As any parent knows, dependents are tax deductible. However, letting your children file on their own can create significant tax saving opportunities if you are subject to rules that limit many traditional tax breaks.

Most questions about taxes begin with “can I?” However, the more fundamental question is “should I?” The distinction is important. “Can I?” implies that the item in question is a good idea in the first place. Often, it is not.

Case in point: Because you can claim your college kids as dependent doesn’t mean you should. In a situation where you earn too much to claim your children’s education credits or the dependency exemption, it is worth evaluating the option to remove them from mom and dad’s tax return.

If your family has a modified adjusted gross income above $180,000, you do not qualify for any education-expense credits or deductions, such as the tuition and fees deduction (up to $4,000), the American opportunity tax credit ($2,500) and the lifetime learning credit ($2,000).

Related: The Compelling Case for Lower Capital Gains Tax Rates

Also, families who fall into the trap of alternative minimum tax (AMT), a separate tax system that denies many traditional tax breaks, obtain no benefit from claiming dependents.

The AMT is more likely to hit financially successful families – those with annual earnings between $200,000 and $500,000, families with several children and those in high income tax states, such as New York and California.

When you don’t benefit from these credits and exemptions, having your college-age children file their own tax returns is advantageous. They can claim the education credits if they have an income and are paying some education expenses. If the students provide more than 50% of financial support (food, shelter, clothing or education), they can claim themselves as a personal exemption.

There is also the under-utilized possibility of creating income for a college student when zero or limited earned income exists.

Consider a college student has annual support needs of $50,000 to cover tuition, living expenses, etc. The parents jointly gift $28,000 of appreciated securities. The student then sells the assets to cover some expenses, while mom and dad supplement the remaining $22,000.

The amount of the gift falls within the annual gift tax exclusion (aka, the ceiling on tax-free giving, $14,000 per parent in 2015, or $28,000 for both), so no one owes a cent to the Internal Revenue Service. And the student now meets the requirement to cover at least 50% of financial support, which means he or she can claim the dependency exemption.

Related: The IRS Tax Scam That Can Rob You Blind

It gets better.

If your children claim themselves, they can sell the investments without triggering the so-called “kiddie tax.” Those who are under 24 and do not provide more than 50% of financial support are subject to the parent’s tax rate when they have investment income of more than $2,100 in 2015. However, the student’s ability to claim the personal exemption eliminates any kiddie tax.

We use two examples to demonstrate the possible tax savings from this strategy for different levels of parental income.

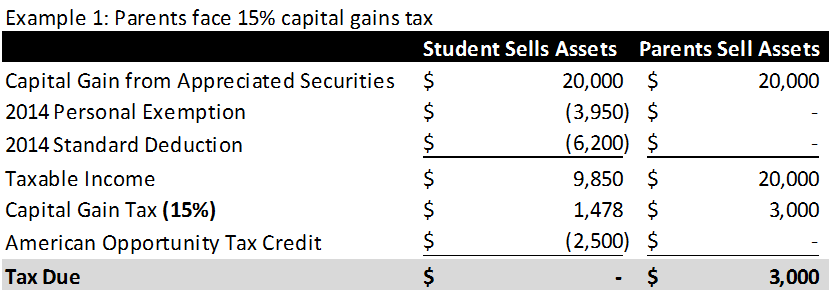

The first example depicts a family with enough income to disqualify them from education credits and additional dependency exemptions. In this case, the total one-year tax savings is $3,000 as the student makes use of the credits, deductions and exemptions which are not available to the parents.

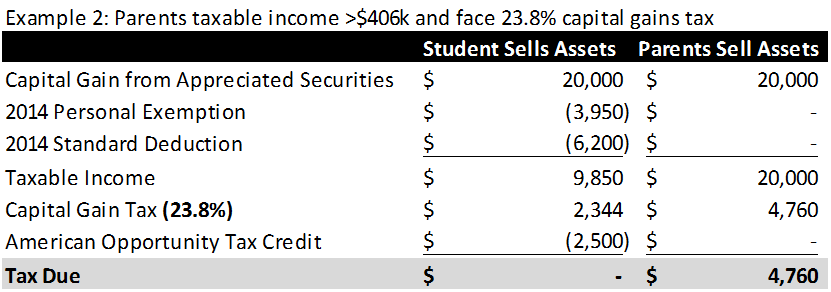

The second example is a family with higher taxable income, which subjects them to a 23.8% capital gain tax rate. In this case, the tax savings is $4,760 in just one year for one child. Over the course of college and graduate school, high income families with multiple children can save $60,000 to $100,000 in taxes simply by smart tax planning.

Despite the complexity of the tax code, finding significant opportunities is possible by going beyond simple tax preparation and thinking outside the box.

Follow AdviceIQ on Twitter at @adviceiq.

Top Reads from The Fiscal Times