Even as outsiders line up to get a piece of Facebook, the social media giant’s latest filing shows that early individual and institutional investors will be selling nearly 84 million more shares than originally planned. And even as the frenzy surrounding the offering builds – or perhaps because of it – Facebook is facing renewed scrutiny over its business model and the risks it faces.

The company revised its S-1 filing with the Securities and Exchange Commission twice in two days this week, with the latest document reflecting new plans to sell more than 421 million shares, up from 337.4 million, as early investors look to cash out more of their holdings. Those investors would face a lockup period of at least 91 days during which they could not sell once the stock is publicly traded.

In an earlier revision, Facebook upped its target price range from the original $28 to $35 a share to $34 to $38 a share. The final pricing will be determined later today with the stock expected to begin trading tomorrow. If the shares are sold for $38 apiece, Facebook would raise more than $16 billion, or $18.4 billion if the entire overallotment – additional shares made available to the underwriters – is sold. That would make Facebook’s the third-largest IPO in U.S. history. At an offering price of $38, the company would be valued at $104 billion.

RELATED: Before Facebook: The 14 Biggest IPOs in History

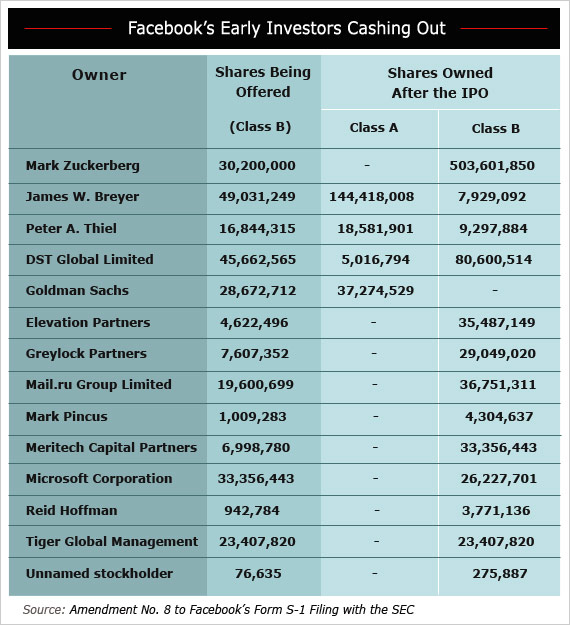

Some of Facebook’s biggest early backers have significantly increased their planned sales. Investor James Breyer and his venture firm Accel Partners, for example, will be selling 49 million shares, up from 38.2 million. Breyer, who sits on Facebook’s board of directors, would still own more than 150 million shares of the company after the IPO. DST Global, an investment firm founded by Russian billionaire Yuri Milner, will be selling almost 46 million shares, some 19 million more than previous plans showed. Billionaire venture capitalist Peter Theil, a co-founder of PayPal and member of Facebook’s board, will be selling nearly 17 million shares, more than twice the 7.75 million he had been slated to sell in previous filings. Goldman Sachs now intends to sell nearly 29 million shares, up from 13.2 million. And Tiger Global Management, a hedge fund run by 36-year-old Chase Coleman, intends to sell 23.4 million shares, up from 3.4 million.

Facebook CEO Mark Zuckerberg is still slated to unload 30.2 million of his more than 533 million shares, or less than 6 percent – a sale that would bring in nearly $1.15 billion if the stock prices at the high end of the new range. But Zuckerberg’s power over the company would be lessened just a bit because of the increased sales by investors who had given him proxy control over their stakes. The 28-year-old would have total voting power of about 57.5 percent, down from 58.8 percent under the previous filing. Zuckerberg’s remaining stake in the company would be worth more than $19 billion.

So Zuckerberg would catapult into the ranks of the country’s wealthiest people – but as the song goes: more money, more problems. (Ok, we know that’s not exactly it, but it’s close enough.) Facebook’s 171-page prospectus includes the usual section about risk factors the company and its investors might face – but the section runs a full 23 pages.

Those potential problems include both consumer and business factors. On the consumer side, the company has grown to more than 900 million active users a month, but acknowledges that it will get harder to keep attracting and engaging users at the same swift rate. The prospectus doesn’t mention previous Internet darlings like MySpace or Friendster by name, but notes: “A number of other social networking companies that achieved early popularity have since seen their active user bases or levels of engagement decline, in some cases precipitously. There is no guarantee that we will not experience a similar erosion of our active user base or engagement levels.” Already, an Associated Press-CNBC poll finds that 51 percent of adults under age 35 and 46 percent of adults overall say Facebook is a fad that will fade as new things come along.

And, as many others have noted, Facebook was upfront about the challenges it faces as consumers increasingly move to mobile devices. As the prospectus puts it: “If users increasingly access Facebook mobile products as a substitute for access through personal computers, and if we are unable to successfully implement monetization strategies for our mobile users, or if we incur excessive expenses in this effort, our financial performance and ability to grow revenue would be negatively affected.”

On the business side, Facebook must still show that it can deliver exactly what advertisers want. “Many of our advertisers spend only a relatively small portion of their overall advertising budget with us,” The prospectus notes. “In addition, advertisers may view some of our products, such as sponsored stories and ads with social context, as experimental and unproven.” Or worse: They could conclude that those ads are ineffective, as General Motors did in deciding this week to discontinue advertising on Facebook.

Given those uncertainties, and the others that the company will have to contend with, maybe it’s worth bearing in mind the moniker that’s generally used to refer to insiders and institutional investors like the ones who are now cashing out more of their Facebook stakes: “the smart money.”