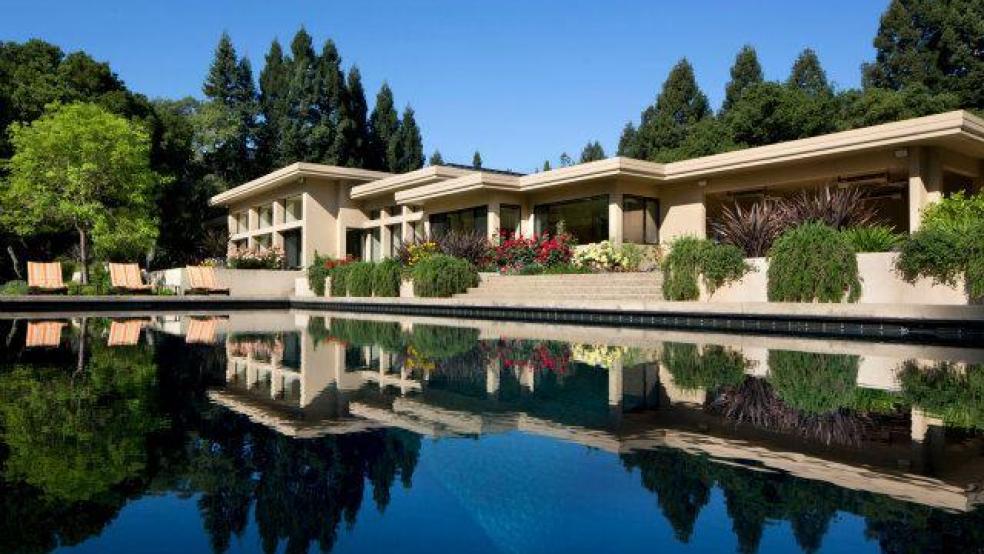

Sales of million-dollar homes are softening.

It's not a correction, experts caution, just something of a breather brought on by volatility in the U.S. stock market and an oversupply of luxury homes.

Sales of homes priced above $1 million fell 4 percent in July from a year ago, according to the National Association of Realtors. Activity is far more robust at the entry level and middle of the market, thanks to a drop in mortgage interest rates and pent-up demand. Luxury, however, doesn't rely on mortgages so much, but is far more sensitive to financial markets.

Related: The Main Reason Millennials Aren't Buying Homes

"That market was the first to recover after the financial crisis, but it's run its course," said Jonathan Miller of Miller Samuel, a real estate appraisal and consulting firm that tracks 18 real estate markets across the country, including New York, the Hamptons and Miami. "Part of it is aggressive pricing and part of it is excess supply."

Miami may as well be the poster child for excess supply. There are 79 towers with 12,573 units under construction in Miami-Dade County east of I-95, according to the Miami Association of Realtors. About 56 towers with 7,932 units are planned, but have not begun development. About 76 towers with 10,816 units are proposed in Miami-Dade County east of I-95 on the high end.

This, as inventory rose sharply in Miami Beach during the second quarter of this year and marketing time doubled. Luxury condo prices jumped a remarkable 20 percent, but closed sales fell by 21 percent. Prices will likely soften as sales fall further and supplies increase. The scenario is certainly magnified in Miami, but it is taking place in the luxury home market nationwide.

"That's where a large swath of development has gone on over the last five years, not just in single-family homes and condos but in rental product as well," Miller said.

Related: Homeownership Hits 51-Year Low, but There May Be a Silver Lining

Luxury home values nationwide fell in the first quarter of this year and recovered by barely 1 percent annually in the second quarter, according to Redfin, a real estate brokerage. Redfin defines a home as luxury if it is among the top 5 percent most-expensive homes sold in a city. Luxury home prices fell 11 percent in San Francisco and 4 percent in Bellevue, Washington, home to an outsized number of tech workers whose wealth is tied closely to the stock market.

"Existing sales above $1 million were down a bit in July. This was in large part due to the stock market volatility seen earlier this summer leading up to and immediately after Brexit," said Lawrence Yun, chief economist for the National Association of Realtors. "The financial markets have stabilized since then."

Luxury prices in the Hamptons, New York's swankiest vacation venue, fell 2.3 percent in the second quarter from the year-earlier period, but sales rose by more than 20 percent, according to Miller Samuel. That market is highly sensitive to the stock market, which swooned at the start of the year and then saw a volatile summer thanks to the Brexit vote.

Related: Tiny Homes Are Hot, and They're Going Upscale

While very high-end buyers don't rely much on financing, those in the $1 million to $2 million range do, and there may be some growth in that segment. An estimated $101.0 billion in jumbo mortgages were originated in the second quarter of 2016, up 31 percent from the previous quarter, according to Inside Mortgage Finance. Through the first half of 2016, roughly $178 billion in jumbos were originated, a 7.9 percent increase from the first half of 2015.

Luxury home builder Toll Brothers did report better-than-expected quarterly earnings in its last fiscal quarter, citing robust sales and new orders. The average price of a Toll home is around $850,000. Toll has benefited from very good land positions compared with other public builders seeking to sell to the luxury buyer. More builders now are finally moving away from pricier homes, seeing far more demand at the entry level, where supply is tight.

"We're seeing very robust activity in the entry space and the middle of the market, but we're not seeing it at the top," Miller said.

This piece originally appeared on CNBC. Read more at CNBC:

Mortgage applications up 2.8% but refinancing applications should be higher

We're in a new housing bubble: Why it's less scary this time

We're actually not married to this big homeowner tax break: Mortgage Bankers CEO