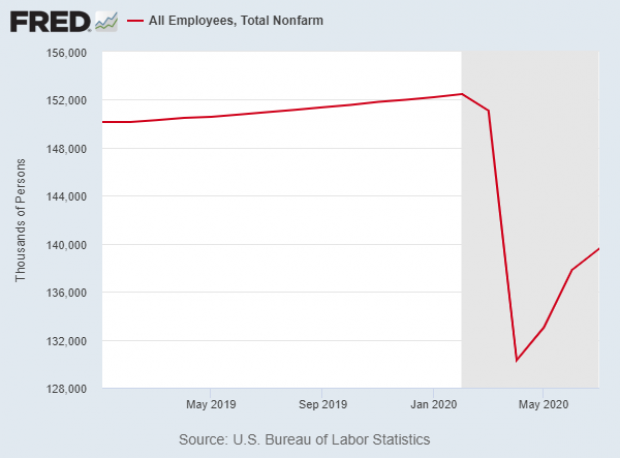

The U.S. economy added 1.8 million jobs in July, the Labor Department said Friday, and the unemployment rate dropped to 10.2%, down from 11.1% the month before. The jobs number beat consensus estimates of 1.5 million new jobs, and the unemployment rate fell nearly half a percentage point more than expected.

Showing job growth for the third straight month, the July report confirms that the recovery continues to rumble along. “Overall this is a favorable report and indicates that the economic recovery which began in May has continued at least through July,” economist Michael Feroli of J.P. Morgan said in a note to clients.

Still, while the July jobs number was positive, it was far smaller than the 2.7 million new jobs seen in May and 4.8 million recorded in June. The latest jobs report essentially provides a snapshot of conditions in mid-July, or about three weeks ago, and more recent data suggests that the surge of the coronavirus in some states, combined with the expiration of federal aid programs including the $600-per-week boost to unemployment benefits, have taken a toll on economic growth.

The beginning of a stall? Some economists are worried that the slowdown in hiring will persist and possibly turn negative, threatening a double-dip recession. Economist Ernie Tedeschi of Evercore ISI said that “after several months of extraordinary monetary & fiscal support, we've recovered ~40% of the jobs lost since Feb.” But we “still have a ways to go, and while July was a good report it was slower than May & June. And much of that fiscal support is already exhausted.”

Even so, there is a high degree of uncertainty among the experts. J.P. Morgan’s Feroli said that growth does appear to have slowed in recent weeks, but he does not expect to see a reversal, as some fear, writing that “it seems reasonable to expect continued positive job growth in August and beyond, albeit at a more moderate pace than seen over the past three months.”

A plea for fiscal support: Joseph Brusuelas, chief economist at the consulting firm RSM, said Friday that in his view, the U.S. is “clearly in the worst labor market since the Great Depression.” Separately, he told Politico that it is "absolutely critical to the economy" for Congress to make a deal for a new round of fiscal stimulus. “If the talks fail, the political sector is creating the conditions for at best a double dip recession or much longer downturn than would occur otherwise,” he said.

Mark Zandi of Moody’s Analytics struck the same note. “It is critical that lawmakers agree to another substantial fiscal rescue package before Congress goes away on its August recess for the fragile economy to avoid backsliding into recession,” he told Politico.

A long way to go: Whatever the prospects may be for growth over the next few months, the economy still has 12.9 million fewer jobs than it did in February (see the chart below). And if the pre-pandemic job growth trend is factored in — absent Covid-19, the economy was on course to continue adding jobs — the number of missing jobs comes to more than 13 million.

The key factor in recovering those jobs, some experts say, is gaining control over the coronavirus. “The economy is unlikely to go anywhere fast until the pandemic is over; that is, there is an effective vaccine that is widely distributed and adopted,” Zandi said.