While Obama administration officials apologized for HealthCare.gov foul-ups and sought to spin the president’s flawed promise that if people liked their health plans they could keep them, I actually made some headway in getting into the federal insurance marketplace.

Although I didn't get in through my online log-in — that interface was still broken as I write this — I did manage to "talk" my application to a telephone (800-318-2596) representative and get some sample policy premiums. Some 700,000 applications for insurance were submitted to the state and federal online marketplaces since the beginning of October, Marilyn Tavenner, the administrator for the Centers for Medicare and Medicaid Services told a Congressional committee last week. I was one of them.

I managed to submit my application to a patient customer service representative ("Sasha"), who walked me through questions on income, family members, Social Security numbers, disclosures and birthdates. There were also some questions about physical limitations and foster care, which, fortunately, were not issues for us. The whole process took about a half hour.

The moment of truth with HealthCare.gov comes when you finally get to see a range of premiums to determine if the program will be competitive with private insurance. As I've noted in previous posts, I have a catastrophic health plan that currently costs $7,128 a year ($594 monthly) for premiums, but doesn’t cover doctor's visits, immunizations or prescription drugs. All of the plans on HealthCare.gov cover these basic services. My out of pocket limit is $6,350 on the individual private plan; it's the same for the HealthCare.gov policies ($12,700 for a family policy).

Since drugs, immunizations and doctor visits are covered in the federal exchange — the bulk of our ongoing medical expenses for my family of four — we're immediately ahead of the game. That's roughly a $1,200 annual savings for us. Maternity and hospitalization are also part of the basic benefits that will be covered by the exchange-offered plans, although it seems like maternity should be optional. We won't need the benefit; those who opt out should get a premium break.

I'm also hoping that the exchange plans will have minor annual increases; my private premium has risen 10 percent to 20 percent each year over the past five years.

PRICING DIFFERENT LEVELS OF CARE

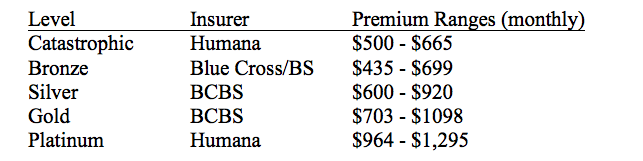

In order to gauge total savings, though, we have to examine the offerings within the five exchange plan levels. Depending on how much you want to cover in terms of out-of-pocket expenses, you can choose a plan that suits your budget. There are five levels of coverage: Catastrophic, Bronze, Silver, Gold and Platinum.

The first two tiers are bare bones, covering up to 60 percent of total health expenses. Silver, Gold and Platinum cover 70 percent, 80 percent and 90 percent, respectively.

Then you need to see specific offerings within your state program. More populous states have several insurers and co-ops competing while smaller states may only have a few policies listed.

In Illinois, there were a wide variety of plans within each level. Here's a sampling:

These premium amounts, however, are not necessarily the final amount those buying insurance on the exchanges will pay. As the Kaiser Family Foundation estimated in a report released Tuesday, some 17 million people will be eligible for tax credits that will reduce (or, for some 7 million people, potentially eliminate) the cost of their insurance. My family doesn't qualify for the subsidies because of our income, so the premium ranges I'm seeing are likely good estimates.

What I don't know is why there's such disparity between insurers within a given plan level. Most of the prices I quoted were for Preferred Provider Organizations (PPO), although you can also get quotes from Health Maintenance Organizations (HMO), where the choice of providers is limited to the insurers' networks and the mode of care is constrained. The premium quotes I saw were estimates, so there's more to this story.

By the way, if you can't submit an application online or don't want to deal with the phone reps, Sasha told me of a back door to see sample policy rates: Go to the search box on HealthCare.gov and enter "plan estimates without applications," then enter your state. Some policies will pop up, so you can get some idea of what to expect.

At first blush, the $435 Bronze monthly premium looks appealing, although I will need more information on whether my doctor and providers are within the insurer's PPO.

We should come out ahead on out-of-pocket expenses since in our worst-case year we spent some $15,000. My back-of-the-envelope guess without seeing actual policy documents is that our family could save from $2,000 to $4,000 annually with the cheapest HealthCare.gov policy. That's real money, especially considering that my current plan doesn't cover doctor's visits, drugs or clinical diagnostics. But I always reserve judgment until I see the fine print.

Can I get a comparable or better deal through an insurer on a private brokered exchange? When I first tried to compare the HealthCare.gov rates with an online private exchange I've used in the past — ehealthinsurance.com — I ran into an unexpected irony: Their server was down, too. (More on that next week.)

To date, my customer service experience with HealthCare.gov has been worse than that with my cable television/internet provider, which has often been dreadful over the years. I was told by the HealthCare.gov rep that my application would take three weeks to process. It takes less time to order a whole house of appliances, have them delivered and installed – with a cable hook-up.Still, it's vexing to me — and millions of other Americans in my situation — that the government didn't hire some competent contractors to get HealthCare.gov up and running. They had three years. Meanwhile, the political liability is still ballooning for the Obama administration and fellow Democrats.

That’s not an encouraging sign for a program that will need to attract millions of customers to work as intended and has struggled to get those sign-ups so far. Through the first month of the exchange's existence, nearly 60 percent of "potentially eligible adults" said they were aware of the marketplace, although only one in five actually enrolled, according to a survey by the Commonwealth Fund (PDF).

An even greater concern is the report that only one-fifth of site visitors were in the coveted 19-29-year-old demographic, a key group that can help balance overall expenses and premiums.

The troubles thus far don't mean that the health care marketplaces can't work — or provide lower-cost insurance. Yet potential customers throughout the entire country are still on hold. Will they hang up for good before the system gets fixed?