Mel Watt broke his silence this week after four months at the helm of the Federal Housing Finance Agency. He effectively repositioned the conservator for Fannie Mae and Freddie Mac as a facilitator of mortgage lending, announcing a series of steps to lower standards on the mortgages they purchase, indirectly increasing access to homeownership for those with less-than-perfect credit scores.

Watt is not alone: The Federal Housing Administration, which insures many non-prime loans, rolled out a program that officials claim would expand credit as well, and Dodd-Frank rules mandating larger down payments for certain qualified mortgages will likely be abandoned.

Related: 6 Housing Trends That May Surprise You

Implicit in this coordinated effort is the notion that access to credit represents a major stumbling block for the stuttering housing market. Whether due to uncertainty from Congress on the future of housing finance, or just a paranoid legacy of a wave of foreclosures after the bubble’s collapse, lenders won’t risk mortgages on non-creditworthy borrowers, the story goes, and policymakers can kickstart housing, and the broader economy, simply by loosening standards.

But what if this looks at the question entirely the wrong way? What if the key problem in the housing market is not supply, but demand? Or, I should say, what if that’s the key problem in one of our housing markets? Because, to oversimplify a bit, there are basically two housing markets in America today: one for the rich and one for the rest.

At the high end, things have rebounded nicely. Luxury home sales jumped in the first quarter of 2014 to twice the historical average. And according to RealtyTrac, a whopping 43 percent of home sales last quarter were all-cash deals, including 80 percent in Manhattan. Part of this is due to institutional investors snapping up vacant properties to convert to rentals. But with those investor purchases slowing, the only buyers left to make all-cash deals are the wealthy, including foreign buyers picking up a getaway home in an urban playground like New York or Miami.

Related: The 10 Most Expensive Home Sales in America

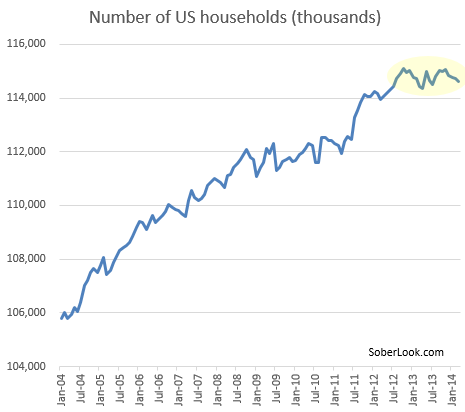

By contrast, the housing market for everyone else has flatlined. And because the 1 percent is only, well, 1 percent of the population, this reads like a stalled housing market, with the lowest homeownership rate since the mid-1990s, and a household formation rate that has basically not budged in three years.

The bifurcation of the housing market mirrors the nagging problem of income inequality in America. With all the income benefits in the post-recession period accruing to the 1 percent, it’s no surprise they alone have the confidence and financial stability to purchase homes. For the rest of the country, stagnant wages and job insecurity put an increasingly unaffordable market, with a double whammy of higher prices and higher mortgage interest rates, out of reach. Prospective homebuyers also have difficulty competing with attractive all-cash offers, remain scarred by the last decade’s bubble and bust, and continue to be pulled down by nagging household debt.

Months ago, I warned that rising student debt stood as an impediment to a housing recovery, with millennials preferring to delay major purchases while paying off their loans. New research from the New York Federal Reserve confirms that young borrowers with student debt are less likely to have mortgages than those without, despite the increased skills gained from higher education.

While this may just be a return to a pre-housing bubble normal, there are now so many more students graduating with debt, the impact on the housing market is greater. And it goes deeper than just debt. The job market for college graduates remains terrible, as it’s been for the past half-decade. Incomes for recent college graduates are down sharply from 2006. And the median net worth for graduates under 40 is a paltry $8,700. You cannot reasonably expect this cohort, traditionally the key entry-level group for housing, to jump into homeownership, no matter how easily they can secure a loan.

The two housing markets leads to a pernicious effect on housing construction. A growing argument on the technocratic left and the right assumes that relaxing zoning laws in desirable locations will lower the price of housing. And under normal rules of supply and demand, that would be true. In fact, this policy approach is actually happening in places like downtown Los Angeles and San Francisco, where 50,000 new housing units are in the pipeline, about half as much as have been built in the city since 1920.

It’s highly unlikely this will lead to cheaper housing, though, because the construction caters to the high-end luxury market, which happens to be the main group buying homes these days. And that’s true across the country. Incredibly, despite stagnant wages and a slow recovery, the size of new homes increased by more than 300 square feet in the last five years, setting a new record in 2013. Stories of increasing mansionization proliferate in Los Angeles, where homebuilders tear down bungalows on small lots and build multi-story single-family homes in their place. This has sent the median price on new homes to a record high. It’s hard to blame the builders – they’re merely following the demand in the market. Why make homes at the low end, if low-end buyers cannot afford them?

That’s why increasing access to credit in a shortsighted attempt to put more people into dubious mortgages won’t actually work. Efforts toward alleviating a major rental affordability crisis seem like a better preliminary step. And more fundamentally, if you want more people to buy homes, they have to earn more money. Current wage growth for the broad middle class will not sustain a robust housing market without the kind of shortcuts that created the last housing bubble. And nobody should pine for that to return.

We’re running a bold experiment in America to find out how much of the benefits of prosperity we can give to the very top without negative consequences. Considering that housing typically drives economic recovery, the distortions caused by a market that tends only to the rich are a flashing red light.

Top Reads from The Fiscal Times:

- How the U.S. Job Market Has Changed Dramatically in 15 Years

- The One Risk Businesses Worry About Most

- Why Economists Are Finally Taking Inequality Seriously

{kind=link}