For weeks, I've been warning that U.S. large-cap stocks, which continue to trade at levels hit more than year ago, were imparting a false sense of confidence in regular investors. Just beneath the surface, things were much uglier.

That truth is being revealed this week as fresh weakness in crude oil — prices have fallen to seven-year lows — is pushing the Dow Jones Industrial Average back below its 200-day moving average after a push toward the 18,000 level once again met intractable resistance. The Energy Select SPDR (XLE) touched lows not seen since late September, down roughly 13 percent from its early November high.

As a result, stocks are looking vulnerable to a quick drop back to the August-October lows at a time when holiday cheer and end-of-year excitement have traditionally pushed the market higher.

Related: Here's Why Oil Prices Are at 7-Year Lows

Consider that the Russell 2000 small-cap index has moved below its 50-day moving average to trade down about 11 percent from its June high. Or how transportation stocks, which are supposed to be on the front lines of the economic cycle connecting manufacturers to suppliers and retailers, have fallen below their late September levels and are down nearly 18 percent from their late 2014 highs.

Or consider how the iShares High-Yield Corporate Bond Fund (HYG) has dropped below its October low to return to 2009 levels, down more than 8 percent from its June high — or nearly two years' worth of dividend payments.

Or how commodity prices have been absolutely pummeled, with the CB Commodities Tracking Index Fund (DBC) down nearly 24 percent below its 2009 financial panic low.

Large-cap stocks are now succumbing to the same fearful selling that has hit these other areas. The catalyst: The wipeout in crude oil and the impact it will have on energy sector earnings.

There has also been chatter of the pressure building on the high-yield bonds of many vulnerable U.S. shale oil producers and the likelihood of an increase in debt defaults. Bloomberg reported that the average yield on speculative-grade oil and gas bonds has climbed to 13.4 percent, the highest level since the financial crisis.

Related: Why Raising Interest Rates Isn’t as Easy as It Sounds

Investors are reacting to the decision by OPEC oil ministers on Friday to continue their price war against U.S. shale producers by keeping production near their 30 million-barrel-per-day quota, in place since 2011. Officials from Indonesia warned that an emergency OPEC meeting would need to be held if oil prices fell below the $30-a-barrel level. Until then, a change in strategy is unlikely. So the downward spiral — weak energy, weak earnings, higher bond yields, lower stock prices — is set to continue.

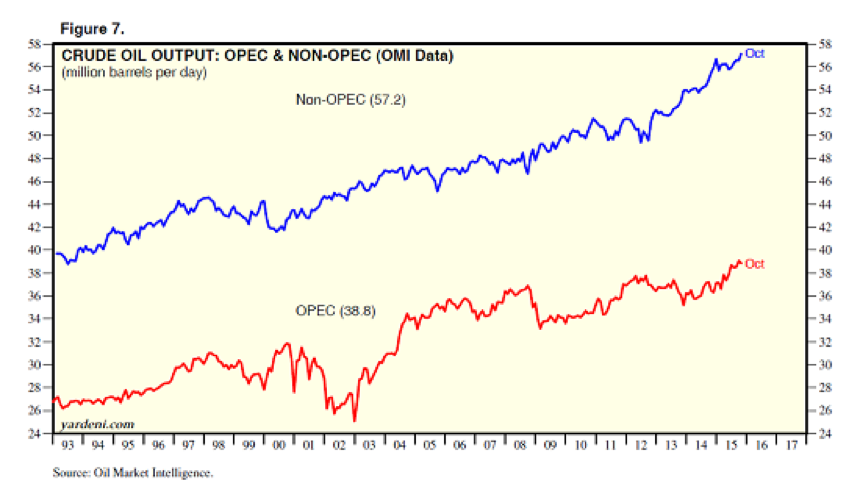

Moreover, while OPEC's official ceiling is around 30 million bpd, Oil Market Intelligence (OMI) reports that they actually produced at a near-record pace of 38.8 million bpd in October while non-OPEC producers pumped a record 57.2 million bpd. Poorer OPEC countries are being forced to pump more oil, despite lower prices, to try to help minimize the overall hit to revenues.

Similarly, weaker U.S. shale producers are being forced to pump more oil at lower prices to try to raise the liquidity they need to service their debt load.

While U.S. drilling rig counts have fallen, U.S. shale producers have refocused on low cost/high productivity wells to keep production relatively stable. Offshore production, on the other hand, is actually rising, according to the U.S. Energy Information Administration, since oil companies want to complete these complex and costly wells once they've begun.

With manufacturing activity slowing globally and here at home, the world is simply awash in too much oil. It's simple supply and demand. And until OPEC cuts production, or a wave of defaults and bankruptcies hit the U.S. oil patch, it's only going to get worse.

With prices so low, global oil revenue is collapsing, down 56 percent from last year's peak, according to Yardeni Research: from a $3.8 trillion annual rate to $1.7 trillion. That will continue to weigh on the earnings of energy companies like Chevron (CVX), which reported a 37 percent year-over-year drop in revenues back in October.

Related: 5 States Getting Crushed by Low Oil Prices

Already, according to FactSet, fourth quarter S&P 500 earnings are expected to decline 4.3 percent over last year, in what is set to be the third consecutive quarter of declining profits. This is something that hasn't happened since 2009. Energy sector profits are expected to decline 65 percent over last year.

Back in September, the overall expected Q4 earnings drop was just 0.6 percent.

How far could stocks fall? If the Dow Transportation Average (blue line above) is any guide, the Dow Jones Industrial Average (black line) could soon suffer a drop back below the 16,000 level — a decline of almost 9 percent from here.