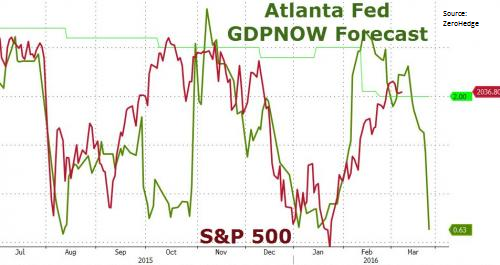

While the stock market is back near three-year highs and job growth remains strong, U.S. economic growth has hit the skids once more. On Monday, in response to tepid personal spending data, the Federal Reserve Bank of Atlanta marked down its first quarter GDP growth estimate to just 0.6 percent — down from 1.4 percent just last week.

The downward economic trend is clear. The Q1 "GDPNow" estimate from the Atlanta Fed is down from the 2.0 percent result posed in the third quarter of 2015, the 2.2 percent average growth rate seen in the first three quarters of 2015, and the 2.4 percent advance seen in 2014.

The Brutal Economic Truth Behind the Rise of Trump

The problem, it seems, is that strength in consumer spending (primarily on services) is fading despite relatively stable income growth. Shoppers simply remain cautious at a time when they are needed to aggressively offset the slowdowns in corporate profitability and factory activity. Those slowdowns are driven by falling labor productivity and rising labor costs as well as low energy and commodity prices and currency volatility.

More recently, based on survey responses to the March manufacturing PMI report (which missed expectations by the most since 2013), there has been concern about the increasingly contentious U.S. presidential campaign.

Monday's spending data included a downward revision to January's numbers that dropped a 0.5 percent month-over-month surge to a paltry 0.1 percent expansion, the weakest result in over a year. The savings rate, meanwhile, climbed to the highest since 2012.

Capital Economics now estimates first-quarter real consumption growth is likely to clock in at around a 2.0 percent annualized rate, down from the 2.4 percent rate seen in the fourth quarter of 2015 and a "disappointment given that employment continued to grow at a solid pace in the first quarter and households enjoyed a further boost in purchasing power from even lower energy prices."

The trouble is that U.S. economic growth has been near its historical "stall speed" of around 2.0 percent since the second half of 2010 — a subdued level of growth that has tended to tip the economy into recession. Each of the last 11 recessions was preceded by a drop in real GDP growth to 2.0 percent.

The continuation of the Federal Reserve's ultra-cheap monetary policy has kept things going. But even that's under threat now as the Fed continues to hint at further rate hikes, albeit gradual ones, in response to a low unemployment rate and evidence that inflation is firming.

Related: Here’s Why Interest Rates Could Be Locked in Until 2018

At this point, things don't look good for the corporate sector. Wells Fargo analysts warn that if "profits remain depressed, the prospects for [capital expenditures] and hiring will come under greater pressure." Business spending on equipment declined at a 2.1 percent annualized pace last quarter, for context.

In light if all that, a turnaround in economic growth depends on consumers opening their wallets. Up to this point, spending has been driven by increases in health-care outlays. Moving ahead, we'll need to see this broaden to areas such as housing. In the fourth quarter of last year, residential fixed investment grew 10.1 percent, up from 8.2 percent in the prior quarter.

Related: Here’s a Sign the Housing Market Is Returning to Normal

All of this is a problem for stocks since, as shown in the chart above, the S&P 500 has been tracking the ups and downs of the economy with a slight delay. With stocks currently contending with overhead resistance going back to late 2014, the drag from slower economic growth could result in a retest of the January-February lows in the months to come.

Much also depends on the "will they or won't they?" decision on rate hikes from the Federal Reserve.

After the "dovish hold" announcement by the Fed earlier this month — which cut in half the number of expected rate hikes this year to just two — the chatter has turned the other direction. A number of policymakers are talking up the odds of an April rate hike when Wall Street didn't expect action until June at the earliest.

St. Louis Fed President James Bullard, who is one of the more prolific Fed chatterboxes, was in the news again on Sunday night telling Nikkei reporters that April and June are "live meetings" for the Fed to raise rates again while downplaying the odds of negative interest rates here in the United States — something that's been deployed, with mixed success, in Japan and the Eurozone.

Janet Yellen’s speech to the Economic Club of New York on Tuesday broke this hawkish trend, but if GDP growth doesn't turn around soon, Yellen’s dovishness might not be enough. And Bullard might have to eat his words as a new recession would likely see interest rates in the United States push below the zero bound.