Health care costs have been rising at historically modest rates for a decade now, prompting a considerable amount of discussion and debate by economists about whether the trend can continue. Most workers, though, would probably be asking another question: What the heck are they talking about?

Since 2005, premiums have grown an average of 5 percent a year, sharply lower than the 11 percent average annual increase between 1999 and 2005, according to the Kaiser Family Foundation. That trend continued in 2015, with the average premium rising a modest 4 percent, according to an annual survey of nearly 2,000 employers by the Kaiser foundation and the Health Research & Educational Trust released last week.

Related: 4 Simple Ways to Save Money on Health Care

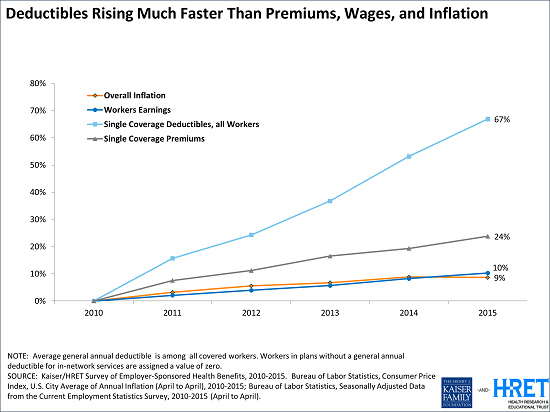

But Drew Altman, the CEO of the Kaiser Family Foundation, says that shift has been “all but invisible” to consumers because deductibles have been climbing at a substantially faster rate.

“With deductibles rising so much faster than premiums and wages, it’s no surprise that consumers have not felt the slowdown in health spending,” Altman said.

And just to be clear, it’s not like premiums are falling: The average premium for an employer-provided family plan is now $17,545, up from $16,834 last year and from $10,880 in 2005. And workers have been paying a greater share of those premiums, as the chart below from Kaiser shows:

Deductibles, meanwhile, have skyrocketed. The average deductible for all covered workers this year is $1,077, up 67 percent from $646 in 2010. And as high deductible plans are becoming increasingly popular with employers, more employees are enrolled in them than ever. The percentage of employees who are in plans with an annual deductible of $1,000 or more has grown from 27 percent in 2010 to 46 percent in 2015.

Some analysts argue that the shift to high deductible plans is responsible for the slow growth in premiums. The trend keeps premiums rising at a lower pace, while at the same time increasing the amount that employees are responsible for paying on their own.

Related: Americans Rank Health Care as Top Financial Burden

One of the main reasons for the rise in these high deductible plans is the scheduled 2018 kick-in of the “Cadillac tax,” which levies a fee on employers offering high-cost insurance plans. The tax was originally meant to target only the top tier of plans, but the rising cost of health care means that more and more insurance options will be hit with the tax. Members of Congress on both sides of the aisle are trying to repeal the tax before it takes effect, but employers aren’t waiting for Congress to act and are actively taking steps to avoid hitting the Cadillac threshold — like introducing plans with lower premiums and higher deductibles.

A poll released last week by the Mercer benefits consulting arm of Marsh & McLennan found that because of the tax, 41 percent of employers surveyed had already implemented a high-deductible plan or were working on increasing enrollment in such plans, while another 25 percent were thinking about taking such steps.