Perhaps it’s vertigo?

Stocks on Wednesday retreated somewhat from their recent record highs – in the case of the Dow Jones Industrial Average, it recorded new closing and intraday highs – while some fretful traders have been heard mumbling about the failure of the Standard & Poor’s 500 index to break above 1,700 points, a technical barrier that is widely viewed as a psychologically important milestone.

Don’t worry; be happy. It’s likely to be a case of the old French maxim at work: reculer pour mieux sauter. (Roughly translated, taking a step backward in order to better jump forward.)

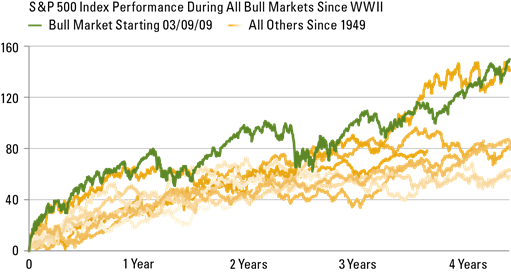

As much as the stock market rally remains unlovable, it also remains unquenchable. Indeed, according to Jeffrey Kleintop, chief market strategist at LPL Financial, it now is the strongest bull market recorded by the S&P 500 since the end of World War II.

*Source: Bloomberg, LPL Financial Research 06/14/13

As Kleintop notes, stocks have accomplished this in the face of some of the most astonishing headwinds imaginable: the European fiscal debacle, the slowdown in China’s economic growth, geopolitical flare-ups, budgetary standoffs in Washington and, more recently, rising interest rates.

In his just-published travel narrative The Longest Road, Pulitzer Prize-winning novelist and journalist Philip Caputo thinks back to 1980 and just such another paradox. When Ronald Reagan proclaimed that “it’s morning in America,” Caputo muses that “a realist would have looked at the country then – suffering from double-digit unemployment and double-digit inflation, still embittered by its first lost war, humiliated by the hostage crisis and the disastrous rescue attempt in Iran – and scoffed.”

Somehow, bullish visions have a way of turning into reality. Reagan, Caputo says, may have been selling illusion, but “Americans bought it because that’s what they wanted to believe. If you believe it, it will happen, and lo, it did.”

Admittedly, prosperity post-Reagan has been a radically different proposition, one characterized by the disappearance of blue-collar jobs and a widening of the wealth gap in the country. But for stock market investors, that was a great bull market to ride, and Kleintop suggests that the more we turn up our noses at the current bull market – investors and insiders have been net sellers of stocks in recent months; the sentiment indicators signal a below-average proportion of investors are bullish – the stronger it seems to get.

Since Federal Reserve Chairman Ben Bernanke spooked investors back at the end of May by talking about tapering off the Fed’s support for the fixed income market (and thus for ultra-low interest rates), the S&P has not only regained all the ground it lost in the immediate aftermath of that speech but added another 2.6 percent to bring its year-to-date gain to around 19 percent.

The most recent set of new highs is just one instance of the market’s apparent determination to move stubbornly higher. Let’s face it: Second-quarter corporate earnings haven’t exactly been overwhelming. Thus far, the estimated S&P earnings growth is up 3.8 percent, while the revenue growth estimate provided by Thomson Reuters is a mere 1.6 percent. Meh.

The results have in many cases come in ahead of analysts’ expectations (65.7 percent positive surprises so far, according to Thomson Reuters I/B/E/S), but they are often doing so on the back of forecasts that were trimmed in the weeks and months leading up to those announcements. And that surprise rate? It may be better than the 64 percent average in the 19 years for which Thomson Reuters has accumulated data, but it’s not as robust as the 67 percent beat rate in the last four quarters.

But this is where a cliché demonstrates how it came to be a cliché. In this instance: “In the kingdom of the blind, the one-eyed man is king.”

While the U.S. economy has its problems, growth is positive, the market is liquid and reasonably transparent (in spite of the raft of insider trading lawsuits brought by the SEC) and the country is stable (notwithstanding the occasional saber-rattling by those ready to take up arms in the face of what they see as incursions on their rights by federal authority).

There is a reason why Moody’s not only affirmed its AAA rating on the U.S. sovereign debt, but also raised its outlook from negative to stable. While growth may be, in absolute terms, underwhelming, it’s still far faster than other countries that also have a AAA rating, “and has demonstrated a degree of resilience to major reductions in the growth of government spending,” Moody’s said in the statement announcing its decision.

There are two caveats to keep in mind, however. First of all, while the U.S. economy and stock market are outperforming many of their peers right now, that won’t always be true. That means that it’s important to keep your portfolio balanced and perhaps to keep an eye open for quality stocks domiciled outside the United States that still trade at a discount.

The other reality to bear in mind is that just because the stock market is on a tear doesn’t mean that all of its components will follow suit. If you’re picking stocks or investing with stock-pickers in mutual funds, keep a close eye on the fundamentals of each individual company and the track record of the manager you have chosen. If there is one thing that is more painful than losing money outright, it is what you experience when your portfolio flatlines during a period in which the S&P 500 is surging ahead and delivering double-digit gains to index investors.

You don’t need to expect that you collect precisely what the S&P 500 delivers, but you don’t want to walk away with a 5 percent return in a year that the market was up 20 percent or more, without a very good reason for that.