There's just no other way to say it: Investors have lost that lovin' feelin' for the stock market.

Yes, the Nasdaq 100 pushed to a record high last Monday thanks to a surge in widely owned and widely recognized stocks like Alphabet (GOOGL) and Amazon (AMZN), but both the Nasdaq and the broader market have slumped since then. The broader point remains: Regular Americans just aren’t wild about keeping their money in the market.

Maybe it's because of a lack of gains outside the flashy tech stocks: The Dow Jones Industrial Average has been trading in a tight range for a couple of months, capping a year-long flirtation with the 18,000 level that was first reached way back in 2014. Or maybe it's something deeper.

New research from the Federal Reserve shows there have been net cash outflows from U.S. domestic equity funds every month between March 2015 and August 2016. The outflows have been large, averaging nearly $18 billion each month for a total outflow of $310 billion over the last year and a half — driven, overwhelmingly, by ordinary households.

Related: It Looks Like Investors Have a Clear Favorite in the Election

It's not just ordinary investors, however. Even professional fund managers are increasingly giving up on this market, in which inter-market and cross-asset correlations are extremely high, thanks in large part to years of aggressive monetary policy stimulus and ultra-low interest rates.

In plain English: When stocks of different types (both cyclical and defensive) and assets of different types (bonds, stocks, commodities and currencies) increasingly move in lockstep, it’s massively difficult for Wall Street pros to get an edge. It also reduces the risk protection offered by portfolio diversification.

That’s especially true now since asset prices seem to depend less on fundamentals like earnings and economic growth and more on event risks, with a binary outcome to headline-making news like the Brexit vote, the U.S. fiscal cliff debacle and the upcoming U.S. presidential election.

Related: Is Trump Pulling Ahead? Here’s What the Polls Are Really Saying

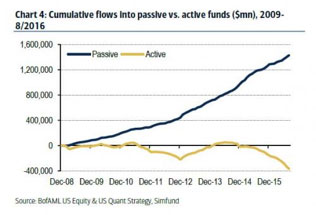

Credit Suisse research from earlier in the year showed that U.S. active investment managers — the highly paid "pros" — were simply buying "the market" on a scale not seen since 2008. In other words, they weren't trying to find undervalued stocks or chase momentum. They were simply giving up and getting exposure to the entire market by indexing. That's boring, to be honest. And for most small investors, it means paying extra in fees for the same stocks they could have owned through some low-cost ETFs. According to Bank of America Merrill Lynch, just 18 percent of active large-cap funds outperformed their market benchmark in the first half of the year compared to 61 percent in 2007.

No surprise then that active funds have been the epicenter of investor outflows, as shown below, as investors have decided to switch to lower-cost indexing.

With everything in stasis, trading activity has slowed, further perpetuating the idea of a staid stock market.

Related: 7 Big Risks That Could Derail the Stock Market’s Rally

Daily trading volumes in October were dismal. Jason Goepfert at SentimenTrader noted about a week ago that volume was on pace to be the lowest in 40 years, as trading activity was running about 17 percent below the average monthly volume for the year — something that hasn't happened in the normally exciting month of October since 1976.

The result has been a deepening sense of apathy. The percentage of bulls in the American Association of Individual Investors sentiment survey has been below 40 percent for nearly every week over the past year. The only other times this has happened over such a long period all came more than 25 years ago. The last new high for the S&P 500 was on August 15, yet the index has remained within 3 percent of that level since then. Such a long, flat, sideways skid has never happened before.

Until valuations become more attractive, and asset correlations return to normal, it's hard to see a reason for these patterns to change.