4 Ways to Fix Social Security

Social Security celebrates its 80th birthday today, and the popular program that provides paychecks for 44 million elderly Americans is in need of a safety net of its own.

As the amount claimed by recipients continues to outpace the amount of money contributed by workers, the system will need to dip into its reserves to keep up with its obligations by 2020. Within 15 years after that (if nothing changes), those reserves will be gone and the system will only be able to pay 77 cents on every dollar owed, an amount that will continue to decrease with time.

The problem is even more acute given that future retirees won’t have the same access to pensions that many current retirees use to fund their retirement, and younger workers haven’t saved nearly enough to cover the costs they’ll face when they stop working.

To close the projected gap, the country needs to raise revenue, reduce benefits or some combination of the two. Here are four of the most commonly proposed solutions:

1. Raise the retirement age. For most Americans, the full retirement age (at which you can get full benefits) ranges from 65 through 67. Advocates of this solution would reduce the amount the government pays in Social Security by gradually pushing back the age at which you’re eligible for full benefits.

The drawback: Many Americans are already forced into retirement before they reach age 65. If they claim early and receive reduced benefits they may not have enough money to meet their basic needs. Also, workers in physically demanding jobs many not be able to work those extra years.

2. Raise the payroll cap. Social Security is funded via payroll taxes, which currently are only levied on the first $118,500 of income. That means that high earners effectively pay a much lower rate toward Social Security than others. Hiking or eliminating that cap, advocates say, would create a fairer system and increase revenue.

The drawback: Critics of this solution claim that increasing taxes on middle- and upper-income earners would reduce their income and stifle the country’s economic growth.

Related: 6 Popular Social Security Myths Busted

3. Institute a means test. While the vast majority of recipients (80 percent, per AARP) rely on Social Security as an integral part of funding their retirement, extremely high net worth individuals don’t need the additional income. This solution would create a net worth or retirement income threshold over which eligibility for social security phases out.

The drawbacks: It could be politically difficult to settle on a threshold, which might vary depending on the geography of a recipient. Plus, this would require people to pay into a system from which they get no benefits.

4. Freeze the cost of living adjustment. Social Security payments have historically been adjusted based on inflation as measured by the Consumer Price Index. This has been minimal in recent years, but the long-term, compounding effect of inflation makes this provision incredibly expensive.The drawbacks: For many people, Social Security is the only inflation-linked retirement income stream that they have. Limiting it could push some retirees over the financial edge as prices rise.

How IBM Is Making Your Passwords Useless

For years, quantum computing has been hailed as a technology that could change the way the modern world works, but a long-standing technical issue has kept that potential from being realized. Now, in a paper published in the journal Nature last week, IBM scientists have taken a big step (see how I avoided the temptation to make a pun there?) toward solving that problem — and while it could represent progress toward making quatum computers real, it also could mean that current cybersecurity standards will soon be much easier to crack. In other words, your passwords could be obsolete soon.

The power of quantum computing has some obvious appeal: The increase in processing power could speed up research, especially in big data applications. Problems with large datasets, or those that need many millions (or billions, or more) of simulations to develop a working theory, would be able to be run at speeds unthinkable today. This could mean giant leaps forward in medical research, where enhanced simulations can be used to test cancer treatments or work on the development of new vaccines for ebola, HIV, malaria and the other diseases. High-level physics labs like CERN could use the extra power to increase our understanding of the way the universe at large works.

But the most immediate impact for the regular person would be in the way your private information is kept safe. Current encryption relies on massively large prime numbers to encode your sensitive information. Using combinations of large prime numbers means that anyone trying to crack such encryption needs to attempt to factor at least one of those numbers to get into encrypted data. When you buy something from, say, Amazon, the connection between your computer and Amazon is encrypted using that basic system (it's more complicated than that, but that's the rough summary). The time it would take a digital computer to calculate these factors is essentially past the heat death of the universe. (Still, this won't help you if your password is password, or monkey, or 123456. Please, people, use a password manager.)

Quantum computing, however, increases processing speed and the actual nature of the computation so significantly that it reduces that time to nearly nothing, making current encryption much less secure.

The IBM researcher that could make that happen is complicated, and it requires some background explanation. For starters, while a "traditional" computing bit can be either a 0 or a 1, a quantum computing bit can have three (or infinite, depending on how you want to interpret the concept) states. More specifically, a qubit can be 0, 1, or both.

Up until now, the both part of that caused some problems in realizing the power of quantum computing.

Up until now, the both part of that caused some problems in realizing the power of quantum computing.

Apparently — and you'll have to take this on faith a bit, as it hurts my head to think about it — the both state can switch back to either 0 or 1 at any given point, and sometimes incorrectly, based on the logic in the programming. Think about when your phone freezes up for a second or two while you're matching tiles. This is its processor handling vast amounts of information and filtering out the operations that fail for any number of reasons, from buggy code to malware to basic electrical noise. When there are only the two binary states, this is a process that usually happens behind the scenes and quickly.

The hold-up with quantum computing up until now is that the vastly greater potential for errors has stymied attempts to identify and nullify them. One additional wrinkle in this reading quantum states is familiar to anyone with basic science fiction knowledge, or perhaps just the ailurophobics. What if the action of reading the qubit actually causes it to collapse to 0 or 1?

The very smart people at IBM think they've solved this. The actual technical explanation is involved, and well beyond my ability to fully follow, but the gist is that instead of just having the qubits arrayed in a lattice on their own, they are arranged such that neighbors essentially check each other, producing the ability to check the common read problems.

That opens the door to further quantum computing developments, including ones that will make your password a thing of the past. So, does this mean that you need to start hoarding gold? No, not yet. And hopefully before quantum computing reaches commercial, or even simply industrial/governmental levels, a better cyber security method will be in place. Or the robots will have already taken over. I for one welcome them.

Medicare Overpaid $251 Million in 18 Months for Drugs

By reimbursing certain drug providers based on outdated pricing, Medicare has squandered millions of dollars that could have been saved if the recommendations of a government watchdog had been followed.

As reported by The Washington Examiner, the Office of the Inspector General for the Health and Human Services Dept. found that Medicare has continued to pay providers of infusion drugs, which are delivered through IV pumps, at higher prices than necessary. HHS is paying providers based on 2003 prices when the drugs were more expensive--this despite warnings from the IG, most recently in February, 2013.

“Medicare payment amounts for infusion drugs…substantially exceeded the estimated acquisition costs,” according to findings reported on the IG’s website.

The IG said that had its recommendations been implemented, $251 million would have been saved over an 18-month period.

The Centers for Medicare & Medicaid Services (CMS) apparently ignored the IG when it proposed that the agency push legislation that would have brought the method of reimbursement for infusion drugs in line with the process for other pharmaceuticals. As an alternative, the IG recommended that the CMS employ competitive bidding to supply infusion drugs.

“CMS partially concurred with the first recommendation, but has not taken steps toward seeking legislation,” The IG’s report said. “CMS concurred with the second recommendation but said subsequently that…infusion drugs will not be included in competitive bidding until at least 2017.”

So presumably the overpaying won’t stop anytime soon.

Why the Rich Tend to Cheat on Their Brokers

For affluent Americans, having more than one financial adviser has now become the norm.

One in three Americans with more than $100,000 in investable assets started a relationship with a new financial services firm last year, seeking to combine the strengths of various firms to gain advice and resources, according to a new study released Tuesday by Hearts & Wallets, a financial research platform for consumers.

Related: The 6 Times You Really Need a Financial Adviser

Hearts & Wallets also noted that 55 percent of consumers with $500,000 in investable assets or more work with three or more firms.

Contrary to the popular image of wealthy investors dialing up their Wall Street broker, the Hearts & Wallets survey found that affluent investors are more likely to use self-service firms — discount brokerages like E*Trade or TD Ameritrade — than full-service brokers. More than 70 percent of investors with $500,000 or more use those self-service brokers, even if it’s for smaller “play money” accounts, compared with 40 percent for full-service firms such as Ameriprise and Edward Jones.

“It’s astonishing the self-service competitive set has deeper reach into investors with $500,000-plus, engaging more affluent investors than the full-service competitive set,” said Laura Varas, Hearts & Wallets partner and co-founder, in a press release.

Related: 6 Traits of an Emerging Millionaire: Are You One?

Some wealthy investors use both. A common pattern is what Hearts & Wallets calls “stable two-timing,” or when investors balance a self-service firm with a full-service firm. Some consumers might even tap into multiple high-service firms to obtain different advice.

“Just as in retail stores, wealthy customers may trust and frequent a Bloomingdale’s, but they will still shop at Costco, too,” Varas said. “Smart consumers compare.”

Top Reads from The Fiscal Times:

- The 5 Worst Money Mistakes of Millionaires

- IRAs: Everything You Need to Know for 2015

- The Worst States For Retirement in 2015

How Men and Women Differ When Buying New Cars

We all know men and women are different when it comes to money. Studies have found that women tend to be less self-assured and thus more considered and conservative in making financial decisions. That carries through to buying a new car, as the infographic below from Kelley Blue Book shows.

Recent surveys have found that Americans are increasingly skipping repeat visits to dealers’ lots — and in some cases even bypassing test drives — in favor of online research. Even so, the KBB study of about 40,000 U.S. adults found that women are more interested in features and safety while men are more likely to focus on styling and pursue a specific brand and model. KBB also found that, “while men are more likely to view their cars as tied to their image and accomplishments, women are more likely to see them simply as a way to get from point A to point B.” As a result, men want more trucks and luxury sedans while women are more likely to go for non-luxury Asian brands of SUVs and sedans.

Related: Car Sales Are on Pace to Do Something They Haven’t in 50 Years

Here are some other differences in how the car-buying process plays out:

Pentagon Doesn’t Know What Happened to $1.3 Billion in Afghanistan

The Pentagon isn’t able to tell federal auditors what happened to more than $1.3 billion in funds intended for construction projects in Afghanistan.

The money was dispersed through a program established to speed up the rebuilding process in Afghanistan by giving money directly to military officers to build roads, bridges, dams and other projects to avoid the lengthy bureaucratic procurement process.

But in the rush to spend and build, much of the money paid out by the Commander’s Emergency Response Program (CERP) between 2004 and 2014 has gone unaccounted for, according to auditors who spent the last year trying to find it.

Related: 7 Threats to U.S. Rebuilding Efforts in Afghanistan

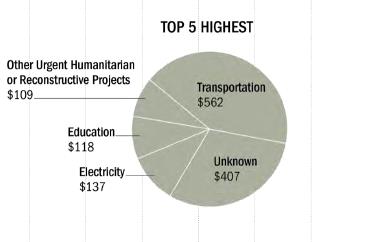

A new report released Friday by the Special Inspector General for Afghanistan Reconstruction says the Defense Department could only provide its office with documentation for $890 million, or roughly 40 percent, of the total $2.2 billion in funds.

The auditors blamed the Pentagon’s financial and project management process for not sufficiently tracking spending, saying DoD’s system doesn’t contain enough data or comprehensive information relating to the actual costs of the projects.

The auditors took the information the Pentagon did provide and divided it up into categories like education, health care, water and sanitation. Aside from transportation, the item that had the most expenses was labeled “unknown.”

U.S. Central Command responded to the inspector general’s findings, or lack thereof, by saying that some of the unaccounted for CERP funds had been shifted to other military needs. “Although the report is technically accurate, it did not discuss the counterinsurgency strategies in relationship to CERP,” the Central Command said.

In total, the U.S. has doled out about $3.7 billion through CERP funds, with $2.2 billion coming from the Defense Department.

This is just the latest report from SIGAR highlighting the Pentagon’s problems keeping track of the enormous amount of money flowing into Afghanistan. Earlier reporting suggested the U.S. has lost some $100 billion in the reconstruction efforts.