Breakthroughs in medicine and technology and a growing focus on physical fitness and better diets have extended human lifespans by 30 years since 1900. The average lifespan is now 79, compared to 73 just three decades ago.

Related: Here’s the Best State for Older Americans – and the Worst

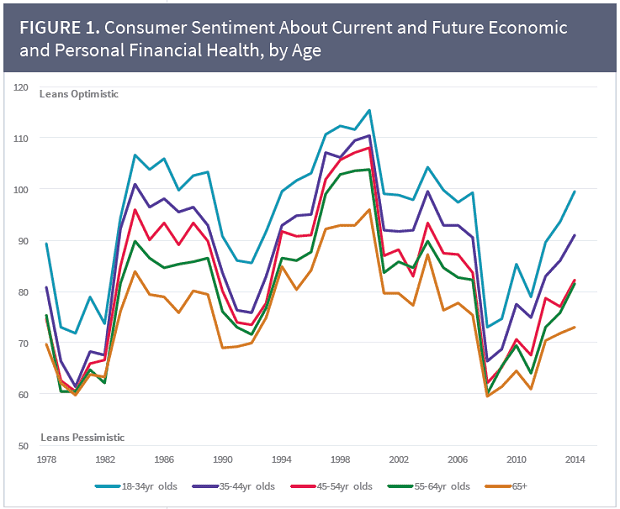

At the same time, new research by United Income, an investment advisory service in Washington, D.C., shows that Americans’ pessimism and unease about the state of the economy and their own future financial well-being grows the longer they live.

Paradoxically, even as psychological studies show that people generally become happier about their lives the older they get, they nonetheless are “overly pessimistic” about their financial futures, according to the analysis.

The report not only highlights growing economic anxiety among an increasingly important and influential cohort of the population, but also suggests that this overarching pessimism and caution could adversely affect the economy and slow GDP growth.

The report found that an “optimism gap” between younger and older Americans increased by three percent for every year added to the life expectancy of average adults. This is manifested in a growing tendency on the part of the elderly to curb purchases, steer clear of even slightly risky equities and expect the worst from the markets when it comes to their personal finances.

In 2014, for example, adults over the age of 64 were 40 percent less optimistic about their future financial well-being compared to adults under the age of 35. They were also 30 percent more skeptical about future economic growth and 40 percent less convinced of future stock market increases than younger Americans.

Slideshow: The 15 Best States for Seniors

However, this pessimism doesn’t comport with the actual performance of the markets; most major stock market indexes increased in all but two of the years between 2002 and 2014, the years covered in the study. The new report sees this as an ominous sign that could put senior’s health and financial wherewithal at risk.

“The benefits of longer lives and retirement may be limited if older households curb their consumption or investment in preventive health measures because they are overly pessimistic about their future financial health,” the study warned. “An overly negative viewpoint toward the future may also create self-fulfilling economic problems if it leads to an overly aggressive fixed-income portfolio.”

And that pessimism translates into declining purchases and consumption.

Given recent trends, the average adult 60 or older will curb his or her spending by about 2.5 percent every year, or by about 20 percent over a decade, according to the study. Also, that decline in consumption accelerates as people reach their 80s.

Related: Why Carrying a Mortgage in Retirement Can Really Pay Off

This rising financial pessimism as the life span continues to widen could have profound economic consequences for the country in the coming decades, according to the survey’s authors. Some 43.1 million people were 65 or older in 2012, or 14.5 percent of the total population, according to the Census Bureau. By 2050, that total will soar to 98.2 million.

There is little doubt that this fast growing cohort will be a dominant factor in the economy as time goes by, with people 50 years and older holding the lion’s share of personal assets and commanding the most buying power of any other age group.

But Matt Fellowes, CEO of United Income and an expert on financial management and retirement, sees a threat to the economy in the coming years if overly cautious and gloomy consumers dictate future growth.

“So that sort of bulge of importance in the economy is only going to extend, and when that economy is being more and more dictated by people that are risk adverse and spending less than they can afford, it does hold back economic growth, there’s no question about it,” he said in an interview.

Related: A Big Reason Workers Aren’t Saving More for Retirement

“It’s literally the only population in America that may be under-consuming – and unfortunately a part of the population that owns more of the buying power,” Fellowes added. “So as the economy becomes more and more dependent on that population, there’s no question that the growth will be stunted.”

Fellowes says it’s too soon to gauge or project this potential elderly consumer drag on the economy, but he insists it will be substantial.

On a more emotional level, the new study suggests that financial worry among older Americans may be getting out of hand, as fears of inadequate savings or a sudden downturn in the markets are frightening many – and resulting in gloomy self-fulfilling prophecies.

“An overly negative viewpoint toward the future may also create self-fulfilling economic problems if it leads to an overly aggressive fixed-income portfolio,” the study says.

Related: The Retirement Revolution That Failed: Why the 401(k) Isn’t Working

Moreover, since consumer spending is correlated with sentiment, “older adults may lead more insular lives because they may feel relatively less free to travel and spend money on entertainment,” the report stated. “This more limited lifestyle can curb their mental health and, eventually, physical health.”

The study was based on a detailed study of data from the University of Michigan that was commissioned by the Social Security Administration and U.S. Commerce Department, among other federal agencies.

Among the report’s other key findings:

- On average, retired adults generally die with a similar amount of wealth regardless of what age they die. For instance, the average retired adult who dies in their 60s leaves behind $296,000 in net wealth, $313,000 in their 70s, and $238,000 in their 90s.

- Older Americans have been leaving increasingly larger estates. The size of estates grew by 130 percent between 2000-2002 and 2010-2012, although the growth in investable asset value size was just 20 percent.