The Federal Reserve just raised interest rates for the second time in three months, signaling a dramatic quickening of its prior pace.

For the first time in more than a decade, Fed policymakers are turning increasingly hawkish out of concern over ongoing labor market tightening, evidence of building inflationary pressure and the surge of business, consumer and investor sentiment following the surprise election of President Donald Trump.

This hawkish turn — a typical late-cycle move by central banks — is made unique by the fact that Wall Street has surged in recent years thanks to an unprecedented monetary stimulus. Never in recorded human history have interest rates been as low as they've been in recent years.

Related: Why So Many CEOs Are Cozying Up to Trump

Higher interest rates nearly always result in recession and bear markets (with only a few "soft landings" the exception). But now, with asset valuations across the spectrum stretching into questionable territory even as price volatility remains extremely low, one wonders: Will this Fed tightening result in something much worse?

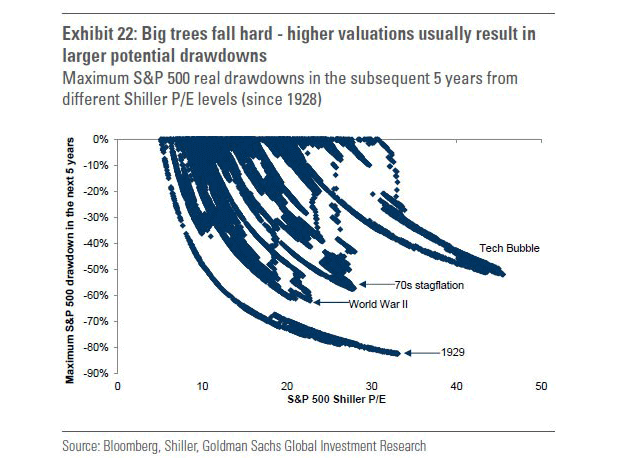

Nearly every segment of the market is expensive. U.S. equity valuations have only been higher during the run-up to the 1929 and 2000 market crashes. Bond yields remain low and bond spreads remain compressed. Commodity prices have rebounded from their early 2016 lows.

But vulnerabilities are appearing. Crude oil is sliding further below the $50-a-barrel threshold as inventory and oversupply concerns reappear. High-yield corporate bonds are selling off in sympathy, as investors once again worry about the solvency of high-cost U.S. shale producers.

Related: Why Oil Prices Are Tanking — and Where They’re Headed Next

A turnabout, if that's what this is, is in a very early state: The Bank of America Merrill Lynch High Yield B Effective Yield stands at 6 percent, up from a post-election low of 5.5 percent but well off the high of 10.2 percent hit in February 2016 as energy prices were bombing out.

Yet Wall Street is beginning to sound the alarm as inflation heats up. On Tuesday, the latest producer price inflation data showed inflation is running at its fastest pace in five years. Consumer price inflation has also been on the rise, driven by higher shelter costs, among other things.

Goldman Sachs strategist David Kostin wrote in a note to clients last weekend that investors "will soon capitulate on their expectation of upside" to their earnings growth forecasts for the year. Part of the reason is that the tax cuts expected from the Trump administration are increasingly unlikely to occur before 2018.

Related: Americans’ Household Wealth Hits a New High

In a note on Tuesday, Kostin expanded upon this outlook by downgrading equities outright. He warned that, with "growth momentum nearing its peak and rates increasing further with a hawkish Fed," the balance of risk for investors looks increasingly negative. The risk is made worse by elevated valuation levels, which as noted in the chart below, have historically led to larger and more painful selloffs.

Goldman economists have penciled in three rate hikes for 2017, to come in March, June and September. They also expect the Fed to start its balance-sheet normalization — that is, the process of reversing the heavy bond-buying done under the QE1, QE2 and QE3 programs — sometime in the fourth quarter.

Investors are ill prepared for a big breakout in volatility, as large-cap stocks have now gone more than 100 days without even so much as a 1 percent selloff. That's the longest streak of calm since 1995. It can’t last forever.

Anthony Mirhaydari is founder of the Edge (ETFs) and Edge Pro (Options) investment advisory newsletters. A two-week and four-week free trial offer has been extended to readers of The Fiscal Times. Redeem by clicking the links above.