The Dow Jones Industrial Average topped the 18,000 level for the first time ever on Tuesday. That's quite a feat, made all the more impressive by the way it happened, coming out of the early December weakness. Up for five days in a row, the Dow has surged 1,000 points in just one week.

Historically, December is the best single month of the year for large-cap stocks — Santa Claus rallies and all that good cheer. And the market has been demonstrating some remarkable consistency lately, with the S&P 500 rising for 29 consecutive days coming out of the October low. That had never happened before.

Related: How Warren Buffett Beat the Market Again in 2014

We're in the midst of some impressive long-term consistency as well. The S&P 500 has set its 51st new closing high of the year and looks set to end December above its five-month moving average for the 30th consecutive month. And so here we are, heading into 2015 with the bulls at full charge.

Have they overdone it?

There is a nagging sense — among some investors, at least — that stocks have maybe, just maybe, outrun the fundamentals supporting lofty valuations. Currently, cyclically adjusted price-to-earnings multiples on the S&P 500 have only been higher in the run up to the 1929, 2000 and 2007 market peaks. Currently, the multiple stands at 27.1 times earnings vs. a long-term average going back to the 1880s of 16.6. So stocks are more than fully valued.

The problem is that stocks have risen so far and so fast, they're already on the cusp of many 2015 end-of-year market forecasts by Wall Street analysts.

Jonathan Glionna at Barclays Capital is looking for S&P 500 earnings growth to slow modestly next year for an end of year target of 2,100 — just 0.8 percent above Tuesday's closing level.

His concern is that corporate profitability, which has been running at record highs, will come under pressure from lower energy prices (a drag on energy revenue), a need for increased capital expenditures, and a tightening labor market. Other factors that have been boosting the bottom line include lower effective tax rates and lower financing costs. Both of these could also see a reversal in the months to come.

Related: Your Year-End Money-Saving Tax Check

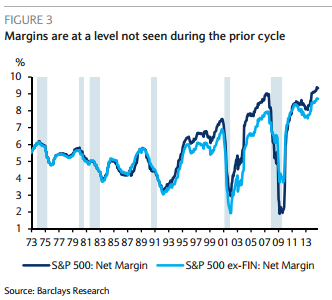

He notes that the S&P 500's overall profit margin stands at 9.4 percent — which is 1 percentage point above the peak profitability in the last business cycle and 3.5 percentage points above the long-term average. This is not sustainable, especially since it has come at the expense of labor's share of income, a continuation of which would keep the pressure on America's middle class families.

It seems that a change is already in the air.

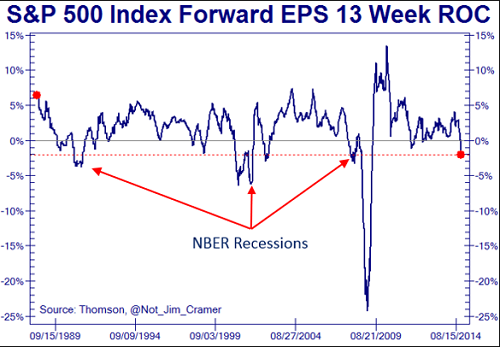

The chart above, compiled from Thomson Reuters data, shows that forward earnings revisions are already dropping at a pace normally associated with economic recessions as well as the profits recession of 1998. The energy sector plays a role here. Deutsche Bank strategist David Bianco, in a recent note to clients, warned that the 1998 profits pullback, like now, was driven largely by a rapid pullback in energy price.

Bianco's year-end S&P 500 target stands at 2,150 — a gain of just 3 percent or so from here. So by all means, celebrate another year of market merriness. Just don’t expect it to keep going forever.

Top Reads from The Fiscal Times: