The federal budget deficit this year will increase in relation to the overall economy for the first time since 2009 and will continue on an upward trajectory for the coming decade, according to a new report by the non-partisan Congressional Budget Office.

With government spending now outpacing revenues for the remainder of the year through Sept. 30, the fiscal 2016 deficit will total $590 billion, or about $152 billion more than the previous year’s shortfall.

Related: Big Deficits Loom as Candidates Pile on Spending and Tax Cuts

Absent any major change in government policy – such as congressional approval of higher taxes or major reforms to Social Security, Medicare and other major entitlements – the deficit is projected to grow considerably in the coming decade as a share of the overall economy. At the same time, the publicly held debt – the amount the Treasury borrows from other countries and investors to keep the government operating -- would rise from an already highly elevated level.

“In CBO’s baseline projections, the budget deficit is generally on an upward trend over the next decade, reaching 4.6 percent of GDP in 2026,” the report states. “A slight decline in the deficit over the next two years is largely explained by the shift in the timing of payments from one fiscal year to another because certain scheduled payments fall on weekends.”

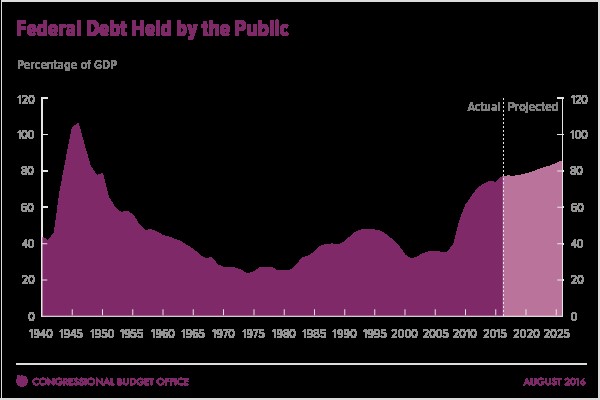

In later years, however, continued growth in spending—particularly for Social Security, Medicare, and net interest—would outstrip growth in revenues, “resulting in larger deficits and increasing debt,” the report warns. As those deficits accumulate, publicly held debt will rise from 77 percent of Gross Domestic Product or $14 trillion by the end of this year to 86 percent of GDP or $23 trillion by 2026.

“At that level, debt held by the public, measured as a percentage of GDP, would be more than twice the average over the past five decades,” the report states.

The new CBO report is the latest alarm bell set off by budget watchdog and fiscal conservatives who warn that – despite the major declines in the deficit achieved by the Obama administration during the economic recovery, a “structural mismatch” between revenues and spending will only get worse as time goes by.

In the current fiscal year, for example, projected total revenues of $3.27 trillion will be eclipsed by $3.87 trillion of spending. By fiscal 2016, the mismatch will be $4.99 trillion of revenue to $6.23 trillion of spending outlays, unless Congress and the next president alter spending and tax policies.

President Obama inherited a financial crisis and major recession upon entering office in January 2009 and presided over massive budget deficits as high as $1.4 trillion beginning in fiscal 2009. After four consecutive years of deficits of $1 trillion or more, the red ink began to taper between fiscal 2013 and 2015, bottoming out at $396.5 billion in fiscal 2015.

Related: Trump’s Massive Tax Cuts and New Spending Alarm Fiscal Conservatives

But now the deficit is on the rise again, a development that will provide added grist for the debate in Washington over whether this is the time for more belt-tightening or whether low-interest rates and the growing need for new infrastructure and economic growth demand increased spending and borrowing.

Republican presidential nominee Donald Trump and Democratic nominee Hillary Clinton have both called for major new spending to rebuild the nation’s highways, bridges, airports and other infrastructure to generate new jobs and bolster the economy. Clinton has proposed raising taxes to help finance these and other initiatives, while Trump says he will slash taxes on corporations and individuals by between $10.1 trillion and $11.9 trillion over the coming decade.

Alarmed fiscal conservatives say that neither approach would address the economic and budgetary problems associated with the mounting debt and an annual deficit that has begun growing again after years of decline.

“Now it’s official: the era of declining deficits is over,” said Maya MacGuineas, president of the Committee for a Responsible Federal Budget and head of the Campaign to Fix the Debt. “CBO has just projected that this year’s deficit will be 35 percent higher than last year’s -- $590 billion vs. $438 billion – and that trillion-dollar deficits will be back by 2024.”

New CBO Director Renews Warning on Long-Term Debt

MacGuineas said in a statement that instead of “prematurely declaring victory” over the lower deficits in recent years, “lawmakers should have used that period to phase in tax and spending reforms to address our nation’s long-term fiscal challenges.

“With the national debt at post-war record high levels and projected to grow another $9 trillion over the next decade, it’s time our leaders get their acts together,” she added.

The new CBO report warned that rising debt would have “serious negative consequences for the budget and the nation.” Those include mounting interest payments on the debt, reduced savings within the economy, less flexibility to use tax and spending policies to respond to unexpected crises or challenges, and “the likelihood of a fiscal crisis in the United States would increase.”

“There would be a greater risk that investors would become unwilling to finance the government’s borrowing needs unless they were compensated with very high-interest rates,” the report states. “If that happened, interest rates on federal debt would rise suddenly and sharply.