Stocks are surging again, with the S&P 500, Nasdaq Composite and NYSE Composite Index at new record highs to start the week. That puts an end to the long, listless churn that has seen the market bounce around without much upward progress as investors contended with factors like the Ebola scare or whatever was happening with Greece.

Related: Stock Hit New Records. Chances Are You Missed Out

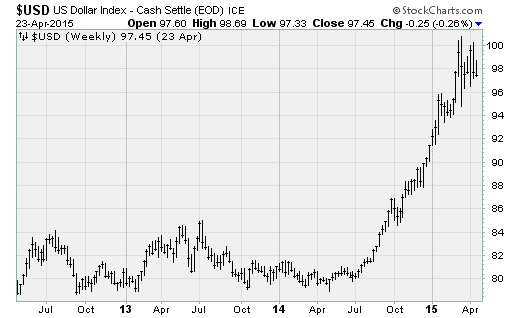

While all the focus has been on technology stocks amid solid earnings and new products that helped bring the Nasdaq above its dotcom-era closing high, the real catalyst for all this is what's happening with the U.S. dollar — specifically, a nascent selloff in the greenback that looks set to at least partially reverse the powerful uptrend that started in July and drove stocks into a stasis.

Here's why:

A broad swath of assets are set to benefit from the dollar's pullback, including crude oil, copper, precious metals and the stocks connected to these goods. Energy, materials, steelmakers and mining names have all been on the move recently.

For example, the Market Vectors Steel ETF (SLX) was up more than 9 percent in the three days through Friday — the best performance since September 2012. Energy stocks, as represented by the Energy Select Sector SPDR (XLE), are threating to push into territory not seen since November. Wholesale gasoline futures have pushed over $2 a gallon for the first time since November, up nearly 63 percent from the low set in January at $1.23 a gallon.

This reversal is good news because it will alleviate some of the pressure the U.S. economy has suffered.

Credit Suisse notes the dollar's strength — up nearly 28 percent trough-to-peak from last May's low to a high set in March — is a clear negative for net exports as well as industrial production and manufacturing activity. The impact on GDP growth is masked by offsets such as lower energy prices (which boosts consumer purchasing power) but is still negative, on balance.

Some quick back-of-the-envelope calculations by Credit Suisse flesh this out. Holding everything else constant, every 10 percent rise in the dollar lowers exports by about 2.4 percent, or $50 billion. This, in turn, would result in the loss of about 290,000 jobs.

The dollar's rise has also been a drag on corporate earnings since it reduces the value of profits when they are repatriated into the U.S. As a rough estimate, about 30 percent of national corporate profits are accounted for by foreign earnings according to data from the Bureau of Economic Analysis.

Related: Corporate Tax Havens Stiff Taxpayers by $110B A Year

Heading into the current first-quarter earnings season, FactSet data revealed that for non-energy companies with 50 percent or more of sales coming from inside the U.S., earnings growth was expected to be 5.9 percent; yet for those with less than 50 percent of sales coming from inside the country, earnings were expected to decline -1.3 percent.

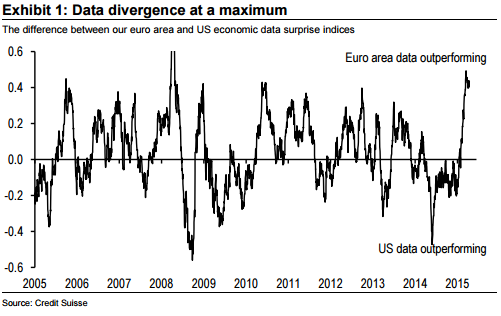

Two big factors are driving the turnaround we're seeing. First, the relative flow of the economic data in the U.S. compared to Europe and Japan has flipped, as we should expect: The U.S. is suddenly looking vulnerable just as new stimulus efforts and cheaper currency valuations are juicing growth overseas.

To drive the point home, Credit Suisse analysts believe annualized Eurozone GDP growth could print as high as 3 percent for the first quarter while the Atlanta Fed's GDPNow estimate of U.S. Q1 GDP growth stands at just 0.1 percent. As the chart below illustrates, the data divergence recently reached an extreme not seen since 2008. Currency valuations, among other things, respond to relative economic strength.

The second factor is that the path of monetary policy stimulus is shifting as well. A few months ago, it was all about the European Central Bank's new bond-buying stimulus and the Federal Reserve's looming rate liftoff. Now, there is already chatter about when the ECB should start tapering its purchases while the timing of the Fed's first interest rate hike since 2006 is being pushed back, possibly into early 2016 (based on probabilities from the futures market).

Over the last few weeks, Fed officials have been talking up their concerns about the consequences of the dollar's impressive rise over the past year — including the drag on the foreign earnings of U.S. businesses and the dampening effect on inflation (which is already below target) via the dollar's role in lower energy prices.

Related: Paul Volcker Isn’t Worried About Low Inflation. You Shouldn’t Be Either

Boston Fed President Eric Rosengren admitted that a strong dollar makes it harder for the central bank to reach its employment and inflation goals. New York Fed President William Dudley blamed the dollar's rise on contributing to a slowdown in U.S. economic growth. And Atlanta Fed President Dennis Lockhart noted that the dollar's lofty valuation is bringing down net exports.

Including these concerns in the Fed's next policy announcement on April 29 could pull the U.S. dollar down further. That should amplify the gains we've seen recently, boosting dollar-sensitive assets like gold and silver that have been in the doghouse for months.

Top Reads from The Fiscal Times: