For years, close observers of the financial crisis wondered why mortgage bond investors never stood up for themselves and demanded sufficient restitution from the banks who swindled them. Investors purchased trillions in mortgage-backed securities that the sellers knew were fraudulent, yet they never made a full-throttle effort to get their money back.

While homeowners were difficult to organize and had limited resources, the biggest institutional investors had deep pockets, and binding contracts that allowed them to recoup most of their losses if the mortgages they purchased did not meet prescribed underwriting standards. A mountain of evidence shows that, in fact, they didn’t: A recent Federal Housing Finance Agency Inspector General’s probe found errors in “almost every” mortgage bond deal examined.

Related: Two Housing Markets for the Two Americas

Now, at long last, the other shoe has begun to drop. An investor group led by Pimco and BlackRock, two of the largest bondholders in the world, sued six trustee banks in New York Supreme Court on Wednesday, opening up a new front in the war over who will bear the losses from the housing bubble’s collapse.

This seems at first glance like one set of rich people arguing with another, and in some ways it is. But there was a time when this raising of pressure on the perpetrators of the crisis would have been welcome news to everyone, as it could have triggered a needed restructuring in the mortgage industry. At this point, it may be too late, but with the future of housing finance still unresolved, having investors invoke their right to avoid a rip-off could still benefit innocent bystanders on Main Street.

Previous efforts by investors have focused on bond issuers, mostly the big banks who purchased loans and packaged them into securities. But you’d have to describe those efforts as half-hearted. After Bank of America rejected an investor-led request in 2010 to buy back $47 billion in poor-quality mortgage loans, the two sides reached a deal to settle the case for just $8.5 billion, about 8 percent of total losses. The eventual approval of that settlement led to copycat deals, also for just pennies on the dollar, compared to the actual damage incurred.

Related: The Biggest Policy Mistake of the Great Recession

Wednesday’s lawsuits instead target the trustee banks, facilitators of mortgage-backed securities deals who created the trusts for the underlying mortgages and oversaw payments to investors. Trustees had legal obligations under the securities contracts, and the lawsuits allege that they did not meet those responsibilities.

In particular, trustees were supposed to act as the agent for the investors with the bond issuers. If the mortgages did not meet stipulated quality standards, as numerous investigations have shown, the trustees were contractually required to force repurchases on the lenders and return the proceeds to investors. But Pimco, BlackRock and the other plaintiffs claim that they informed the trustees of what they call an “industrywide abandonment of underwriting guidelines,” and yet the trustees did nothing to advocate for their interests.

The trustee banks in the lawsuits include Deutsche Bank AG, US Bancorp, Citibank, Wells Fargo, HSBC and Bank of New York Mellon. The investors seek damages on approximately 2,200 mortgage-backed securities trusts, for losses that exceeded $250 billion, so the ultimate resolution could be extremely costly.

Trustees Betraying Trust

While the trustee banks had obligations to defend investors, they also had large conflicts of interest that prevented them from fulfilling their role. These large global mega-banks did business with all the bond issuers, and did not want to jeopardize that by forcing repurchases on them. Moreover, some trustees, like Citi and Wells Fargo, were divisions of banks that also issued bonds, and they wouldn’t want to set any precedents on absorbing losses that would affect their bank’s bottom line. The trustees aligned with the “sell-side,” the bond issuers, over the “buy side,” the investors.

So investors have a case to make that the trustees failed them. But making this case in 2014 will be much harder than it would have been in 2010 or 2011. A New York appeals court ruled last December that the six-year statute of limitations on breach-of-contract claims for mortgage-backed securities begins when the transaction is executed. Investors believe it should begin when they demand a repurchase. Defining when to start the clock will decide whether or not the investors have standing to sue.

This long delay for investors to invoke their rights had grave consequences for the country. When there was a multi-pronged assault on the banks and trustees — the threat of state and federal law enforcement actions, private lawsuits by homeowners resisting foreclosures, and investor pressure to repurchase bad mortgages — there was a glimmer of hope for a global solution, where losses would be more evenly distributed and homeowners could potentially stay in their homes.

Related: Economy May Never Fully Recover from Crisis

But the government’s efforts to hold banks accountable led to sweetheart deals (witness this week’s settlement with SunTrust Bank, delivering 48,000 foreclosure victims relief totaling a paltry $833 each). The courts basically crushed individual homeowner struggles to fight the banks. Investor leverage to rework the system has significantly weakened, thanks to their hesitancy. They also may not even be able to seek damages at this point.

If successful, though, the investor revolt against trustees could have a beneficial outcome. Congress is embroiled in a debate over what to do about the housing finance market. Most of the plans pave the way for a return to the private-label mortgage-backed securities system that helped lead to the crisis. By filing this case now, investors are in their own way trying to affect that debate, by demanding stronger investor protections before they throw one dime into a reconstituted mortgage bond market.

The Association of Institutional Investors wants trustees bound to an “unambiguous fiduciary standard,” so they will be even more obligated to act in the best interests of the bondholders. A suit against trustees for breaking their promises will strengthen this argument, showing that more protections are necessary. (Ironically, the argument would be even stronger if investors happen to lose, which could account for the delay.)

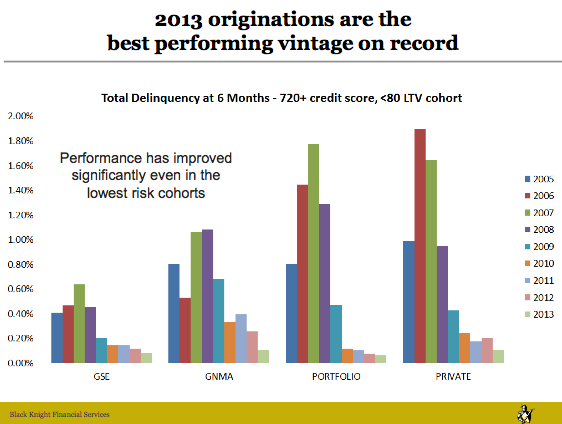

Ultimately, this could help protect the public. Trustees that safeguard investors in mortgage bonds will be more wary of shoddy deals carrying toxic mortgages. That reduces the market for such bad loans, meaning lenders will write less of them. In the current housing finance market, Fannie Mae and Freddie Mac’s high quality standard has led mortgage loans granted in 2013 to be the best performing on record. Strict investor protections and trustees in a watchdog role could at least be an attempt to replicate this. And that means less dangerous home loans for everyone.

On one level, the investor/trustee dispute could be dismissed by ordinary Americans as high-class warfare between the 1 percent and the 1 percent. But creating markets with incentives against cheating, instead of for it, is in all of our interests.

Top Reads from The Fiscal Times:

{kind=link}