Americans Just Went on a $32 Billion Credit Card Shopping Spree

Americans may be heading for another credit card crunch. After paying down almost $35 billion in credit card debt in the first quarter of the year, consumer charged up a storm in the second quarter, racking up $32.1 billion in new debt, according to CardHub, a credit card comparison site. CardHub says that’s the second highest quarterly total since it began keeping data on credit card debt in 2009.

While that buying binge could potentially signal improved confidence in the economy and in their own financial prospects, CardHub warns that the debt risks are building. It projects that consumers will close out the year with an annual net increase of more than $60 billion in credit card debt, with the total credit card debt outstanding climbing to more than $900 billion, the highest since the recession.

Related: 5 Cities with the Most Credit Card Debt

CardHub CEO Odysseas Papadimitriou says that jump brings Americans “perilously close to a tipping point at which balances become unsustainable and delinquency rates skyrocket.”

For 7 out of the past 10 quarters, consumers have racked up more debt than they’ve paid off. Papadimitriou cites that as evidence that consumers are going back to the bad habits they had before the economic downturn.

CardHub based its study on data from the Federal Reserve, and if the results are a sign of trouble then another new report from the Federal Reserve Bank of New York suggests that problem is even worse than it looks. In a report called “Do We Know What We Owe,” the New York Fed found that people widely underestimate their credit card debt, telling the Fed’s survey-takers that it’s about 37 percent lower than what lenders say it is.

So if we are actually getting to a tipping point with credit card debt, it may be even closer than we realize.

Top Reads From The Fiscal Times

- Millions Facing a Hefty Increase in Medicare Premiums in 2016

- How Much Does Our Social Safety Net Cost? $742 Billion a Year and Rising

- The 10 Worst States for Property Taxes

Trump and Schumer Will Try to Scrap the Debt Ceiling

The president and the Senate Democratic leader agreed to seek out a more permanent debt ceiling solution that would end the perpetual cycle of fiscal standoffs. “There are a lot of good reasons to do that, so certainly that’s something that will be discussed," Trump said Thursday. It might not be easy, though, as conservatives see the borrowing limit as a way to keep government spending in check. Paul Ryan said Thursday he opposes doing away with the debt ceiling.

Is a Fix for Obamacare Taking Shape?

Senators on the Committee on Health, Education, Labor and Pensions heard from governors Thursday in the second of four scheduled hearings on stabilizing Obamacare. The common theme emerging from the testimony was flexibility: "Returning control to the states is prudent policy but also prudent politics," said Utah Gov. Gary Herbert, a Republican. He was joined by Democrat John Hickenlooper of Colorado, who said that states need room to innovate and learn from their mistakes. Much of what the governors said was in line with what the Senate panel is already considering, including the continuation of cost-sharing subsidies to insurance companies. (CBS News, Axios)

Senate Approves Trump's Deal with Dems. Will the House Go Along?

The Senate on Thursday voted to fund the government and increase the federal borrowing limit through December 8 as part of a deal that also included $15.25 billion in hurricane disaster relief funding and a short-term extension of the National Flood Insurance Program. The bill passed by a vote of 80-to-17, with only Republicans voting against the bill.

The package now goes back to the House, where it likely faces more strenuous resistance. The Republican Study Committee, a conservative caucus with more than 155 members, on Thursday announced it opposed the deal because it does not include spending cuts. Rep. Mark Walker, the group's chairman, sent a letter to House Speaker Paul Ryan listing 19 policy changes to "address the growing debt burden" or "begin draining the swamp" that could win conservative support for raising the debt ceiling. Some Democrats may also vote against the deal to signal their frustration with an agreement that they say weakened their hand in trying to protect undocumented immigrants who were brought into the country as children.

White House Backs Off Shutdown Threat…for Now

“Believe me, if we have to close down our government, we’re building that wall,” President Trump said of his planned border wall with Mexico 10 days ago. Just two days later, though, White House officials told Congress that a short-term spending bill to fund the government into December wouldn’t have to include $1.6 billion for the wall, The Washington Post reports.

Trump still wants money for the wall to be included in a December budget bill, and he could follow through on his shutdown threat at that point. For now, though, an agreement on a “continuing resolution” to keep the government running after September 30 seems likelier, allowing Congress to deal with some of the other pressing issues it faces this month.

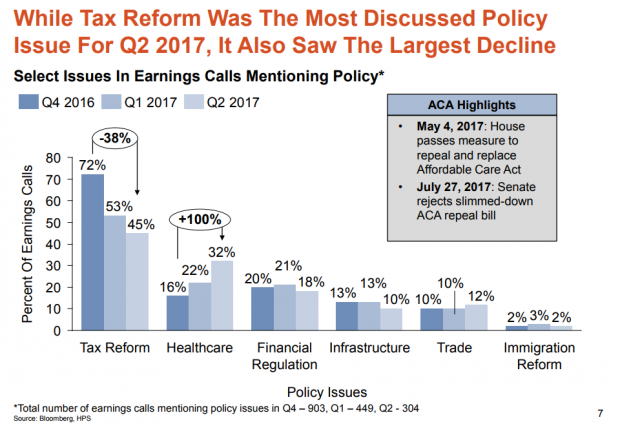

Which Trump Agenda Items Are Companies Talking About With Wall Street?

Hamilton Place Strategies, a public affairs consulting firm, analyzed transcripts of earnings calls by publicly traded U.S. companies over the last three quarters. They found that tax reform was the policy issue companies discussed most on those calls with Wall Street analysts — but that mentions of the subject dropped by 38 percent from the fourth quarter of 2016 to the second quarter of 2017. Overall, the percentage of earnings calls mentioning government or policy issues fell from 41 percent to 16 percent. Health-care reform saw the largest increase.

Does this mean that businesses have given up on tax reform this year? Perhaps. More likely, it's simply the result of a lack of action on the tax overhaul. Hamilton Place notes that mentions of tax policy peaked in February just after the Senate Finance Committee advanced Treasury Secretary Steven Mnuchin's nomination and have spiked after other tax-related announcements. So mentions of tax reform on earnings calls could surge again the fall.

One other note about what businesses have been discussing: Calls mentioning President Trump fell by 84 percent from January to late August.

08312017_HPS_Chart_of_the_day.PNG