If you’ve tracked the disastrous rollout of the HealthCare.gov website at all, you’ve heard repeatedly about the vital importance of young enrollees for the ultimate success or failure of Obamacare.

Now a policy brief released Tuesday by the Kaiser Family Foundation suggests that those “young invincibles” are not quite as important as the conventional wisdom holds – and that, even if they enroll at relatively low levels, it’s highly unlikely that they will set off an Obamacare “death spiral.” The Kaiser analysis finds that, even in a likely worst-case scenario, premiums would only go up 1 to 2 percent in 2015, nowhere near the kind of spike that could send the reform law snowballing toward failure.

Related: Millennials Jump Ship over Obamacare Bait and Switch

The oft-repeated actuarial analysis behind that “death spiral” prediction goes like this: Obamacare imposes limits on how much more insurers can charge older policyholders relative to younger ones. That means the young enrollees will be subsidizing coverage for older ones. If young, healthy people don’t sign up in sizable enough numbers, insurers would be left with a pool of customers that is disproportionately older and sicker (read: more expensive).

The insurance companies would adjust by hiking premiums the next year, making their plans even less appealing to the healthier young group and increasing the likelihood that only those who most need coverage would sign up. As the cycle continued, it could destroy the individual insurance market and doom Obamacare.

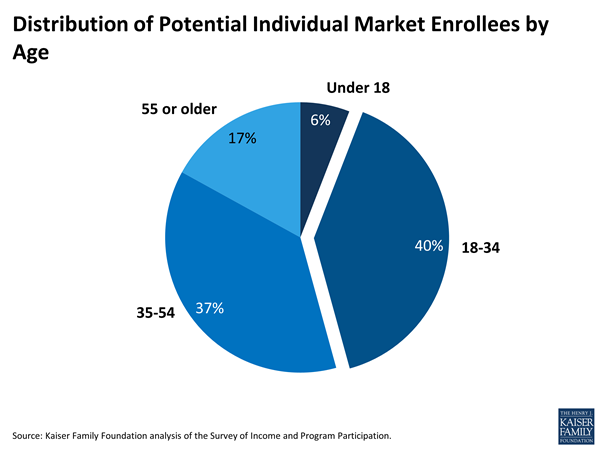

The reality isn’t quite that simple, Kaiser Family Foundation analysts Larry Levitt, Gary Claxton and Anthony Damico explain. Yes, they write, the age distribution across the entire market matters and the goal is to have young adults enroll in about the same proportion as they represent of the overall market of potential insurance buyers.

Adults age 18 to 34 make up 40 percent of the market, so, ideally, they’d account for 40 percent of new enrollments – that’s how the Obama administration got to its stated target of 2.7 million young enrollees, based on CBO projections that 7 million people would sign up for 2014.

The Kaiser analysis modeled out two scenarios in which young adults opt not to enroll to varying degrees. If adults under age 35 sign up for Obamacare at a 25 percent lower rate than the rest of the population, they would represent 33 percent of the individual market enrollees, not the 40 percent of the potential market they represent. The result, Kaiser reports, would be that insurers’ costs are about 1.1 percent higher than premium revenues.

In the second scenario, young adults sign up at half the rate of the rest of the population, so that they represent just 25 percent of enrollees. That rate roughly matches the enrollment rates through November for young adults in California’s health care exchange, which reported that 21 percent of enrollees over the first two months of open enrollment were in the 18 to 34 age range.

The Kaiser analysts note that “this is likely a worst-case scenario, since the expectation is that older and sicker individuals are more likely to buy first and that younger and healthier people will tend to wait until towards the end of the open enrollment period.” Even so, they found that costs in this case would only be about 2.4 percent higher than revenues from premiums.

Insurers typically set their rates to deliver a profit margin of 3 percent to 4 percent, the Kaiser trio wrote, meaning that even under this worst-case scenario, they’d still make a slim profit. Even if they raised rates by 1 percent to 2 percent in 2015 to boost their margins, that increase “would be well below the level that would trigger a ‘death spiral,’” the authors wrote.

The Obamacare law also includes some other components that could ward off a death spiral, including government subsidies that rise along with premiums and thus dampen any price hike to consumers and so-called “risk corridors” that would have the government compensate insurers if costs exceed projected targets by more than 3 percent.

The bottom line, according to the Kaiser report, is that signing up young adults may be less important than it has been portrayed to be, and the real key will be to get relatively healthy people to buy plans: “It is important to attract the ‘young invincibles,’ but maybe with a greater focus on the ‘invincible’ part.”

Top Reads from The Fiscal Times: