Garage or Backyard? Here’s What First-Time House Buyers Want

More than two-thirds of potential first-time homebuyers want a house in move-in condition, and 43 percent are looking for a place in the burbs.

Beyond that, first-time buyers are most interested in a home with a backyard or pool, striking design, and smart or energy efficient technology, according to the TD Bank First-Time Home Buyer Pulse.

“It’s encouraging to see interest from the first-time homebuyers who have been cautious for much of the housing recovery,” TD Bank Head of Pricing and Secondary Markets Scott Haymore said in a statement. “Consumers are gaining confidence in the economy and many are looking to enter the housing market within the next two years.”

Related: Why First-Time Home Buyers Are Flocking to Tennessee

Last year, first-time homebuyers comprised 38 percent of the market, according to the National Association of Realtors.

Among those surveyed, 62 percent want to make a down payment of at least 20 percent, but nearly two-thirds said they were still saving up for it. Almost half said they needed to pay down debt before they could buy a house.

The average down payment in the first quarter of 2015 was $57,710, reports RealtyTrac. Entry-level buyers usually put down less money than repeat buyers, and are more likely to take advantage of Federal Housing Administration loans, which allow down payments of as little as 3 percent for those who qualify.

Those who can’t get an FHA loan can still put down less than 20 percent by buying private mortgage insurance, with annual premiums of between 0.5 percent and 1 percent of the loan amount.

Quote of the Day: A Big Hurdle for the Tax Cuts

“He goes in and campaigns on an issue, and the challenge is he then talks about executing drug dealers. Why do you think the press is going to cover the tax cuts if you’ve given them the much more exciting issue?”

-- Grover Norquist, president of tax-cutting advocacy group Americans for Tax Reform, on President Trump’s failure to sell the tax law.

The Obamacare Mandate That Could Produce $12 Billion in Fines in 2018

Republicans effectively eliminated the individual Obamacare mandate in the tax package signed late last year. Although the new regulation reducing the mandate penalty to zero doesn’t take effect until 2019, President Trump has cited the rule change as a victory over the health law so many conservatives oppose. “Essentially, we are getting rid of Obamacare. Some people would say, essentially, we have gotten rid of it," Trump told a crowd in Michigan two weeks ago.

However, many parts of the Affordable Care Act are still in effect and will continue to operate even after the individual mandate is eliminated in 2019.

In particular, the employer mandate, which requires companies with more than 50 employees to offer health benefits or face fine of roughly $2,000 per worker, will continue to play a significant role in the Obamacare system. The Congressional Budget Office estimates that the mandate will produce more than $12 billion in fines in 2018 alone.

Some conservative groups are pushing lawmakers to stop enforcing the employer mandate, but the IRS is still working to enforce the law. According to The New York Times Monday, the IRS is sending out notices to more than 30,000 businesses that have failed to comply.

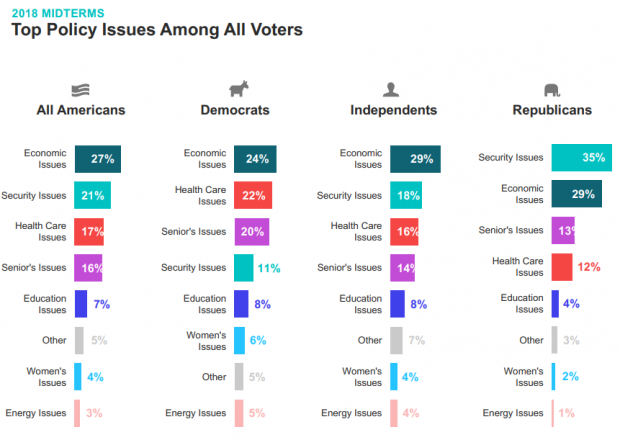

Chart of the Day: It’s Still the Economy, Stupid

Security may be the top policy issue for Republican voters, but the economy is the top concern for Democrats, independents and voters overall, according to Morning Consult’s latest polling on the midterm elections. Health care is third on the list, followed by “seniors’ issues.” The results are based on surveys with more than 275,000 registered U.S. voters from February 1 to April 30.

Number of the Day: $13 Billion

An analysis by Bloomberg finds that the roughly 180 companies in the S&P 500 that have reported earnings for the first three months of the year saved almost $13 billion thanks to the corporate tax cut enacted late last year. Those companies’ effective tax rate dropped by more than 6 percentage points on average. About a third of the tax savings went to 44 financial firms.

How a Florida Doctor with Social Ties to Trump Delayed a $16B Billion VA Project

A West Palm Beach doctor who is friends with Ike Perlmutter, the chairman of Marvel Entertainment and an informal adviser to President Trump on veterans’ issues, has held up “the biggest health information technology project in history — the transformation of the VA’s digital records system,” Politico’s Arthur Allen reports. Dr. Bruce Moskowitz “objected to the $16 billion Department of Veterans Affairs project because he doesn’t like the Cerner Corp. software he uses at two Florida hospitals, according to four former and current senior VA officials. Cerner technology is a cornerstone of the VA project. … Moskowitz’s concerns effectively delayed the agreement for months, the sources said.” Read the full story.