The stock market's rebound out of its August-September unpleasantness has been nothing if not impressive. The S&P 500 has moved above its 200-day moving average, rebounding 11 percent from its late September low to return to levels seen on August 19.

The sea change could not be more dramatic. And it could set the stage for a last-gasp, late-stage dotcom-era style market melt up.

Measures of sentiment and investor positioning had plunged to recession-like levels, driven by an amorphous, currency-driven problem overseas (China's market losses), indications of a slowdown in the economic data, earnings headwinds (again, mainly caused by currencies and China) and fears over the impact of possible monetary policy tightening by the Federal Reserve. It looked as though recent speculative excesses (in areas like big tech and biotech) were about to be unwound.

Related: Baby Boomers Face a Shocking Retirement Savings Shortfall

All of this seems eerily similar to the action surrounding the market's behavior in the late 1990s, when the Federal Reserve was forced to reverse course after a small rate hike in 1997, dropping rates nearly a percentage point into a low in 1998 that ignited the final phase of the dotcom bubble.

The atmospherics are striking. After reporting solid earnings, large tech stocks like Microsoft (MSFT) are surging to new highs. The Nasdaq Composite looks ready for another run at its dotcom era high of 5,132 after drifting away from the new record it set back in July. The faith in this bull cycle — centered on the belief in the infallibility of central bankers and of monetary policy stimulus — is still gaining new converts.

The uptrend out of the September lows was ignited by a walking back of futures market odds of rate liftoff by the Federal Reserve to March 2016 or beyond. It achieved acceleration on hints from the European Central Bank that it was considering pushing its policy deposit interest rate deeper into negative territory to combat deflation and economic stalling. Then it reached terminal velocity last week on an interest rate cut by the People's Bank of China.

Any quibble is summarily dismissed by the comfort of the promise of cheap money. Never mind the underwhelming corporate revenue growth (of the S&P 500 companies that have reported quarterly results so far, just 43 percent are beating on the top-line vs. the typical 60 percent over the past two years). Don’t be shaken by evidence of economic stalling here at home (Macroeconomic Advisors' tracking estimate of third quarter GDP growth is at 1.5 percent with the fourth quarter at 2.4 percent). The central banks are on it.

Related: Why We Might Be Headed for a Recession in 2016

Until that near-religious belief is broken, either by uncontrollable deflation, premature policy tightening or a surge of wage-driven inflation, the uptrend is unshakable. Don’t fight the Fed — or the tape.

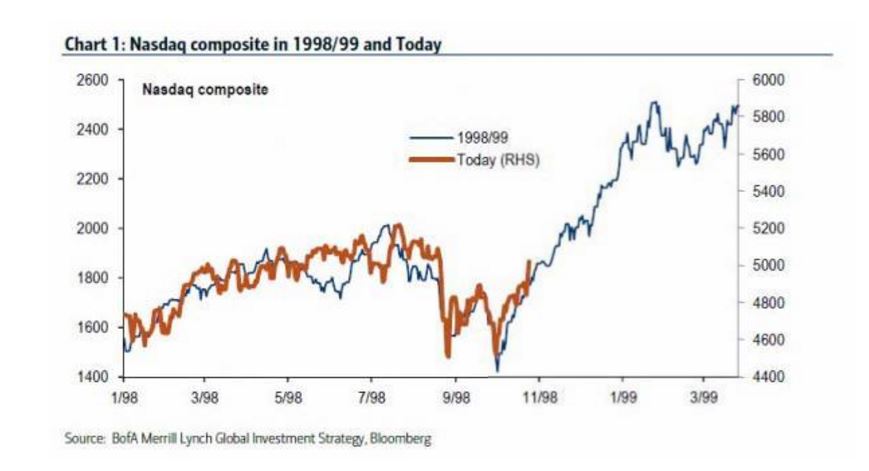

Wall Street is noticing the parallels to the late ’90s, with Bank of America Merrill Lynch analysts circulating the chart above overlaying the current rise in the Nasdaq to the movements between 1998 and 1999. Then, like now, a bull market and U.S.-led economic expansion was suddenly interrupted by problems in emerging market economies. Once the issues started hitting Main Street U.S.A., global policymakers responded and monetary policy was eased — powering a narrow but powerful final meltup rally.

Back then, BoAML analysts note, it was a "barbell" of high-growth dotcom stocks as well as deep-value emerging market/Russia stocks that outperformed. If a repeat is really about to happen, I would focus on tech stocks like Microsoft and Apple (AAPL) as well as areas of value such as industrials, energy and materials.

Yet BoAML's chief investment strategist, Michael Hartnett, warns that an exact repeat, despite the positive indications on the surface, isn't likely and is telling clients to sell into any end-of-year market rally.

Market breadth certainly suggests that one should view the current rebound skeptically: One measure, comparing the performance of the "equal weight" S&P 500 to the normal S&P 500 that favors stocks like Apple with large market capitalizations, suggests that larger stocks are dominating overall performance in a way not seen in over two years.

Moreover, as Hartnett lays out, the global macroeconomic picture is one of "deflationary expansion," while the market is threatened by the "end of excess liquidity" and the "end of excess profits." Second, while investors got nervous over the last few months, they didn't reach panic levels — and an economic recession was never the base-case expectation. And third, Hartnett believes investors will demand not only fresh central bank stimulus but evidence that it’s translating into a rebound in corporate profitability.

This last point will depend on the Federal Reserve turning dovish enough at its policy meetings this week and again in December to weaken the U.S. dollar and reverse the dynamic of a strong dollar/weak EM currencies/weak commodities/weak energy/weak profits that's been in play over the past year — but also do it in a way that expresses confidence in the growth prospects of the economy.

If Fed Chair Janet Yellen can accomplish this, stocks should be able to zoom to new record highs heading into the New Year's holiday before rate hike concerns resurface once the calendar flips to 2016.