U.S. corporations — like many Americans — exploit every available rule in the tax code to minimize the taxes they pay. The United States has one of the highest corporate tax rates in the world, at 35 percent (not including any state levies), yet the actual amount in corporate taxes that the government collects (“the effective tax rate”) is lower than those of Germany, Canada, Japan and China, among others. The reason is confusingly called “tax expenditures,” a doublespeak term designed to legitimize special interest tax breaks and loopholes.

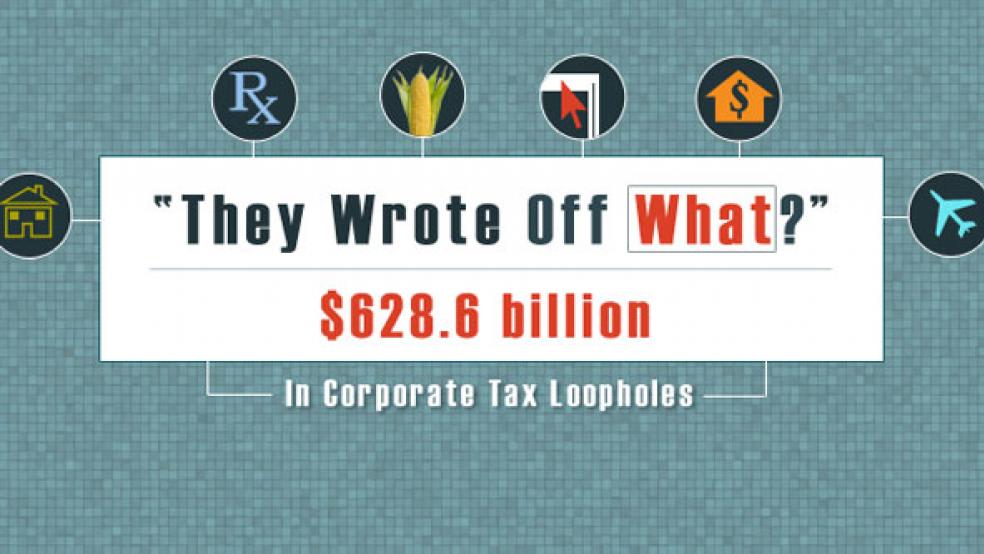

Those ‘expenditures’ will cost the U.S. government $628.6 billion over the next five years, according to a 2010 report from the Tax Foundation. With advice from the Urban Institute’s Eric Toder, one of the country’s foremost authorities on corporate tax policy, we assembled the 10 most costly corporate tax loopholes and who benefits from them.

10) Graduated Corporate Income

This policy places the first $50,000 of a corporation’s profit at a 15 percent tax rate, with higher profit levels garnering higher tax rates, until it tops out at 35 percent for taxable corporate income exceeding $335,000. The result is that an owner of a small corporation pays only 15 percent in taxes on the first $50,000 of profit, leaving more left over potentially for reinvestment and growth.

5-yr Cost to Government (2011-2015): $16.4 billion

Who benefits: Individuals that own small corporations.

9) Inventory Property Sales

Foreign income of American companies is taxed in the country in which it is generated, and the U.S. gives a tax credit for that amount in order to avoid double taxation. Some companies have accumulated a glut of such tax credits (the “inventory”), and in order to use them up, they artificially boost foreign income through a “title passage rule” that allows companies to allocate 50 percent of income from U.S. production sold in another country as income generated by that foreign country (the “property sales”).

5-yr Cost to Government: $16.7 billion

Who benefits: Multinationals with operations in high-tax foreign countries.

8) Research and Experimentation Tax Credit

Intended to spur research and development within companies, in its simplest form this break allows for a 20 percent tax credit for “qualified research expenses.” There are more complex applications, as well. Detractors complain that it is paying corporations to do research they would have done anyway.

5-yr Cost to Government: $29.8 billion

Who benefits: Pharmaceutical companies, high tech companies, engineers, agriculture conglomerates.

7) Deferred Taxes for Financial Firms on Certain Income Earned Overseas

Because most financial firms conduct their foreign operations as branches rather than as subsidiaries, as most companies in other industries do, they do not benefit from the tax breaks afforded to foreign subsidiaries. To compensate, this loophole enables financial firms to treat income from their foreign branches as if they were subsidiaries, along with all of the attendant tax benefits.

5-yr Cost to Government: $29.9 billion

Who benefits: Any financial firm with foreign operations.

6) Alcohol Fuel Credit

This is a tax credit for the production of alcohol-based fuel, most commonly ethanol, which is made from corn. The credit ranges from $0.39 to $0.60 per gallon. In theory, the credit is meant to encourage alternative forms of energy to imported oil. It is largely responsible for propping up the price of corn, and is extremely popular in corn-producing states like Iowa and Illinois.

5-yr Cost to Government: $32 billion

Who benefits: Food and agricultural conglomerates in the Midwest.

5) Credit for Low-Income Housing Investments

As you might expect, this one gives tax breaks to companies that develop low-income housing. It’s the rule that’s responsible for so many larger new developments setting aside 20 percent or 40 percent of their units for people whose income is well below the area’s median gross income.

5-yr Cost to Government: $34.5 billion

Who benefits: Real estate developers.

4) Accelerated Depreciation of Machinery and Equipment

This one allows companies to deduct for all of the depreciation of a piece of equipment at once (as opposed to over the, say, 20 years it actually takes the item to depreciate). This is the equivalent of the U.S. government giving the company an up-front, interest free loan. Congress recently made this expenditure temporarily even larger for 2011, to encourage investment in equipment.

5-yr Cost to Government: $51.7 billion

Who benefits: Airlines and manufacturers using large equipment that lasts many years.

3) Deduction for Domestic Manufacturing

This loophole enables a tax deduction for manufacturing activities conducted by American companies within the United States. It covers conventional manufacturers, but also extends to industries like software development and film production. The intent is to keep manufacturing from being outsourced.

5-yr Cost to Government: $58 billion

Who benefits: Any U.S. company that produces a product within U.S. borders.

2) Exclusion of Interest on State and Local Bonds

Companies (and individuals) do not pay federal income tax on interest from their investments in state and municipal bonds. What’s more, private companies can in some cases issue tax-free bonds of their own for projects that benefit the public, such as construction of an airport, stadium or hospital.

5-yr Cost to Government: $59.8 billion

Who benefits: High-income investors and corporations.

1) Deferral of Income from Controlled Foreign Corporations

Multinational companies can defer paying U.S. income taxes until they transfer overseas profits back to the United States, under this law. In practice, many companies leave much of their profits overseas indefinitely, thus paying only the tax in the relevant foreign country, which is likely far lower than the U.S. rate, and avoiding U.S. taxes permanently. The list of corporations enlisting this loophole is seemingly endless.

5-yr Cost to Government: $172.1 billion

Who benefits: Every multinational company.

Related Links:

The Paradox of Corporate Taxes (The New York Times)

Obama Calls for Cut in Corporate Tax, Loopholes (Reuters)

Some Perspective on Corporate Tax Loopholes (Tax Foundation)