There has been a lot about Bitcoins in the media lately. They are a type of electronic currency that is “mined” by computers and theoretically capped at a maximum of 21 million coins. Almost daily, some organization or business gets a bit of press by announcing that it is willing to accept Bitcoin payments.

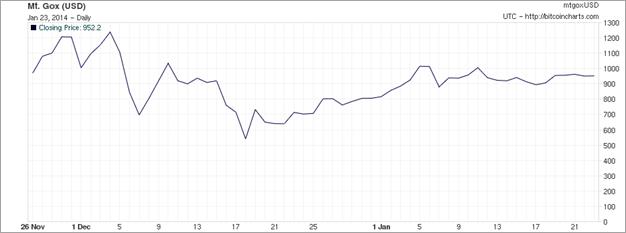

The price of Bitcoins varies and at times has fluctuated hundreds of dollars per coin in a single day. But lately the price has been relatively stable around $950.

NYU economist David Yermack says Bitcoins have none of the qualities of bona fide currencies. The Federal Reserve Bank of Chicago says that without illegal transactions, Bitcoins really have no purpose. However, Internet pioneer Marc Andreessen thinks the real value of Bitcoins is the underlying technology, which has wider application.

Related: Why Regulating Bitcoin Is Like Herding Cats

Libertarians in particular have been very excited by Bitcoins because they hate the Federal Reserve and love the idea of a free market money. It doesn’t seem to bother them that everything they say they hate about dollars is even truer with Bitcoins.

The main libertarian critique of the dollar is that it is a “fiat currency” that is not backed by anything real. Libertarians have long favored a gold standard with gold coins circulating as they did before 1933, and full convertibility of paper money for gold on demand at a fixed price.

But Bitcoins are literally backed by nothing. They are just computer code and don’t even have the physical presence of a paper dollar. At least there is gold in Fort Knox backing the dollar to some extent and it is legal tender for the payment of taxes and debts. No one can be forced to accept Bitcoins in payment for anything.

Some libertarians have made this point, including the economist Gary North. But most libertarians are still fascinated by Bitcoins. They are especially attracted by making anonymous payments for things that cannot be tracked by government through the traditional banking system.

Related: Porn, Drugs Hitmen, Hackers—Welcome to the Deep Web

This is indeed a potentially big draw for certain types of people, in particular criminals, terrorists and tax evaders. This means, inevitably, that Bitcoins are of great interest to government authorities and traditional banks subject to government regulations and scrutiny.

Yesterday, Treasury Secretary Jack Lew and JPMorgan CEO Jamie Dimon were asked about Bitcoins at the World Economic Forum in Davos, Switzerland. Lew said, “From the government’s perspective, we have to make sure [Bitcoin] does not become an avenue to funding illegal activities that have malign purposes like terrorist activities.”

Dimon said it was unlikely that his company would have anything to do with Bitcoins, suggesting that enforcement of laws against money laundering and terrorist financing would likely put an end to the phenomenon. (On Dec. 20, the Congressional Research Service issued a report on the legal obstacles to using Bitcoins as money.)

I think that’s right. The Treasury and Federal Reserve could put Bitcoin out of business in a minute if they choose to do so. I think they are looking the other way for now because they don’t really believe that Bitcoins are a currency or anything remotely like one. They are simply an asset, a commodity that some people are willing to pay real money for.

Related: Feds Are Targeting Unregistered Bitcoin Exchanges

If this is the case, then there is no reason why users shouldn’t pay taxes on gains in the value of Bitcoins just as they do when they invest in gold or Treasury securities or any other asset that has some characteristics of money. This is the position that Singapore has taken and it appears that the United Kingdom will as well. Sweden and Finland have also said that Bitcoin is not a currency, merely a commodity that should be taxed as such.

The Internal Revenue Service has yet to take a position on the matter. In her recently-released annual report for 2013, Taxpayer Advocate Nina Olson said that existing IRS guidance on the taxation of Bitcoins is inadequate and urged the agency issue rules that specifically apply to it and other electronic or cyber currencies, which are proliferating.

Of course, if taxes have to be paid on gains in the value of Bitcoins, this will severely limit their use as a currency. It also points out the fact that any currency whose value fluctuates as Bitcoins do is very poor at providing the function of a medium of exchange. Stability is an essential quality of money.

While it is true that the value of the dollar fluctuates, it does so gradually and relatively predictably. Even when inflation in the U.S. was over 10 percent in the late 1970s, there was no movement to replace the dollar with some other type of currency. That really only happens when hyperinflation occurs, which is defined as a rate of inflation exceeding 50 percent per month. I repeat, 50 percent per month. Remember that the next time someone casually throws around the word “hyperinflation.”

Related: The Bitcoin Gamble—Is Now the Time to Invest?

I think Bitcoins are a momentary fad that will fade away. But they raise important questions that aren’t going away. One is how businesses will respond to changes in the way people want to pay for things such as with smart phones. Many ways of making payments more convenient for consumers are hampered by outdated laws and regulations, designed for an era when people paid with cash or checks that have barely caught up with the use of credit and debit cards. Obviously, it is in the interest of both buyers and sellers to make paying for things as easy as possible, but those institutions that benefit from the status quo, such as banks and credit card companies, will resist.

The other question of continuing importance is the idea of true electronic currencies; that is, replacing all coins and paper currencies with electronic money. The University of Michigan economist Miles Kimball is the principal exponent of this idea. He points out that it would have vast benefits for the Federal Reserve in the conduct of monetary policy. Instead of buying and selling Treasury securities and waiting for the effects to trickle down through the economy, the Fed could instantaneously and everywhere increase liquidity to fight an economic downturn or squeeze liquidity to fight inflation.

Space prohibits a full discussion of the theoretical issues raised by a pure electronic currency system and it certainly won’t happen any time soon. Many people will strenuously resist giving up the convenience and anonymity of cash transactions. However, they shouldn’t underestimate government’s ability to end the use of currency if it wishes to. Just this week, India announced that it was calling in all pre-2005 currency in an effort to fight the underground economy. In 1933, the U.S. called in all gold coins and later retired all bills larger than a $100.

Top Reads from Bruce Bartlett:

- Slashing the IRS Budget: Penny Wise, Pound Foolish

- Enterprise Zones: A Bipartisan Failure

- Why Legalizing Marijuana is a Smart Fiscal Move