Today Mish Shedlock featured a disturbing article with a title that succinctly summarizes an enormous financial problem: The "Education Bubble"; Student Loan Debt Passes Credit Card Debt, Expected to Hit $1 Trillion.

![]()

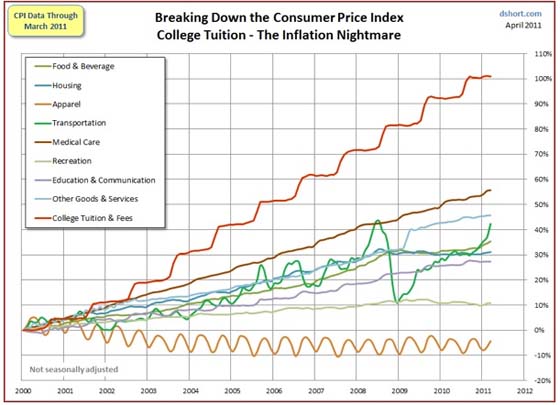

Mish's article especially resonates with my own research on the astonishing inflation in college tuition and fees, an imminent disaster that's been in the making for decades. This chart shows the relative growth of education costs as compared to the eight components of the consumer price index. College tuition and fees, a subcategory of Education & Communication, is weighted at a mere 1.5 percent of the overall CPI (more here). But for households that pay these expenses with student loans, the burden is staggering.

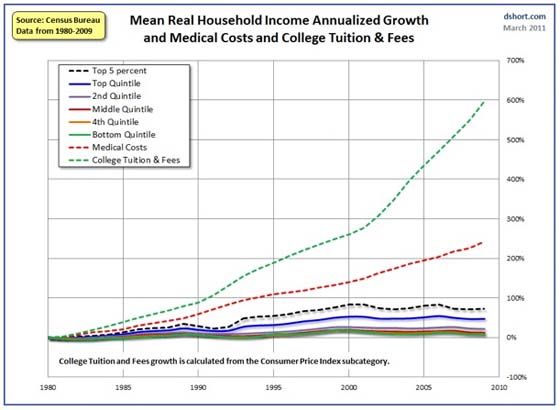

"How staggering?" you ask. The next chart shows a quintile breakdown, plus the top 5 percent, of mean real (inflation-adjusted) household income from 1980 to 2009 (the latest year of data from the Census Bureau). I've included an overlay of both medical costs and college tuition and fees in excess of the overall CPI.

Just to clarify: The nearly 600 percent growth in college tuition and fees through 2009 is above and beyond the 165 percent cumulative measure inflation based on the CPI. For more on this analysis, see my Household Income Growth Versus Two Major Expenses.

The Impact of Student Loan Debt on Retirement Planning

The burden of the skyrocketing student loan debt for young adults has inevitable consequences for the distribution of disposable income (personal income minus personal current taxes). More specifically, student loan debt shrinks discretionary income — the money left after paying off bills. Individuals who delay or make minimum contributions to retirement savings because of loan debt are losing the time value of money invested for a longer period.

We're entering an era when the growing cost of entitlements may well trigger policy changes that reduce Social Security benefits for younger wage earners. Such an outcome will increase the importance of building financial capital in 401(k)s, IRAs and other deferred savings plans, not to mention after-tax savings. Getting off to a late start in retirement planning because of major student loan debt is a recipe for a disastrous retirement.

Related Links:

And there Goes Spain (Business Insider)

Jeff Gundlach's Complete Guide To The Inevitable American Default (Business Insider)

John Paulson On The Worst Case Scenario For The The U.S. Economy (Business Insider)

S&P: There's Still A Huge Risk Of More Bailouts (Business Insider)

Richard Koo Explains Why The S&P's Downgrade Is Totally Absurd (Business Insider)