Things are moving fast in Washington, D.C.: Just over the last 24 hours, the Justice Department appointed a special counsel to look into the situation while Reuters is reporting Trump's campaign had at least 18 undisclosed contacts with Russia.

As a result, the 20-percent-plus post-election rally in stocks is under threat and U.S. equities on Wednesday suffered their worst one-day selloff since last September before rebounding a bit on Thursday.

The pain could get even worse for key sectors of the market.

For Wall Street, the concern is that the political blowback will threaten Trump's pro-growth legislative agenda. Hopes for quick action on tax cuts, infrastructure and certainly health care reform are dimming fast.

Related: How Millions of Aging Baby Boomers Could Bust the Economy

Both Wall Street's weakness and Trump's political headaches look like they are just getting started. The percentage of S&P 500 stocks in uptrends, shown in the chart below, broke below its six-month range and dropped to 69 percent vs. a high of 80 percent in March. Yet the S&P 500, for now, remains within the confines of a four-month trading range. That suggests the selling pressure could intensify before sentiment is sufficiently wiped out.

Looking back on the market's behavior over the past six months, it's clear that sentiment had become overextended and downright frothy. The surge to new stock market highs simply wasn't justified by the fundamentals.

Earnings expectations have been coming down as the boost from last year's energy price rebound fades. The "hard" activity-based economic data has been weak for months, but now even survey-based "soft" data is rolling over as hopes of a second-quarter GDP rebound fade. Even the bond market has been warning of trouble, with the U.S. 10-Year Treasury yield declining from a mid-March high of 2.62 percent to a low of 2.18 percent in the middle of April. Yields on the 10-year are now around 2.23 percent.

Related: How Political Fireworks in Washington Could Singe the Market Rally

Above all, investors are finally waking up to the fact that U.S. policy uncertainty remains high, with big, meaty issues like the 2018 budget, geopolitical hotspots and health care unresolved.

As the market turns, financial stocks are leading the way down. The odds of a Federal Reserve interest rate hike in June fell to 65 percent on Wednesday (from 88 percent one week ago) and long-term bond yields dropped. As a reminder, big bank stocks were among the leading gainers after Election Day as investors priced in hopes of higher net interest margins built on expectations for higher inflation, higher interest rates and higher economic growth under the new president. The prospect of regulatory reform also helped.

Now, big banks look especially vulnerable.

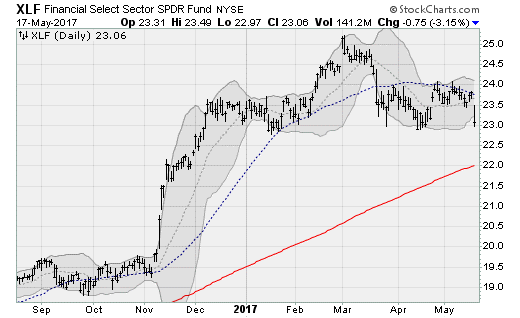

The Financial Select SPDR (XLF) gained nearly a third from its November low to its March high. The ETF, which provides exposure to the financial stocks in the S&P 500 index, has traced out an epic head-and-shoulders reversal pattern — one of the best-known formations among technical analysts. The "neck line" at $23 represents critical support. A breakdown would trace a downside price target of $21, which would represent a violation of the 200-day moving average (an important long-term trend measure) for the first time since last July.

Related: Killing Banking Rules Will Invite a Whopper of a Recession

With "Sell in May" seasonality in the air, Jeff Hirsch of the Stock Trader's Almanac notes that the S&P 500's last correction ended on Feb. 11, 2016, ending a 14.2 percent decline.

Another correction is possible here — and a full-on wipeout of the 20 percent post-election gain isn't out of the question either, given that post-election gains in the U.S. dollar and in the 10-year yield have already been fully reversed.