Controversy erupted last week when University of Massachusetts Professor Gerald Friedman produced estimates showing that under the Sander’s economic plan, “The growth rate of the real gross domestic product will rise from 2.1 percent per annum to 5.3 percent so that real GDP per capita will be over $20,000 higher in 2026 than is projected under the current policy.” The reaction from critics is exemplified by a letter from four former heads of the Council of Economic Advisors under Democratic presidents, Alan Krueger, Austan Goolsbee, Christina Romer, and Laura D’Andrea Tyson:

“As much as we wish it were so, no credible economic research supports economic impacts of these magnitudes. Making such promises runs against our party’s best traditions of evidence-based policy making and undermines our reputation as the party of responsible arithmetic.”

Related: The Pros and Cons of Bernie Sanders’ $50 Billion Tax Idea

Defenders such as Jamie Galbraith, an economist at the University of Texas, argued that there is nothing “magical” or outlandish about the estimates, Professor Friedman used a defensible model to obtain his results:

“What the Friedman paper shows, is that under conventional assumptions, the projected impact of Senator Sanders' proposals stems from their scale and ambition.

When you dare to do big things, big results should be expected. The Sanders program is big, and when you run it through a standard model, you get a big result.”

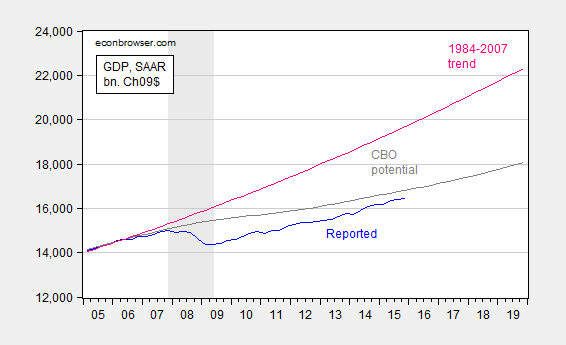

Is it possible for the economy to reach such a high rate of economic growth? To answer that question, this graph from University of Wisconsin Professor Menzie Chinn is helpful:

The graph shows the actual path of real GDP, the expected trend for potential real GDP based upon pre-recession data, and updated estimates of the trend from the CBO in light of the Great Recession.

Related: Bernie Sanders’ $18 Trillion Price Tag If Elected President

Why is there such a big difference between the pre- and post-recession estimates of the trend for real GDP? First, the housing bubble inflated the pre-recession data and distorted estimates of the trend in GDP upward, something that was not recognized until after the housing bubble collapsed.

Second, the rate of population growth has been declining and the population has been aging in a way that was not fully revealed in the pre-recession data, both of which reduce the size of the workforce and our ability to produce goods and services.

Third, during the recession, many people, discouraged by their job prospects, dropped out of the labor force and many will never return. Finally, productivity fell during the recession reducing our productive capacity. As former president of the Minneapolis Fed, Narayana Kocherlakota notes, empirical estimates suggest that a 1 percent increase in unemployment is associated with a .9 percent fall if productivity, which is a fairly sizeable amount.

Our ability to grow over the next few years depends upon the size of the gap between actual output and potential (trend) output. The bigger the gap, the more room there is for short-run growth. From the graph, it appears as though the gap between actual and potential output is relatively small, and hence our ability to grow over the next few years is limited. How can we possibly sustain a 5 percent growth rate over the next several years with such a limited gap to close?

Related: Sanders' Big Spending Plans Would Reinvent the U.S.

However, there is a lot of uncertainty in the estimates of potential output. We don’t know for sure how many of the people who left the labor force during the recession will return when the economy begins to boom, job opportunities are plentiful, and wages finally begin to rise. We are uncertain about how much of the pre-recession estimates of the trend rate in output was due to the housing bubble rather than true underlying economic fundamentals.

We are also uncertain about how much of the fall in productivity during the recession was due to long-run structural factors rather than the economic downturn. We can calculate the fall in population and the aging of the population fairly precisely, but when it comes to translating those estimates into the effects on the workforce, we cannot know for sure, to take one example, how many people will retire at age 62 rather than keep working until they are 65 or older.

Because of this uncertainty, we should not take it as given that our ability to grow over the next few years is as limited as the graph above might imply. An aggressive policy such as Senator Sanders has in mind could, in the end, result in inflation as we butt up against and try to push past the constraint implied by the estimates of potential output. But there is considerable uncertainty about this and there may be more room than we think. As I see it, accepting that our capacity to grow is limited when in fact there is considerable room for growth is a much bigger error than attempting to grow and finding that the gap is small.

Related: Bernie Sanders: ‘We Will Raise Taxes. Yes, We Will’

In the first case, people who could be working remain unemployed, while in the second there would be inflation. Inflation is relatively easy for monetary authorities to reverse, and the costs fall mainly on the wealthy. Unemployment is much harder to overcome, and the costs fall mainly on the working class. Thus, if we are going to make a mistake, it ought to be shooting for more employment than we need rather than too little.

In addition, the long-run trend rate of economic growth depends upon economic policy. If we implement policies that promote both public sector and private sector investment, it’s possible to lift our long-run potential above where it is today. Actual output would then be chasing a moving target as we try to close the output gap, and we might be surprised at how much our productive capacity, and hence our ability to provide jobs, can be increased.

Narayana Kocherlakota argues “that there are good reasons to believe that, with appropriate stimulus, it would be possible to achieve growth outcomes of around 5-6 percent per year for the next four years.” But we won’t know unless we try. The inflation risk is minimal, and we owe the households who have struggled so much during the recession and the long, drawn out recovery the best possible chance we can give them of finding a decent job.