lot of money, but the Fed researchers say that is a “sizable decline” because the mean average of collection balances over the same period is $280.

Related: The Hidden Costs of Rejecting Medicaid Expansion

The research was based on data from the Federal Reserve Bank of New York’s Consumer Credit Panel, which includes many financial indicators for individuals throughout the country. The report focused on the total balances that were sent to a private collection agency within a 12-month period. The working hypothesis was that Medicaid expansion should have had a much larger impact on counties that had a high un-insurance rate prior to implementation of the health care law.

The researchers used 2013 uninsured rate distributions to create five uninsured rate quintiles. Counties that fell within the first quintile has the lowest uninsured rate (14.5 percent) while counties in the fifth quintile had the highest 2013 uninsured rate (29.8 percent) – and presumably would experience the most dramatic beneficial impact under Medicaid expansion. And, in fact, they did.

“While the full effects of the Affordable Care Act on financial health are yet to be seen, and while the effects of the ACA—positive or negative—are not restricted to financial health, we offer suggestive early evidence that the Medicaid expansion is fulfilling the goal of health insurance: providing ‘peace of mind’ by protecting against financial hardship,” the study concludes.

The researchers note there are other trends that may boost the “peace of mind” theory, although the findings are less conclusive. One has to do with trends in credit card balances per person, which suggest that the average per capita credit card balances have declined in the counties where residents benefit most from Medicaid expansion.

Related: How Obamacare Could Backfire on Hillary Clinton

“The estimate in the fourth quarter of 2015 indicates an average decline of a little less than $200,” the report states. “For comparison, over the sample period, the mean per capita credit balance is $2,614, with a standard deviation of $914.”