|

Consumers are struggling. The housing market is in worse shape than ever, and manufacturing is fading. Economic growth is far undershooting the upbeat expectations at the beginning of the year, even as global growth is slowing sharply. Now, amid new signs that job growth is cooling off, the first-quarter’s weakness is extending into the second quarter, and economists are once again ratcheting down their 2011 forecasts. Is the recovery in trouble?

It’s a wave of worry that’s giving investors agita. Stock prices have tanked more than 5 percent since early May, as economic data turned sour, and it looks like the economy’s woes run deeper than expensive oil and Japanese supply disruptions. The growing fear is that troubles in consumer spending, housing and job creation could limit growth for some time. The fiscal stimulus and monetary support offered by policymakers -- have not resulted in the level of economic growth that would create jobs, and it’s not likely that the government will open it’s checkbook again anytime soon.

Consumers, who are central to solid and sustained growth, are at the heart of the new worries. Their pullback is a big reason why the economy is slowing down, and it’s not just because of high gas prices. Labor markets are not generating income at a rate fast enough to support a healthy pace of spending. The Labor Dept. last week reported that U.S. payrolls increased by a slim 54,000 workers in May, suggesting new hiring caution amid slower growth. Labor also revised March and April job gains downward, and the unemployment rate headed back up, to 9.1 percent last month, from 9 percent in April and 8.8 percent in March.

A new survey by Newsweek/Daily Beast says Americans are angry and nervous about the economy and are losing faith in the government’s ability to create jobs. “Americans are angry about the economic situation facing the country. Sixty-five percent say that they are angry that the economy is stagnating while big corporations are posting record profits.

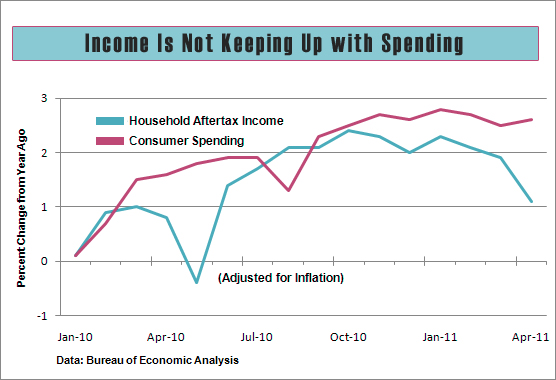

Even before the jobs report, last week’s GDP data showed a sharp downward revision to household income, a big factor in the recent lowering of second-quarter forecasts for economic growth by J.P. Morgan, Barclay s Capital and other big banks. After taxes and inflation, income has grown at a paltry annual rate of only 0.8 percent since last September. Income hasn’t grown at all since December, despite the $110 billion boost in January from lower payroll taxes, and the latest jobs numbers do not bode well for any great pickup in the second half.

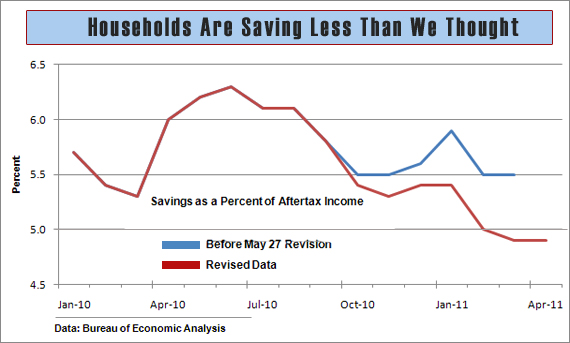

Weak income growth may be creating another problem: “Households have only maintained spending as well as they have by reducing the saving rate,” says J.P Morgan economist Robert Mellman. Since September, inflation-adjusted consumer spending grew at a 3 percent annual rate, three times faster than income. In less than a year, savings have dropped by $149 billion, from more than 6 percent of income to only 4.9 percent in April. New consumer caution resulting from weaker job markets or falling stock prices could give households cause to rebuild their savings in the second half—at a cost to spending and economic growth.

The new anxiety may start with consumers, but it doesn’t end there. The record low for home prices in March is a sign that any housing recovery is still a long way off, and that massive policy efforts haven’t helped. Historically, housing construction has directly added anywhere from 0.5 to more than 1 percentage point to economic growth in the years immediately following a recession, and that doesn’t include the knock-on effects, such as greater demand for home-related goods and services. Even when housing begins to recover, the impact will be much smaller than in the past, since construction’s share of GDP is now less than half of what it was five years ago.

The industrial sector has a major role in the slowdown story, and the auto industry could play a big part, especially in the second quarter. Economists at UBS estimate that a combination of weaker demand and supply shortages could subtract as much as 1 percentage point from second-quarter GDP growth. May sales fell to an 11.8 million annual rate from 13.1 million in April. At least some of the drop was due to a lack of Japanese brands, which would suggest a sales rebound later in the year, but that’s no sure thing, if cooler job growth gives potential car buyers pause.

However, the manufacturing slowdown goes beyond autos, and it’s global. Some of the loss of momentum reflects the direct and indirect effects of the Japanese earthquake, not only in the U.S. but across Asia, say global economists at J.P. Morgan. In addition, businesses are reining in their production now that inventories, depleted during the recession, have been rebuilt to levels needed in a growing economy. How quickly global growth snaps back will be determined by the strength of Japan’s production rebound and whether or not the pace of global demand holds up, say the Morgan analysts.

A similar dynamic is at work in the U.S. economy, but future demand is a more crucial issue. Last year, inventory restocking contributed almost half of the economy’s 2.9 percent growth rate. Now, with inventory needs largely sated, further growth in output and employment will depend more on the pace of spending. And there’s the rub. During the recovery, which is nearly two years old, overall spending by consumers, businesses, governments and foreign buyers has grown at a tepid 1.8 percent annual rate, and the pace slowed sharply in the first quarter, to 0.6 percent.

Inventories may have grown too fast last quarter, which could feed the slowdown, as a reduced rate of ordering, production, and employment in the months ahead cut further into economic growth. Business stockpiles grew three times faster last quarter than they did in the fourth quarter, as production ran far ahead of sales. Recent reports show that factory orders plunged in April, and the nation’s purchasing managers reported a steep drop in manufacturers’ ordering and production in May.

This year’s economic slowdown is yet another reminder that the U.S. economy remains severely out of balance after the shock from the 2007-09 recession. In particular, the problems in jobs, housing, and the federal deficit have become structural, says Wells Fargo chief economist John Silvia, and not easily addressed by a traditional recovery. That puts economic policy at the forefront of any solution. But Washington seems unlikely to be of much help in the coming year, which means the economy will have to wobble along the best it can on its own.

Related Links:

Economic Woes Give Republicans Early Campaign Focus (CNN.com)

As Job Growth Slows, Obama’s Economic Policies Come Under Attack (Neon Tommy)