For stocks, two big dynamics are in play right now: A stalling of corporate earnings growth and the anticipation of higher interest rates as the Federal Reserve prepares its first policy tightening cycle since 2004.

You’ve likely heard that already, from me or from others, but you may not recognize the potential significance for your portfolio: These two major factors could keep a lid on price gains well into 2016 — which is when it'll become clear whether or not the U.S. economy is strong enough to handle the Fed's higher interest rates.

Related: Forget the Fundamentals, This Market Is About Just One Thing

Credit Suisse researchers went back and looked at the trends around the start of the Fed's last three rate hike cycles in 1994, 1999 and 2004. The takeaways were as follows:

- Stocks tend to suffer a short-term period of turbulence near the start of rate liftoff.

- Valuation multiples contracted during the 1994-1995 and 1999-2000 rate hikes, but were range bound in 2004-2006.

- In two of these three occurrences, the pullback in stocks proved to be a buying opportunity ahead of new highs (1999 and 2004).

- Small caps tended to get hit harder than large caps.

Timing, like so much in life, is critical — but hard to nail down. Credit Suisse found that valuation multiples came under pressure in a window ranging from six months before a rate hike right until action was taken. Regardless of whether the Fed takes action in June, or the more likely date for liftoff in September, we're right in the thick of it now.

You'd never guess that smaller stocks suffered more from the way the Russell 2000 has been outperforming the 30 mega caps in the Dow Jones Industrial Average throughout March: The Russell 2000 is up 0.6 percent month-to-date vs. a 2.3 percent loss for the Dow.

That suggests that either traders believe the Fed's first rate hike won't happen for six months or more or, alternatively, that they are going to wait until Fed Chair Janet Yellen and her cohorts actually pull the trigger. Maybe the willingness to wait and see is because they've been burned once before: In September 2013, it was nearly unanimous that the Fed would start tapering its “QE3” bond-purchase program but the Fed surprised by waiting until December of that year before taking action.

Related: Stock Market Bulls Need to Step Up — or Else

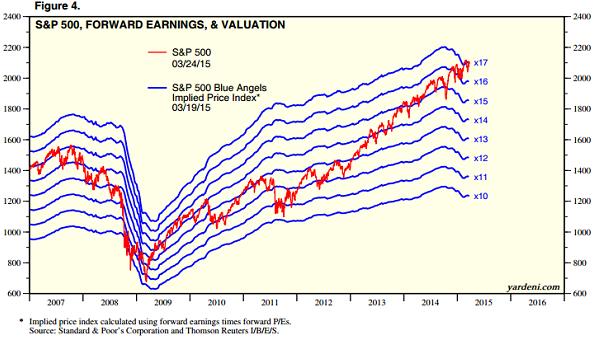

When it happens, the turbulence is likely to be severe given the way forward earnings expectations are rolling over. You can see this in the chart below from Yardeni Research, which compares the S&P 500's price level to what he dubs the "Blue Angels" earnings valuation lines — in reference to what look like vapor trails from fighter jets in the sky. The blue lines show both the path of forward earnings expectations and demarcate the levels of various price-to-earnings valuation multiples.

The danger here is that if stocks are going to rerate lower in terms of valuation, the drop in forward earnings will make that decline even deeper.

If you're looking for specific areas to avoid, Credit Suisse notes that automobile and consumer stocks were among the laggards in the last rate hike cycles. That suggests the likes of Ford (F) and General Motors (GM) will get hit hard, as well as sector ETFs like the Consumer Discretionary SPDR (XLY) — which maintains exposure to stocks like Walt Disney (DIS), Home Depot (HD) and Amazon (AMZN).

On Friday, Yellen provided some additional insight into when all this will go down. The overall impression was that September, or possibly later, is probably the right time to expect. She noted that there is still some way to go on restoring the job market to health and that any additional weakness in inflation would delay the first rate hikes. She added that while job market gains have been substantial, there could be value in allowing the labor market "to run a bit hot" for a period.

Related: The Middle Class Is Struggling in All 50 States

Assuming that this tightening cycle will be like the 1999 and 2004 precedents, stocks should find a durable low between two to four months after the Fed's first rate hike. Using September as the liftoff date, that puts us in or near the start of 2016. But if this is like 1994, large-cap stocks could continue to drift sideways while small-cap stocks drift lower until the Fed reverses course and restarts stimulus — either in the form of a rate cut or fresh bond buying. This is what happened when the Greenspan Fed cut rates in 1995.

If so, any sustainable low might not come until the tail end of 2016. Yellen herself alluded to the possibility of this Friday when she said the policy tightening pace could speed up, slow, pause or reverse depending on the incoming flow of data.

After the easy, rip-roaring gains of 2013 and 2014, investors will need to relearn patience as the market becomes more volatile in this uncertain policy environment.

Personally, I'm looking for one last hurrah pushing the NYSE Composite to new record highs in response to a "no hike" decision by the Fed in June, mimicking the stimulus-related market melt ups seen in bourses across Asia and Europe this year. If so, that'll represent the best last chance for investors to exit positions and prepare for what's likely to be the most difficult trading environment since the 2011 correction.

Top Reads from The Fiscal Times: