Cold weather is heating up the U.S. stock market

As crude oil prices rebounded from 12-year lows reached earlier last week, climbing back above $31 a barrel on hopes that cold temperatures in the U.S. and Europe would increase demand for heating oil, stocks followed suit.

Whether this rally — up two straight sessions! — is a classic "dead cat" bounce or the start of the next sustainable up leg in an already historic post-2009 bull market ultimately depends on the policy response from the Federal Reserve, the European Central Bank and the rest of the world's major central banks. Investors — as they did during the 2010 Greek debt crisis, the 2011 fiscal standoff and the 2012 growth scare — once again are looking for monetary policy deliverance.

With sentiment so bombed out, it won't take much to get the bulls to stampede. Yet there is a nagging fear that with interest rates already so low, and balance sheets already swollen by bond purchase programs, that the central banks are out of policy ammunition.

Related: Will the Fed Ride to Investors’ Rescue?

First and foremost, markets would get a lift on comments from the Federal Reserve — preferably from Chair Janet Yellen — that the December forecast for four quarter-point hikes in 2016 is no longer the most likely scenario given recent turmoil and crude oil’s test below $27 a barrel last week.

Remember, back in September the Fed held off on raising interest rates because of the August selloff in global markets. Specifically, policymakers were worried that recent "global economic and financial developments may restrain economic activity" as well as put "further downward pressure on inflation."

With the Russell 2000 small-cap index closing below the 1,000 level last Tuesday for the first time since 2013 and crude oil touching 2003 levels, it's hard to see how all of that doesn't apply again right now. Market-derived inflation expectations have slid back to early 2015 lows. The 10-year U.S. Treasury yield is testing below 2 percent again for the first time since October.

Related: 4 Reasons to Worry About Iran's Oil Coming to Market

The futures market is now only pricing in a single rate hike this year in the wake of a weak inflation report last week. A reduction in the Fed's own rate hike forecast to more closely align with where the market is would help alleviate concerns the institution is repeating the mistakes of 1937 — prematurely tightening on a still fragile economy.

Even better would be a restart of the quantitative easing or "QE" bond buying program that was halted in December 2014 — an idea being touted by noted investor Ray Dalio of Bridgewater. At the time, with job growth perking up, the economy stable and the federal deficit narrowing and limiting fresh Treasury bond supply, there was a fear the Fed's monthly T-bond purchases were creating a shortage of high-quality collateral needed for the inter-bank lending market.

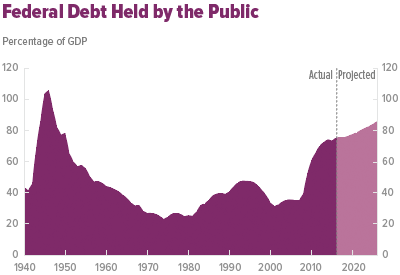

New estimates released last week by the Congressional Budget Office show the deficit will grow in 2016 for the first time 2009 and will likely continue to grow for the foreseeable future. As a result, the national debt will swell again, as shown above. That will increase the T-bond supply, allowing the Fed to restart QE if needed. (As an aside, this would also control the government's interest expense and encourage the kind of deficit spending fans of fiscal stimulus have been clamoring for.)

Related: 3 Money Moves to Make When Stocks Are Sinking

Fresh stimulus efforts by the other major central banks could also encourage investors. The European Central Bank, in its December meeting minutes released on Jan. 14, signaled it is already looking at expanding and extending its existing bond-buying program. Last Thursday, ECB chief Mario Draghi said a review and possible reconsideration was possible at the next policy meeting in March.

Making an effort toward what economists call "verbal easing," Draghi added during a Q&A exchange with the press that the ECB still has plenty of policy tools at its disposal as well as the power, willingness and determination to act.

The People's Bank of China is still likely to cut interest rates, too. The Bank of Canada appears to be on the verge of cutting rates into negative territory. And Bank of Japan Governor Haruhiko Kuroda has said that further monetary easing would happen if economic risks threatened to push inflation lower. The quarterly report on Japan's regional economics showed an ongoing lack of wage pressure.

Related: The Devil's Due — How China Could Send S&P 500 Below 666

Still, it's debatable that another surge of cheap money stimulus will solve the deeper, structural issues in play here, such as the epic oversupply in crude oil, China's bad debts, Europe's stagnation and a drop in corporate profitability coming as the U.S. labor market finally tightens.

Nor is it clear that the Fed wants to play the role of savior right now. After all, the Fed wasn't holding out much hope for higher inflation anyway: Its December forecast showed below-target inflation all the way through 2018. Perhaps Yellen has turned hawkish, satisfied with stable prices and stable job growth (which is her statutory mandate, after all) despite stock market losses — a scary thought indeed for those relying on the "Fed put" to save their 401(k)s.