On November 16, the Harvard economist and former Treasury Secretary Lawrence Summers gave a provocative talk at an International Monetary Fund conference. In it, he suggested the possibility that the United States has entered into a long-term period of slow growth not dissimilar to that which Japan has suffered from for the last 20 years.

The specific term Summers used was “secular stagnation,” which is one familiar to an earlier generation of economists. Many believed that the Great Depression had permanently changed the long-term trend rate of economic growth that was possible given the rate of growth of the population, technological progress and the decline of investment opportunities, among other things.

Related: Japan’s Huge Stimulus Plan—A Bold Roll of the Dice

The principal spokesman for this view was the Harvard economist Alvin Hansen. He and other secular stagnationists feared that the prosperity of the war was just temporary and that the Great Depression would return as soon as the stimulus of wartime spending ended. Virtually all economists expected the unemployment rate to spike when millions of soldiers returned from the war and sought work.

As it turned out, pent up demand for goods that were unavailable during the war, the decimation of our economic competitors by the war and a permanently higher level of government spending for programs like Social Security and to fight the Cold War kept the economy growing. Indeed, the 25 years after World War II were almost a golden era in terms of growth, which greatly increased the middle class and improved living standards for the poor as well.

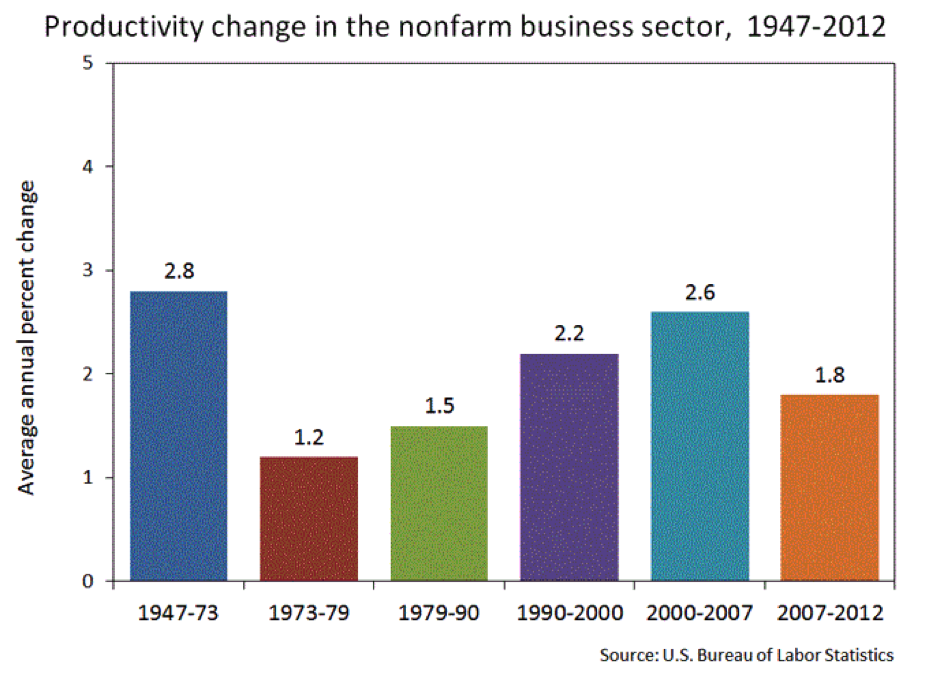

The golden era ended in the early 1970s for reasons that economists are still debating, but is unmistakable in the data. As one can see, the rate of productivity growth—output per man-hour—fell sharply after 1973. Lower productivity growth led to lower growth in wages and incomes.

There was a revival of productivity in the 1990s as computers and technology raised productivity growth almost back to its immediate postwar level. But since the financial crisis emerged in 2007, the growth rate has fallen and some economists expect it to fall further.

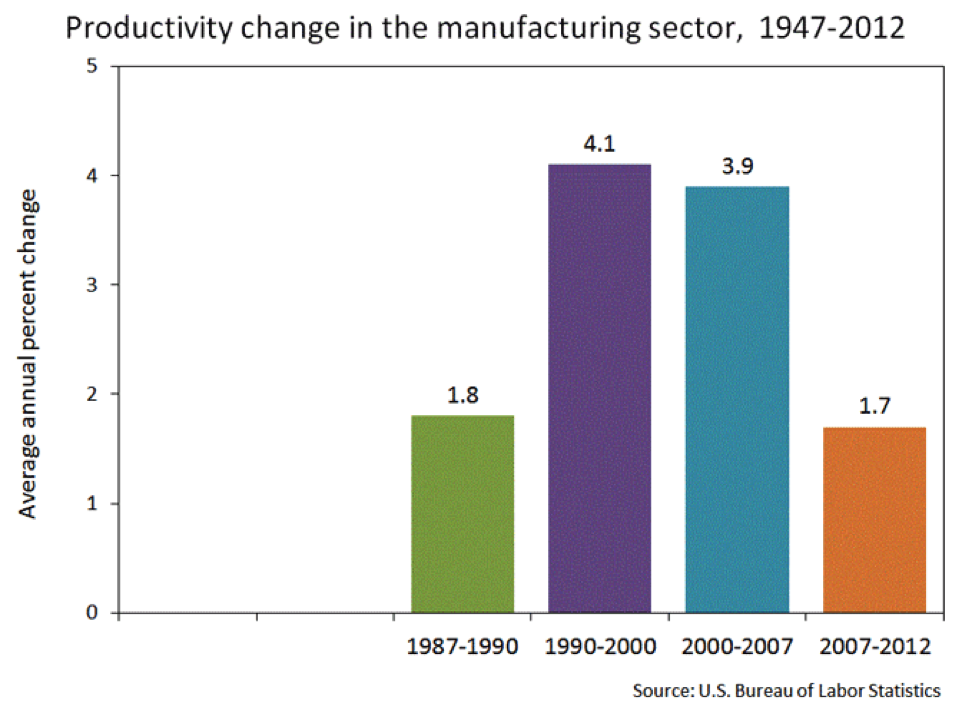

The economist Robert J. Gordon of Northwestern University is the principal spokesman for a pessimistic outlook for growth. He notes that almost all of the increase in productivity in recent years has been in manufacturing. But manufacturing is a declining share of the economy. Moreover, productivity growth has fallen in that sector as well.

As Gordon argues in a recent paper, whatever gains resulted from technology appeared to have been fully incorporated into productivity and the growth rate has returned to its pre-1990s trend of about 1.5 percent per year.

In another paper published last year, Gordon points to several “headwinds” against which real economic growth has to push to rise above the rates of less than 2 percent per year we have experienced since 2007. These include demographics, education, inequality, globalization, energy/environment and debt, both public and private.

Related: The Three-Speed Global Economy Puts U.S. in 2nd Gear

The key demographic factor is slowing population growth. It should be remembered that the formula for long-term growth in the gross domestic product is basically growth of the labor force plus productivity growth. If population is growing at a slower rate, that means the labor force will also grow at a slower rate 20 years or so down the road unless supplemented by immigration.

According to Social Security’s actuaries, the fertility rate in the U.S. has fallen from 3 in the 1950s and 1960s, to a rate of 2 since then. Even if productivity stayed the same, this factor alone would shave a percentage point off the trend rate of economic growth. Given the falloff in productivity, it appears that potential real GDP growth has fallen 2.5 percent per year over the previous generation.

Further evidence that growth is not likely to rebound quickly is that real interest rates remain very low. While this is partially a function of Federal Reserve policy, it also results from a dearth of investment opportunities, according to the economist Antonio Fatas.

In theory, the rate of interest and the rate of profit are linked. If a business can borrow at 2 percent and has an investment opportunity that will return 3 percent, it should make that investment. This is why the Federal Reserve expected investment to rise when it cut market interest rates. Yet even with such rates near zero, there is little evidence of rising investment. This can only be because businesses don’t perceive investment opportunities that would produce profit rates much above zero.

The worst-case scenario is Japan, which has had a real GDP growth rate of less than one percent for the last 15 years, with no sign of recovery. As recently as the 1980s, many Americans were fearful that the Japanese would overtake us and become the most powerful economic power on earth. Now those same people say the same thing about China.

Related: WTO Is Closing in on Landmark Trade Reform

The optimistic scenario is that technology is not stagnant. Innovation waxes and wanes, but new ideas have always come along and sometimes it takes a while for them to become significant drivers of growth. Also, new problems always come along and require new solutions.

The economic historian Joel Mokyr believes we have only scratched the surface of the potential for the Internet and computers to create new occupations and growth opportunities. And most economists think the recent economic slowdown temporary, resulting from problems in the financial sector that will eventually work themselves out. Better policies might have shortened that workout, but there is no reason yet to think they are permanent.

In all likelihood, recent slow growth is unlikely to continue indefinitely and become secular stagnation. On the other hand, there is at present no end in sight. Secular stagnation is a possibility that cannot be casually dismissed out of hand. Japan is proof of that.

Top Reads from The Fiscal Times: