One major selling point of the Republican tax overhaul, which lowered the corporate tax rate to 21 percent and sweetened the rules for capital expensing, was a promised boost in investment by U.S. firms. A jump in capital expenditures would boost economic growth, supporters of the legislation said, and in the long run provide the basis for higher productivity and increased pay for American workers.

However, according to a new research paper from the International Monetary Fund, there is still

no consensus on whether that investment boost has in fact occurred. Outgoing White House economic adviser Kevin Hassett has linked better-than-expected GDP growth to a rise in business investment spurred by the tax cuts, but many analysts outside the Trump administration say the evidence is weak to nonexistent.

Reviewing the economic data since the passage of the tax overhaul, the IMF researchers said that while business investment did grow in 2018, the cause has been “the strength of expected aggregate demand” rather than changes in the tax code. In other words, U.S. firms spent more on capital investments because business was good and improving, not because the tax rules suddenly changed. And although there has been a jump in investment, the increase falls short of the levels predicted by economic models, the analysts said.

Why has investment fallen short? The researchers said that increased corporate market power has played an important role. Market power produces higher margins for dominant firms, which makes them less sensitive to policy changes such as a lower tax rate, the researchers found. Uncertainty over trade policies also played a role, depressing corporate investment as executives waited to see how the Trump administration’s tariffs and trade deals played out.

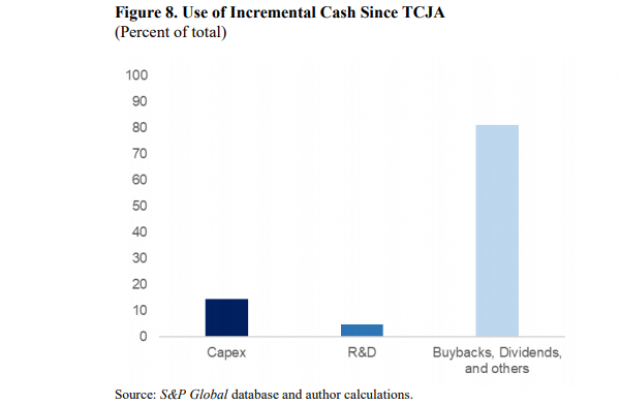

As a result, only about 20 percent of the tax-cut windfall has gone toward capital investment and R&D spending, the researchers said (see the chart below). The rest has gone mostly toward “share buybacks, dividend payouts, and other asset-liability planning and balance sheet adjustments.”